Winners in the AI-driven semiconductor cycle

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

The main driver of growth in the semiconductor sector continues to be logic and memory chips related to AI infrastructure, which have the most favorable growth prospects within the entire sector. Demand in these markets consistently exceeds supply, resulting in a strong pricing environment and improving corporate margins. Following our previous analysis of the risks and structural catalysts in the sector, this article focuses on which companies are likely to benefit most from the tailwinds affecting the industry, particularly in the logic and memory chip markets, which are at the center of growth.

Our previous analyses presenting the industry background can be accessed via the following links:

These segments of chip-making is worth paying attention

The building blocks of the future: what you need to know about chips

By 2026, revenue growth of over 30% is projected for both the logic and memory chip markets, primarily due to strong demand generated by data center investments. In contrast, only single-digit growth is expected in other segments of the semiconductor industry. The geographical focus of growth will remain on the United States, where the pace is likely to accelerate compared to last year. In view of these favorable trends, our analysis focuses on these markets as we attempt to identify the players that are likely to benefit from industry trends, while also assessing the extent to which the positive outlook has already been factored into the valuations of the companies concerned and how much upside potential remains in their shares.

Nvidia

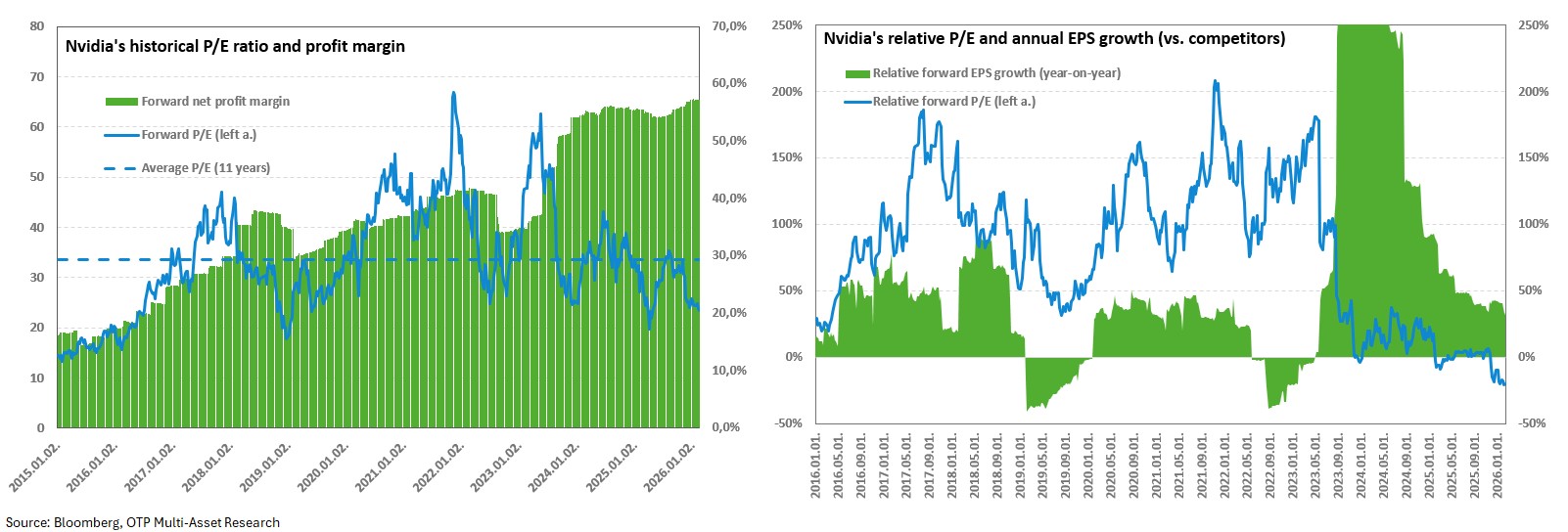

Nvidia, which has become a key player in the semiconductor industry in recent years, remains an unavoidable investment target in the AI-driven technology cycle. Although its share price has risen about tenfold over the past three years, the movement is justified by its fundamentals. The data center business, which accounts for the majority of revenues, is enjoying structural demand growth with the spread of generative AI models coming to market at the end of 2022 and is the number one winner of AI infrastructure investments. Nvidia GPUs have a nearly 95% share of the GPU market, while GPUs account for more than 90% of AI chips. As a result, the company's approximately 85% share of the AI chip market makes it a dominant player.

