The year got off to a good start, so what should we be paying attention to now?

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

In our 2026 investment outlook, we have chosen a strategy similar to last year's. Given that the stock market is expensive and there is significant political uncertainty, but the loose fiscal and monetary environment and profit dynamics are supportive, we recommended maintaining neutral exposure regarding equities and using correction phases to build positions. Once again, we expect excess returns to come primarily from regional or sector picks, and based on the performances of these so far, we have reasons to be optimistic. However, not much time has passed yet from 2026, and we expected a volatile year, so there could still be periods of less favorable return data. Nevertheless, it is worth examining how the events of recent weeks—of which there have been quite a few—might influence the main trends and effects on our recommended topics for the rest of the year.

The following topics are those that we consider to be the most decisive from a market perspective in recent weeks:

AI investment boom: Most large technology companies announced investment plans for this year that exceeded previous expectations, with the four major companies (Alphabet, Amazon, Meta, and Microsoft) expected to spend nearly $700 billion this year, primarily on AI infrastructure development. These figures have once again raised fears among investors, as on the one hand, companies' free cash flow is almost disappearing (with the exception of Microsoft), which means that share buybacks, which previously provided significant support for share prices, may also decline, while there are also concerns about the future return on these projects. These concerns are not groundless, of course, and it is also true that investor expectations are increasingly high, which is easier for large tech companies to miss in the short term, and this may cause a temporary wave of corrections and a shift away from the technology sector. However, it is important to note that several of the companies concerned still appear to have everything they need to overcome fears about returns over time, which means that their long-term prospects can still be considered good/stable.

