6.9% deficit is projected for 2026, and 5.3% for next year

Related content

Palantir Delivers Another Blowout Quarter

Palantir reported an outstanding quarter, with accelerating growth, expanding margins, and a record contract backlog. Management raised its full-year guidance, continuing its recent pattern of upward revisions. The shares are expected to open Tuesday’s session around 15% higher. Palantir remains on our Equity Top Picks List.

AWS Puts Amazon Back in High Gear

Amazon's stock price surged following the release of a better-than-expected preliminary report. Investors primarily praised AWS's spectacularly accelerating growth and outstanding profitability, and not even the announcement of a capex plan increased to $220 billion could dampen the mood.

6.9% deficit is projected for 2026, and 5.3% for next year, as the effect of tax cuts and higher pensions build up while one-off expenditures fall out in 2027

After many years of 7-8% deficit, an adjustment was made in 2024, despite the unfavourable macroeconomic environment. This brought the deficit down to 4-5% of GDP, which could be considered as an average level in regional comparison.

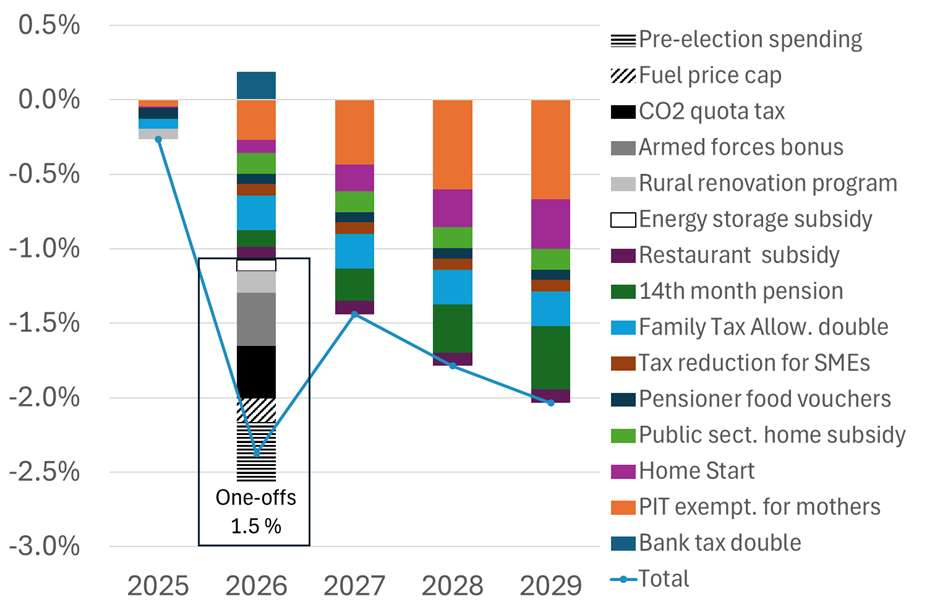

After the 4.7% in 2025, the deficit could reach 6.9% in 2026 due to government measures like the extension of PIT exemptions for mothers and families, the 6-month bonus for law enforcement workers and soldiers, the Home start program and home subsidy for public workers, 14th month pension, tax reduction for SMEs and the energy storage, restaurant, confectionary subsidies (Figure 1), pre-election spending, new measures that the current government is expected to introduce this year (Table 1).

In 2027, several one-off expenditure items are expected to drop out, while this year’s pre-election spending measures will no longer weigh on the budget. In addition, interest expenditures are likely to decline. However, the further extension of tax exemptions, the gradual introduction of the 14th-month pension, and lower revenues from windfall taxes are expected to exert pressure on the fiscal balance. Overall, based on currently available information, we expect the budget deficit to improve to 5.3% of GDP (Table 2). It should be noted, however, that the fiscal plans of the new government have not yet been announced. More details are expected to be presented in a supplementary 2026 budget and a medium-term fiscal plan this autumn, which should also outline the path toward reducing the deficit below 3% of GDP, as required to meet the Maastricht criteria.

Hungary's ESA-based fiscal deficit increased to 5.5% of GDP in 2026Q1, from 4.7% in 2025Q4 on a four-quarter (4Q) rolling basis, due to a 9% deficit in Q1 (Figure 2). This was lower than the 10.7% published in the financial accounts one day earlier. The reason for the gap was that the HCSO uses seasonally adjusted GDP in the denominator, while the central bank uses unadjusted data, correcting with this discrepancy the HCSO number would only be 0.1 ppt lower. The 0.8 ppts increase in the deficit was the result of a 0.9 ppt increase in the expenditure-to-GDP ratio, while the revenue-to-GDP ratio increased by only 0.1 ppt.