The company has been able to achieve such an outstanding market position thanks to its chips, which outperform those of its competitors, and the supporting CUDA software ecosystem. This technological advantage provides significant pricing power, which is clearly reflected in the company's extremely high margins. When building Nvidia-based data center infrastructure, hyperscale technology companies spend 40-50% of their capital expenditures (Capex) with the company (expected to be ~$300 billion this year, which is ~90% of revenue), so the investment intensity of large technology players has a significant impact on revenue growth. As these companies have sharply increased their capital investments in building AI capacity in recent years, this has directly supported Nvidia's revenue and profit dynamics.

With such strong structural tailwinds, one might rightly assume that the company is trading at a premium valuation, but this is far from the case. The company's forward P/E ratio of 23 lags behind the average of 29 for AI-related chipmakers, but the stock is also trading at a discount compared to broader technology stocks. There are two main investor concerns behind this. On the one hand, the market expects that the current growth rate is not sustainable in the longer term and that revenue/profit growth will gradually slow down. In the short term, however, this fear is not justified: this year, the company could achieve nearly 60% growth in both revenue and earnings, similar to the 2025 expansion, which could be supported by the Capex increase plans announced by hyperscale companies in recent weeks. In the longer term, the high base effect may indeed lead to a slowdown, but by 2030, the average annual growth rate (CAGR) could be around 25%, which is still considered extremely robust, especially given the current valuation.

Another concern is that the company may lose market share due to intensifying competition, which could negatively affect its pricing power and ultimately lead to margin compression. Although Nvidia's market share is expected to decline in the coming years, the extent of the decline is difficult to predict at this stage. There are currently no truly competitive alternatives in the GPU market, while GPU architecture continues to offer a significant advantage over custom-designed AI chips in computationally intensive training processes. In addition, the cost of switching data center infrastructures already built on Nvidia hardware and software ecosystems can be high, which strengthens the company's embeddedness year after year. Based on analyst expectations, Nvidia's market share in the AI chip market could stabilize at around 70% by the end of the decade, which would continue to allow for above-average margins. Although a certain degree of margin compression is a realistic risk in the longer term, there are no short-term signs of this in the company's results.

Nvidia's current valuation is not only discounted relative to its direct competitors, but also lower than the company's own historical average, while margins are at record levels and growth continues to significantly exceed the industry average. The fundamentals are therefore significantly more favorable than for most competitors. In addition, there are several potential positive catalysts, including recent plans by large technology companies to increase capital expenditure and the possible resumption of sales in China – the latter is supported by both sides, but Nvidia has not yet received final approval. In light of all this, higher pricing than at present may appear fundamentally justified.

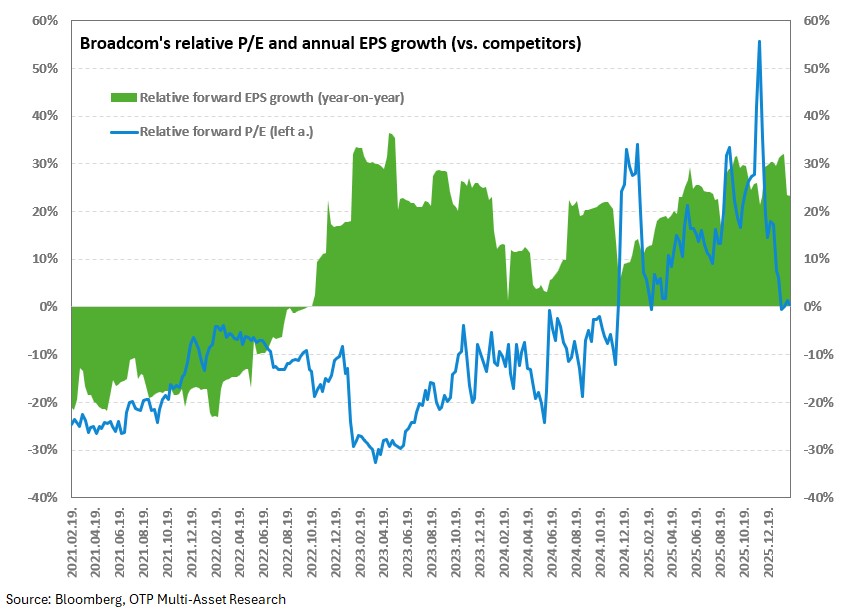

Broadcom

Broadcom, which leads the market for custom-designed AI chips (AI-ASIC) with a 70% share, is one of the big winners in AI infrastructure investments, similar to Nvidia. However, unlike Nvidia, it is not present in the GPU market, but is involved in AI-ASIC design, the advantages of which are primarily evident when using pre-trained AI models, as they can be optimized for specific tasks and are energy efficient. The focus is expected to gradually shift from training to inference in AI models, which paints a more favorable long-term growth picture for the AI-ASIC market.