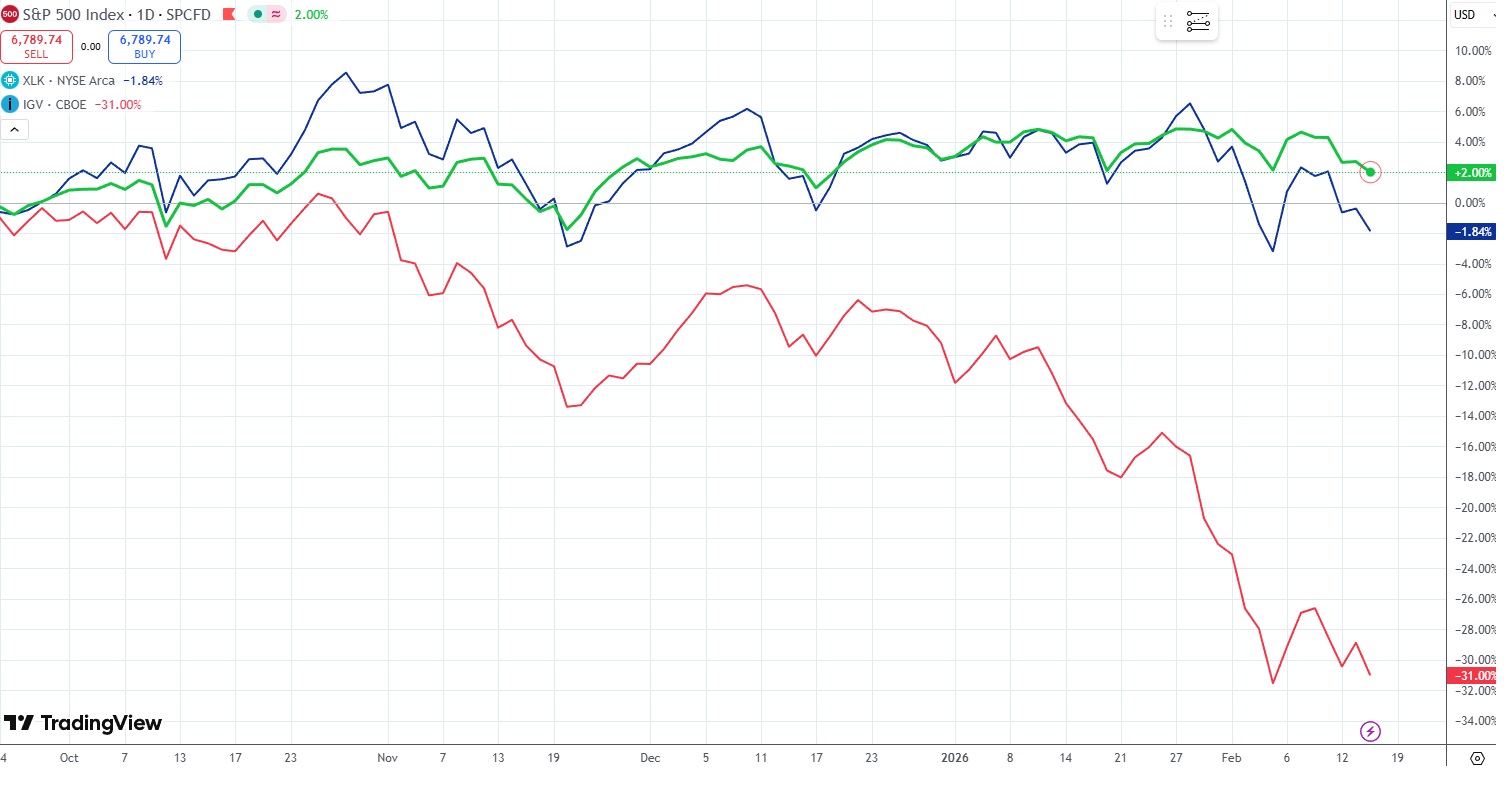

Software market slump: Software companies' ETF (IGV) has lost 30% of its value since last fall's highs, as the emergence of new AI solutions (Anthropic's announcements in recent weeks) poses serious challenges to the business models and growth prospects of some players. The sector was previously able to achieve high growth with high margins, which was rewarded by the market with high valuation multiples, but longer-term expectations suggest that the size of the market they can capture will shrink, which could render premium pricing multiples obsolete. Currently, however, players in the sector are being widely sold off, while there are sub-segments or companies within the sector that are protected from these challenges, making the price declines excessive in their case.

