AI shock on the software market: why could cybersecurity be a winner?

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

The rise of AI agents has shaken confidence in software market players. Investors are not yet distinguishing between individual sub-sectors, so industry uncertainty has led to widespread price pressure. However, we believe that the cybersecurity segment may be structurally more protected against the disruptive impact of AI, and that the strict regulatory environment and emerging AI risks may actually increase demand for services. If the sector's leading players are able to deliver stable growth and strong guidance in the upcoming earnings season, this could fundamentally change the current negative market narrative. The cybersecurity industry is one of the favored sectors in our 2026 Investment Outlook.

The software sector was hit by another wave of sell-offs last week after Anthropic, a company specializing in artificial intelligence, launched new AI tools. The new solutions cover a range of areas, from legal and technology research to customer relationship management and data analytics functions, which are currently the core activities of many software company. The announcement reinforced industry fears that some companies may be able to replace certain subscription based software solutions in-house, which could significantly undermine traditional SaaS (Software as a Service) business models in the longer term.

In response to the news, the S&P 500 Software index fell nearly 10% in the first half of last week before rebounding. The sector has had a weak year so far: the index has lost about 15% of its value since the beginning of the year and has fallen nearly 27% from its peak last fall. Investor reaction has not yet differentiated between the various sub-sectors of the software market; the selling pressure is widespread. The market basically expects AI technologies to significantly reshape the software industry, but it is currently difficult to identify the structural winners and losers. As a result, many investors are reducing their exposure to the sector in general in order to mitigate risk

Although the pressure on software companies seems partly justified, we believe that certain sub-sectors—especially cybersecurity—may be relatively more protected against AI-driven cannibalization. One reason for this is that many cybersecurity solutions rely on real-time system logs and telemetry data, which are not necessarily available to large language models (LLM) during training, making their effectiveness less replicable with generative AI tools. Furthermore, cybersecurity systems must fit tightly with companies' complex software and network infrastructure, making solutions such as Secure Access Service Edge (SASE) or identity protection very difficult to replace with in-house, coding AI agents.

Market leaders in this field, such as Zscaler (SASE) and Okta (identity protection), have high customer retention rates, which strengthens their resilience to AI-based disruption. Strong loyalty and their role in critical infrastructure may support their growth prospects in the medium term, which could lead to upward revisions in revenue forecasts. Palo Alto Networks' acquisition of CyberArk (an identity protection services company) announced last summer also suggests that building a comprehensive identity security ecosystem in-house or relying on large language models is extremely difficult to achieve. Furthermore, companies offering multi-product (bundled offerings) security platforms, such as Palo Alto or CrowdStrike, may be more secure, as companies today prefer security solutions that integrate multiple functions.

The business model of cybersecurity companies is also protected by a strict regulatory environment, which imposes high levels of transparency, auditability, documentation, and risk management requirements on security systems. The compliance burden is particularly significant in the financial sector and for critical infrastructures, while serving government customers requires additional special licenses—such as FedRAMP certification for cloud services—which involve ongoing control reports and strict security documentation. In the case of in-house developed AI-based security solutions, companies would bear full compliance and audit responsibility, while in the case of an external service provider, a significant part of this burden would be borne by the cybersecurity company itself, which has the required certifications, audit processes, and governance frameworks in place. All of this creates a meaningful layer of protection for players in the sector and limits the rapid spread of in-house alternatives based on AI agents.

In addition, we believe that the spread of AI agents will not weaken but rather strengthen the demand for cybersecurity services, as the more AI-driven applications are developed, the greater the emphasis will be on minimizing the attack surface. New AI-based tools bring new types of security risks, such as prompt injection attacks—a vulnerability in large language models where attackers insert malicious instructions that can be used to steal data—as recently demonstrated in a case where Anthropic's AI model was used in a cyberattack. As companies entrust more and more business processes and operational sub-functions to AI algorithms, their potential attack surface expands, which can generate structurally higher demand for cybersecurity services.