The TPU (Tensor Processing Units) architecture, jointly developed by Broadcom and Google, is currently considered the market-leading solution in this segment. The main competitive advantage of the latest TPU model is its outstanding energy efficiency: it outperforms Nvidia's B200 GPU by nearly two times in terms of performance per watt (which is, however, a generation older). This feature could make Broadcom particularly valuable in a market environment where the next bottleneck in the AI value chain could be energy demand and electrical capacity constraints. In addition, the average unit price of TPUs is just over a third of the cost of an Nvidia GPU, although GPUs remain difficult to replace in the training phase. However, the lower product price is also reflected in the gross margin of the company's semiconductor business, which is around 55-60%, compared to Nvidia's level of around 75%.

Broadcom is not only present in the AI value chain with its hardware solutions, but also offers critical IT infrastructure software, including virtual machines, hybrid and multi-cloud environments, and endpoint and network security-focused cybersecurity services. These infrastructure-level software areas are expected to be more resilient to the disruptive effects of AI than application software providers. As a result of Broadcom's enterprise-focused software portfolio and cost-efficiency-driven reorganization, the software business achieved a gross margin of 93%, raising the overall enterprise gross margin to around 74%. In addition, the software division has transitioned to a fully subscription-based revenue model, which provides greater revenue visibility and stability, thereby mitigating the cyclicality of the semiconductor business and helping to maintain the company's higher valuation.

In September, investors may have gotten ahead of themselves, so a bunch of good news might've already been priced into Broadcom's stock. But since then, there's been more positive news. During the fall, the market reclassified Google's latest AI model from a laggard to a leader, attributing its competitive advantage in part to the TPU architecture developed jointly with Broadcom. This has led to a significant increase in demand for TPUs, resulting in new large orders, including Anthropic's approximately $11 billion deal. Overall, the positive news raised EPS expectations for 2026 by more than 50%, but the share price did not follow suit, leading to a significant improvement in the company's valuation. If energy becomes the next bottleneck in the AI value chain, demand for Broadcom's highly energy-efficient TPU solutions could accelerate even further.

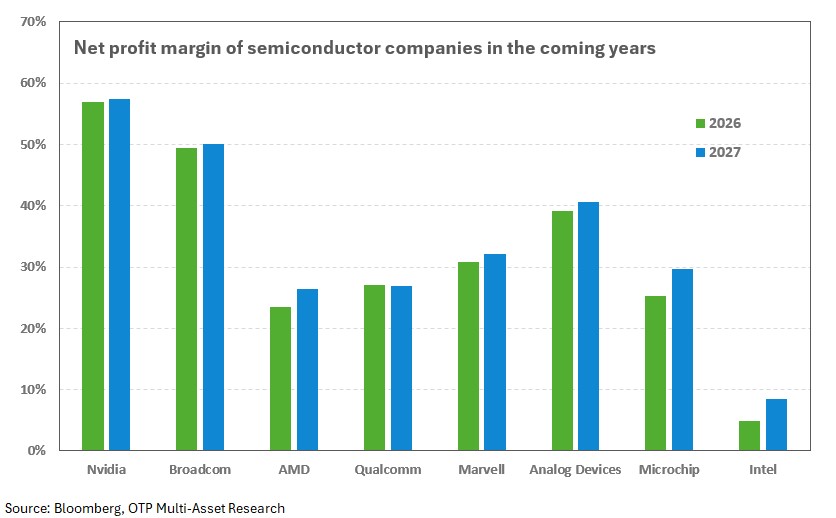

In the short term, Broadcom could be one of the biggest beneficiaries of Google's significantly higher-than-expected Capex forecast of around 50%. Since at least half of the company's hardware revenue is estimated to come from Google, this could result in significant additional revenue growth, the impact of which is not yet fully reflected in the share price. Broadcom's forward P/E ratio of 29 is essentially in line with both its competitors' and its own valuation levels over the past two years, but the company has more favorable growth prospects in both the short and long term (revenue CAGR of ~27% through 2030) and it has the second-highest profitability metrics after Nvidia (net profit margin: ~52%), which could even justify a premium valuation.

Another supporting factor is the company's software business, which provides a stable, subscription-based revenue structure, mitigating the cyclicality of the traditional semiconductor market – this may also justify higher pricing. However, among the risks, it should be noted that approximately 17% of revenues come from China, which represents a significant geopolitical exposure. In addition, the high concentration of hardware revenues towards Google (>50%) increases customer risk, while a further increase in the proportion of revenues from the semiconductor segment may moderate corporate-level margins in the longer term.