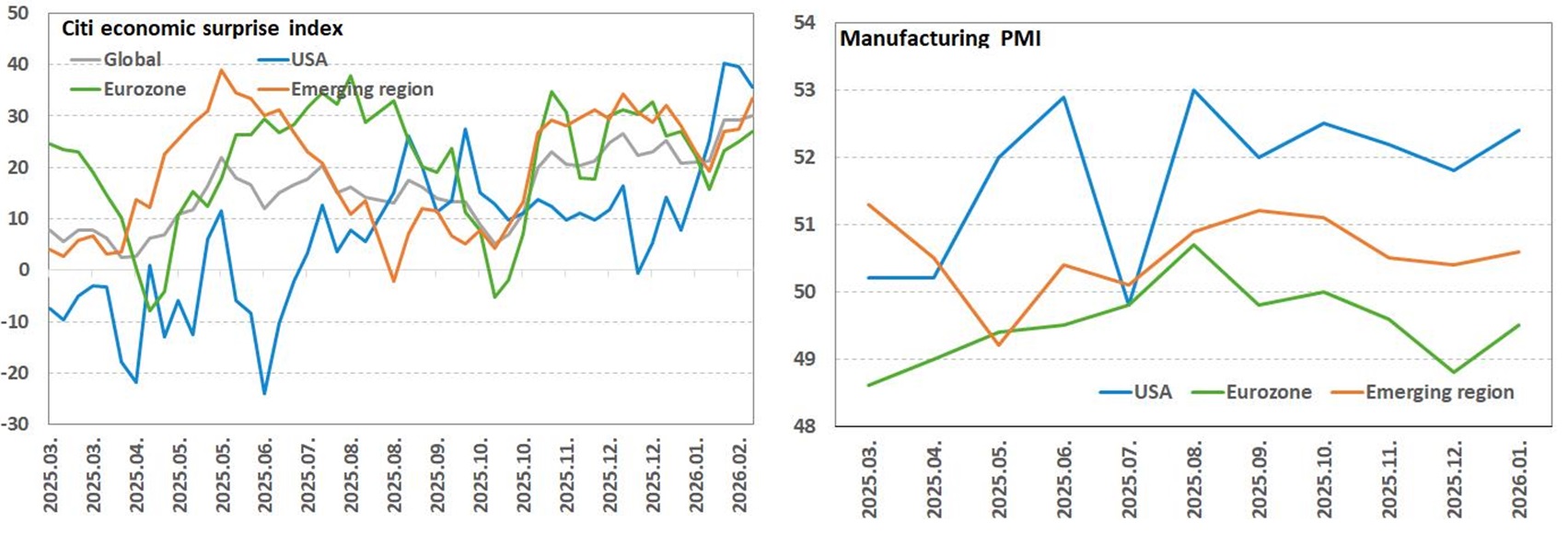

Economy: macroeconomic data shows a stable/positive picture overall, the outlook for manufacturing is improving, growth figures in major economic centers are better than expected, while there are no signs of noticeable inflationary pressure for the time being. In the US, the latest inflation statistics were particularly favorable compared to expectations, while the economic surprise index is rising sharply (partly driven by significant AI investments). The growth-boosting effects of the Big Beautiful Bill passed last summer will continue into this year, and with midterm elections coming up in the fall, minor easing measures have already been implemented, and it is possible that further easing may come in the near future (the much-discussed tariff rebate would be the really big bang among these). Recession risks therefore remain low in a loose fiscal and monetary policy environment, which is also being driven by AI investments, all of which is helping the corporate sector to achieve healthy profit growth.

Fed chair change: Trump's nominee for the position, Kevin Warsh, is considered to be a more hawkish central bank president than the other options, partly because he has repeatedly criticized quantitative easing (QE) in the past. Although this narrative may hold true for now (hearings will be held in the meantime, but concrete steps will not be taken until at least the end of May), given President Trump's commitment to low interest rates, this narrative could easily change over time. On the one hand, Warsh may argue for the need for interest rate cuts, citing the productivity-enhancing effects of AI. On the other hand, a possible reduction in the Fed's balance sheet could be risky from current levels, but its potential negative effects would likely be offset by banking deregulation, which, from a liquidity perspective, would not necessarily cause a disruption in the market.

Geopolitics: This year has also gotten off to a strong start on the geopolitical front. Just a month ago, everyone was wondering whether the US would try to take Greenland from Denmark by force. Narratives tend to swing toward extremes from time to time, which is reinforced by the American president's communication. What has been confirmed, however, is that the US considers the American continent to be its own territory (the approach called DONROE doctrine), where it will not tolerate external interference (see Venezuela or Cuba) and where its influence can continue to grow. All this, however, leads to accelerated divison of the world to different major geopolitical blocs, and the wavering confidence in American support is prompting Europe to rethink its own defense, trade, and alliance systems. Since last year's Trump-Xi agreement, there has been a de-escalation in the trade war between the two countries, but this does not seem sustainable in the long term. The Russian-Ukrainian peace agreement continues to progress slowly, while the US is gathering increasingly serious military forces around Iran, which increases the chances of a potential attack.

How does all this affect assets, regions, and sectors?

Equities: Fears surrounding the return on AI investments and AI's disruptive effects, strong geopolitical risks (Iran), and the hawkish narrative surrounding the change in the US Federal Reserve chair, combined with high valuation levels, unfavorable seasonal effects in February, and the optimistic positioning that developed at the beginning of the year, increase the likelihood of a short-term stock market correction. A decline of up to 10-15% from the peak would not be surprising at all, that's why we recommended a neutral equity exposure at the end of last year. For the time being, however, we believe that these declines can essentially be used to increase equity exposure, as economic data remains strong, the risk of recession is still low, companies are showing double-digit profit growth, and over time, fears about AI and risks surrounding the change of Fed chair may subside.