Expenditures as a percentage of GDP on a 4Q basis were affected to the largest extent by higher public wages (+0.7 ppts), other expenditures (+0.5 ppts), financial transfers (+0.2%) and lower investments (-0.2 ppts) and interest expenses (-0.1 ppts). In case of public wages, the 6-month bonus for armed forces and other wage hikes can explain the increase. The rise of other expenditures can be explained by higher expenditures on state property at the end of last year, pre-election spending, and base effects. Financial transfer rose mostly because of the payout of the first week of the 14th month pensions. The decline in public investment was in line with our assumption outlined in our previous GDP report on Q1 GDP. The remaining expenditure items did not change significantly (Figure 4).

On the revenue side, production taxes were down by 0.2 ppts partly explained by lower excise tax revenues on fuels and other products, plus income from financial transaction duty and insurance tax also declined. The remaining revenue items changed between -0.1 and 0.1 ppt (Figure 5).

The fiscal deficit in 2026 could reach around 6.9% of GDP, considering both the measures already embedded in the budget and the financial transfers promised by the new government for this year. The previous administration introduced several significant measures last year (outlined in an earlier flash report) that had only a moderate impact on the 2025 deficit but are expected to weigh more heavily in subsequent years. Their effect will be particularly pronounced in 2026 due to several one-off expenditures. The most notable include the six-month salary bonus for law enforcement personnel and military staff (HUF 450 billion), the restaurant and confectionery subsidy scheme (HUF 110 billion), the energy storage subsidy (HUF 100 billion), and the rural renovation program (HUF 180 billion), which expires in 2026.

In addition, the Court of Justice of the European Union ruled in April that Hungary’s tax on CO2 emission allowances may be incompatible with EU law, subject to confirmation by the national court. Should this be upheld, the government would need to refund taxes collected between 2023 and 2025, while also losing the revenue planned for subsequent years. This would increase the deficit by approximately 0.3 ppts of GDP. Furthermore, in parallel with the introduction of the fuel price cap strategic reserves were released at a below market price and the excise tax on fuel was cut, which would increase the deficit by 0.2 ppts altogether in 2026. On top of that, monthly cash-based data also suggest that the outgoing government engaged in significant front-loaded spending earlier in the year, potentially adding around 0.5 ppts to the deficit. As shown in Figure 1, the combined net impact of these measures—after accounting for the positive feedback via higher consumption and income tax revenues—is estimated at -2.4% of GDP, of which around 1.5 ppts reflect one-off spending.

Additionally, the incoming government has pledged to introduce a school start grant, raise low pensions, and increase family benefits by 50% this year. While the details remain unclear, assuming the latter two measures take effect from September (i.e. for the final four months of the year), their combined net impact of those three measures would amount to around 0.2% of GDP. If a food voucher scheme for pensioners is also introduced under a similar timeline (instead of the HUF 30.000 paid last year), it could add another 0.1 ppts to the deficit. At the same time, we assume that the envisaged savings measures (e.g. improving public procurement efficiency or reducing excessive communication spending) will not yet materialise in 2026.

As part of a political agreement between the Hungarian government and the EU, approximately EUR 6.5 billion in RRF grants and EUR 3.5 billion in RRF loans are expected to be disbursed in 2026, in addition to ongoing cohesion fund inflows. If RRF loans were used to finance new investments, this would raise the deficit; however, we assume that most of these funds will be directed toward existing projects, effectively serving as a cheaper source of financing. EU grants and cohesion funds will also enable the government to substitute domestic financing with EU funding in certain ongoing investments (subject to minimum co-financing requirements). Moreover, the government may choose to scale back low-priority legacy investment projects. Plus, public investment is expected to rise in 2026, supported by EU funds, which could also contribute positively to growth and tax revenues.

Looking ahead, we expect the deficit to narrow to around 5.3% of GDP in 2027, as the expiration of one-off spending items offsets the deficit-increasing effects of gradually introduced tax exemptions and the partial phase-out of extra taxes. One-off expenditures amounting to roughly 1% of GDP are set to drop out of the budget in 2027, plus the extra pre-election spending (around 0.4 ppts) will no longer weigh on the deficit. In addition, interest costs are projected to decline by 0.5 ppts, On the downside, the further extension of personal income tax exemptions for mothers with two children will reduce revenues, and we assume pensioners will receive an additional week of pension payments, as previously promised. We also factor in the gradual rollback of a significant share of extra taxes (around 0.2 ppts of GDP on top of rolling back the doubling of the windfall tax on banks). Meanwhile, the excise tax on fuels—temporarily reduced in response to the oil price shock—is expected to be restored as oil prices normalize. Regarding the new government’s additional commitments, which are expected to be implemented gradually from 2027, our earlier analysis of the Tisza program suggests that planned savings and revenue-enhancing measures (such as a potential wealth tax) could broadly offset the associated costs, despite some uncertainty. Accordingly, we assume that any new deficit-expanding measures introduced from 2027 will be fully financed by corresponding savings or additional revenues.

Figure 1 – One-off outlays and medium-run effect of major government measures on the budget balance*

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more