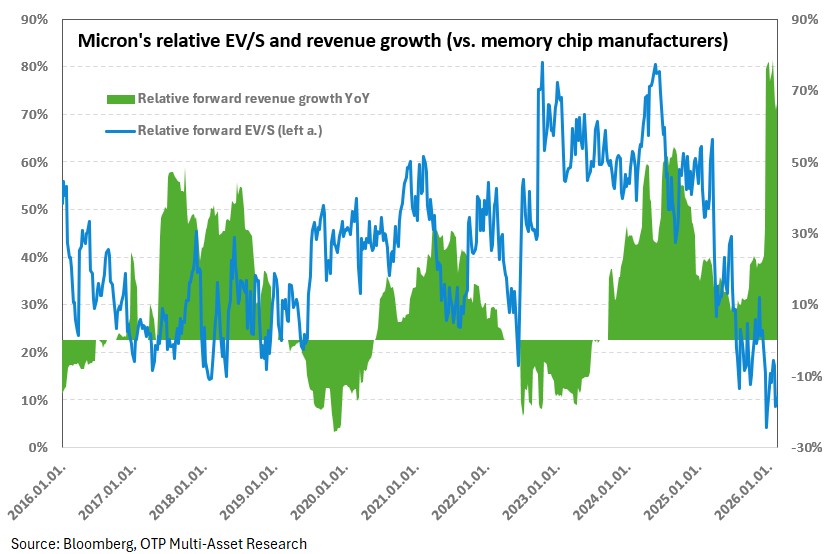

Micron

Unlike the previous companies, Micron Technology, which is also on our Equity Top Pick list, does not operate in the logic chip market, but is the largest US player in the memory chip market, which is also supported by the AI investment wave. In order to meet the high memory demands of data centers, companies in this segment have shifted their manufacturing capacity toward high-bandwidth memory chips (HBM) with the higher data transfer speeds required for this purpose.

Increasing the sales ratio of HBMs, supported by structural tailwinds, can help mitigate the strong cyclicality typical of the industry, and the product has also become the focus of memory manufacturers due to its higher margins compared to traditional memory products. At the same time, the shift to HBM has caused a decline in the supply of traditional PC and smartphone memory products (DRAM, NAND), resulting in significant shortages in these segments. As a result, prices for traditional memory chips have risen many times over in recent months.

The primary beneficiaries of this process were memory chip manufacturers, which performed exceptionally well in terms of growth and profitability, while other players in the value chain experienced cost pressures due to rising input prices. In the case of Micron, despite the seemingly favorable forward P/E ratio of ~10, the sharp rise in memory prices seen in recent months has most likely already been factored into the share price, with the current valuation level more in line with the typical end-of-cycle range for the memory sector (9–12 P/E). At the same time, unlike previous cycles, a more sustainable demand environment is emerging: supported by AI-driven structural growth factors, market tightness is expected to persist over the next 1–2 years, with no significant improvement in supply-demand conditions in sight for the time being.

The typical upturn phase of the memory chip market usually lasts 2–3 years, and the current cycle has already entered its third year. However, based on the intensity of AI infrastructure investments and the earliest expected appearance of capacity expansions in the memory industry in the second half of 2027, this cycle may be more sustained this time around. A prolonged upturn period may justify higher valuation levels in historical comparison, and further increases in memory prices cannot be ruled out. Short-term demand pressure may be further intensified by major PC and smartphone manufacturers, which previously built up their memory inventories at lower contract prices but may need to replenish them in the second half of the year due to their product refresh cycles. Due to the current supply shortage, new contracts are expected to be concluded at significantly higher prices, which may generate extra demand and further strengthen the upward trend in memory prices.

Thanks to the extremely favorable demand environment, Micron could practically double its revenue this year, while its earnings could more than quadruple compared to the already record-breaking base. The company's margin profile could also improve significantly, with the net profit margin expected to approach 40% by 2026. Micron outperforms its competitors in all key metrics and is also in a strategically advantageous position: it is the only major US HBM manufacturer, while its planned domestic capacity expansions mean it is less affected by potential tariff risks. Among its competitors, South Korea's Samsung and SK Hynix also have strong fundamentals, and some analysts believe they may be ahead in the development of next-generation HBM solutions. This could raise questions about Micron's role as a supplier of Nvidia.

However, Micron's management strongly denied that there were any performance issues with the company's new HBM solution and announced that mass production would start earlier than expected. In the short term, in a strong demand market environment, Micron's inclusion among Nvidia's suppliers does not significantly affect fundamentals, as demand for the products is already abundant. In the longer term, however, in such a competitive market, weaker performance by management could result in a discount in valuation. However, momentum remains strong in the near term: analysts have revised their revenue and profit expectations for 2026 and 2027 upward by 10-12% this year. If the company can prove that it is able to keep pace with its South Korean competitors in HBM technology, this could serve as a further positive catalyst for the company.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more