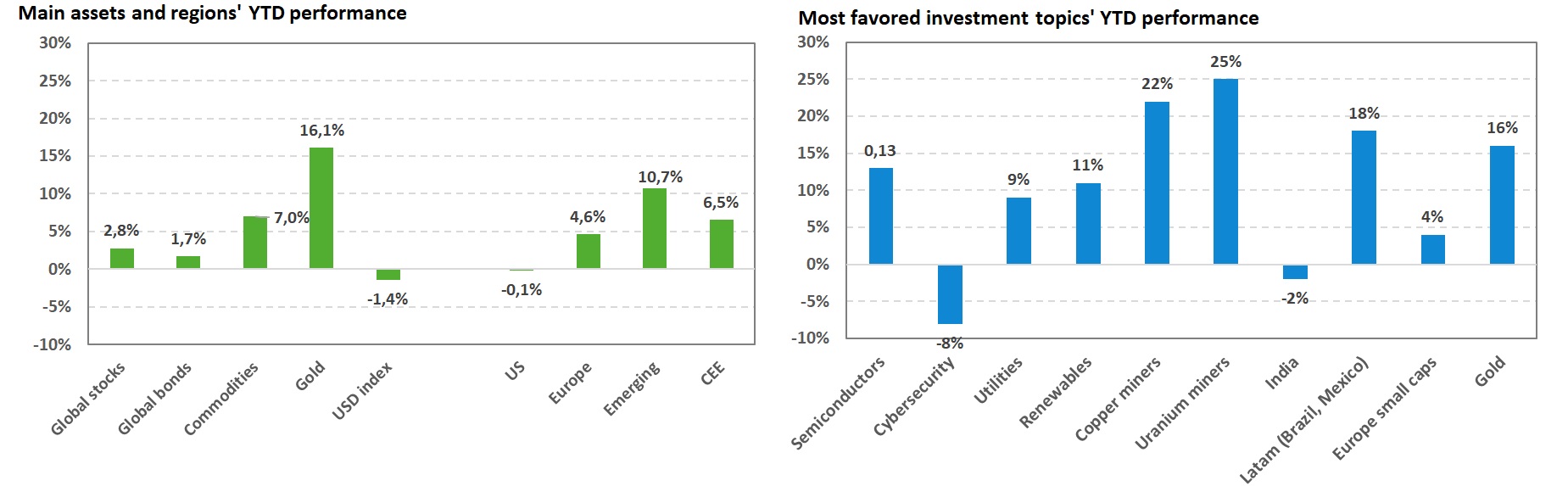

Regions: The US stock market has not had such a weak start to the year in relative terms for a long time, which can be explained in part by the processes discussed above (AI fears), which have a greater impact on US stock indices (due to the overrepresentation of the technology sector). However, as US economic data shows more positive surprises, this underperformance may disappear over time compared to Europe, which remains a cheaper market but also paints a much weaker picture in terms of profit growth. Emerging markets are the clear winners in terms of capital flows, and this effect also has a positive impact on our favorite region, Central and Eastern Europe. We would remain selective within the emerging markets, as although the Chinese risk has moderated in the short term (de-escalation), the US-China confrontation may remain with us in the long term (as by 2027-28, it will be within reach for the US to cover its rare earth metal needs from allied countries, the situation may tip towards escalation again), while China and the regions closely linked to it carry significant weight within the emerging market index. The undervaluation of the Central and Eastern European region has diminished significantly following the recent rise in exchange rates, but it may continue to benefit from emerging capital inflows. In any case, its performance is likely to increasingly align with the movements of emerging markets as a whole.