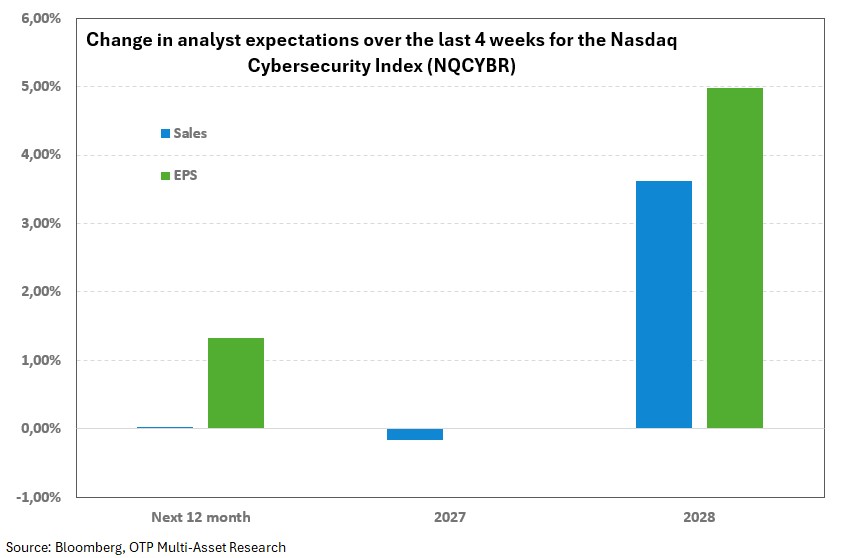

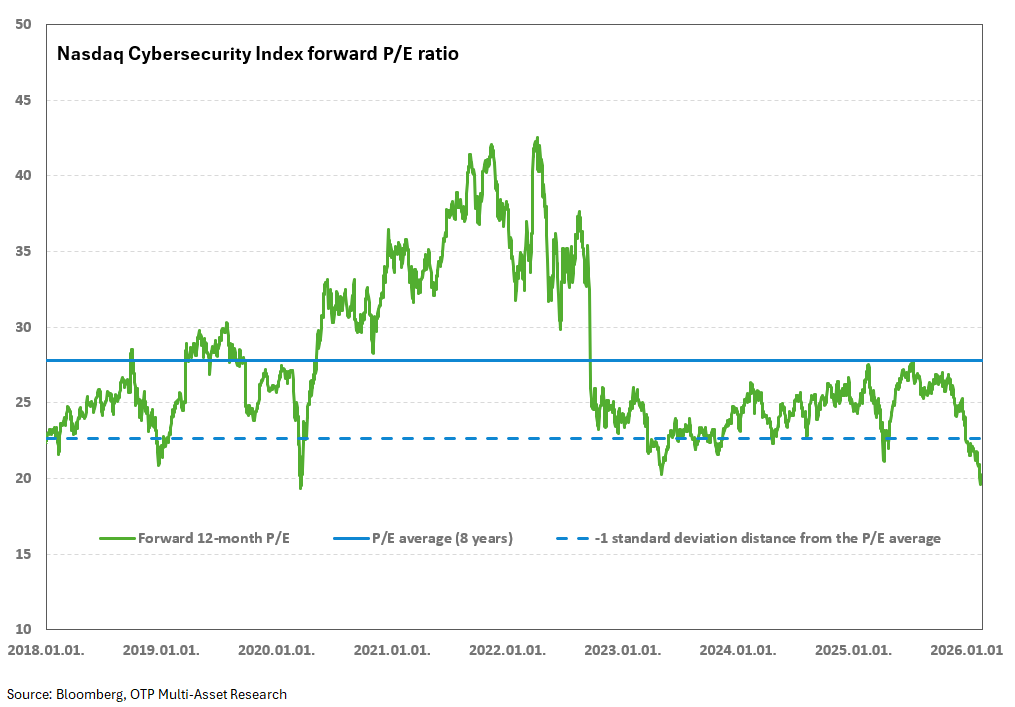

While investors have been concerned about the long-term growth prospects of the cybersecurity industry, along with other software companies, analysts' expectations do not reflect these fears at this time. Revenue and profit expectations for 2028 have improved by 3-5% over the past month, while cyber security companies' share prices have fallen by nearly 10% over the same period. As a result, the industry's valuation multiples have declined significantly and are now at historic lows not seen since the Covid period. Thus, if market sentiment changes with regard to the industry, there is plenty of room for growth.

The upcoming earnings season could serve as an important catalyst for the cybersecurity sector. If leading industry players can demonstrate that their growth rates are not slowing down and management provides better-than-expected annual guidance, this could significantly challenge the current negative narrative. The earnings season has been mixed so far, but overall the picture is supportive: Fortinet exceeded analyst consensus in both quarterly results and guidance, while Datadog's annual forecast fell slightly short of analyst consensus, but this may be explained by management's traditionally cautious approach. The market reaction was positive in both cases (Fortinet +4%, Datadog +14%), suggesting that the recent weeks' price weakness may have already priced in the risks to a significant extent, and even with mixed results (see Datadog), a meaningful rebound may occur. However, the sample is limited for now, so it is worth waiting for further earnings reports. Among the key players in the sector, Palo Alto will publish its figures on February 17, Zscaler on February 26, CrowdStrike on March 3, and Okta on March 4—these reports will be particularly worth paying attention to.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more