Favourite investment stories

Semiconductors: Semiconductor manufacturers are significantly outperforming the technology sector as a whole YTD. Meanwhile higher AI related infrastructure spending is causing concern regarding large technology companies, the prospects of semiconductor manufacturers are improving thanks to the higher demand for its products (chips). The weakness of the technology sector may, of course, have a negative impact on them indirectly, but the fundamentals remain stable until announcements are made about a significant reduction in investment plans. We wrote more about this here: These segments of chip-making is worth paying attention

Cybersecurity sector: The spread of AI agents poses a serious risk to the software sector, which may remain under pressure for a longer period of time, apart from temporary flare-ups. For the time being, investors are not making distinctions, but there will be some companies within the software sector where fears will ultimately prove to be exaggerated. We consider the cyber security sector to be one , which is in many ways more protected against AI solutions than the average software company. Over time, companies will be able to prove this by maintaining their growth figures, and high margins, meaning that the temporary pressure could even create favorable opportunities in the longer term. We wrote more about this here: AI shock on the software market: why could cybersecurity be a winner?

Utilities/renewables: The long-term fundamental story remains intact, with electricity demand expected to rise due to electrification, AI data centers, and the growing middle class in emerging markets, providing a boost to the utilities sector and renewable power generation. Furthermore, the utilities sector could outperform even during a market downturn due to its defensive characteristics, while the new Fed leadership's shift toward lower interest rates could be positive for renewables.

Mines (copper/uranium): The increase in electricity consumption may create a structural deficit in the copper or even uranium market in the longer term, which will only be reinforced by AI infrastructure spending that is higher than previously expected. Copper and uranium mines are therefore not affected by AI fears, but since we are talking about high-beta segments, a risk-averse period could lead to significant price declines in the short term, as high (COMEX) inventories should also be monitored in the case of copper. However, for those thinking longer term, it may be worth looking beyond these fluctuations.

LatAm: The Brazilian stock market was the winner, supported by the commodities' outperformance at the beginning of the year, and the strengthening of the DONROE principle is more likely to bring benefits than risks for the Latin American region. Based on this, the region is part of the US sphere of interest and, as such, is likely to be considered a popular destination for capital inflows. This is because the local stock market remains favorably priced, the potential of falling real interest rates offer further opportunities, and significant infrastructure investments are likely to keep commodity prices high, which also indirectly benefits the region.

India: In terms of geopolitical blocs, India continues to position itself as a bridge between the two sides. In recent weeks, a free trade agreement has been concluded with the EU, and US tariffs will finally be reduced to 18%, which could be an important catalyst for this year's economic outlook. In recent years, the local stock market has been less sensitive to market corrections driven by AI fears, meaning that if this were to cause further waves globally in the short term, we could expect Indian stocks to perform relatively stronger. We wrote more about this here: What can we expect from India this year?

European small caps: There has been no significant change in this segment, which is more sensitive to improvements in economic data, which is positive for them, as is the fact that the EU is increasingly recognizing that, in the process of global blocs formation, it needs to develop its own center of power (greater military, technological, and economic autonomy), which in turn requires strengthening its internal markets and removing regulatory and competitive barriers in order to succeed. These efforts may benefit smaller-cap companies that are more active in the internal market.

Gold: The parabolic rise at the beginning of the year ended with a sudden, significant drop at the end of January. The reasons can be traced back to the development of significant speculative positioning, which may have been catalyzed by the nomination of the new Fed chair and the intensified "hawkish" narrative surrounding him. As the latter effect may remain dominant in the coming months, gold may also see a period of consolidation, after which the question of whether it will rise or undergo a further downward correction may be determined by the Fed's monetary policy direction. Several factors continue to favor gold (geopolitical tensions, de-dollarization, rising debts, loose budgets, and central banks potentially supporting this with loose monetary policy), so even in the worst-case scenario, we can imagine a prolonged sideways movement due to excessive positioning rather than a rapid collapse in prices.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more