GDP growth picked up to 1.7%, supported also by one-offs. The victory of the TISZA party improves the mid-term outlook

Related content

Palantir Delivers Another Blowout Quarter

Palantir reported an outstanding quarter, with accelerating growth, expanding margins, and a record contract backlog. Management raised its full-year guidance, continuing its recent pattern of upward revisions. The shares are expected to open Tuesday’s session around 15% higher. Palantir remains on our Equity Top Picks List.

AWS Puts Amazon Back in High Gear

Amazon's stock price surged following the release of a better-than-expected preliminary report. Investors primarily praised AWS's spectacularly accelerating growth and outstanding profitability, and not even the announcement of a capex plan increased to $220 billion could dampen the mood.

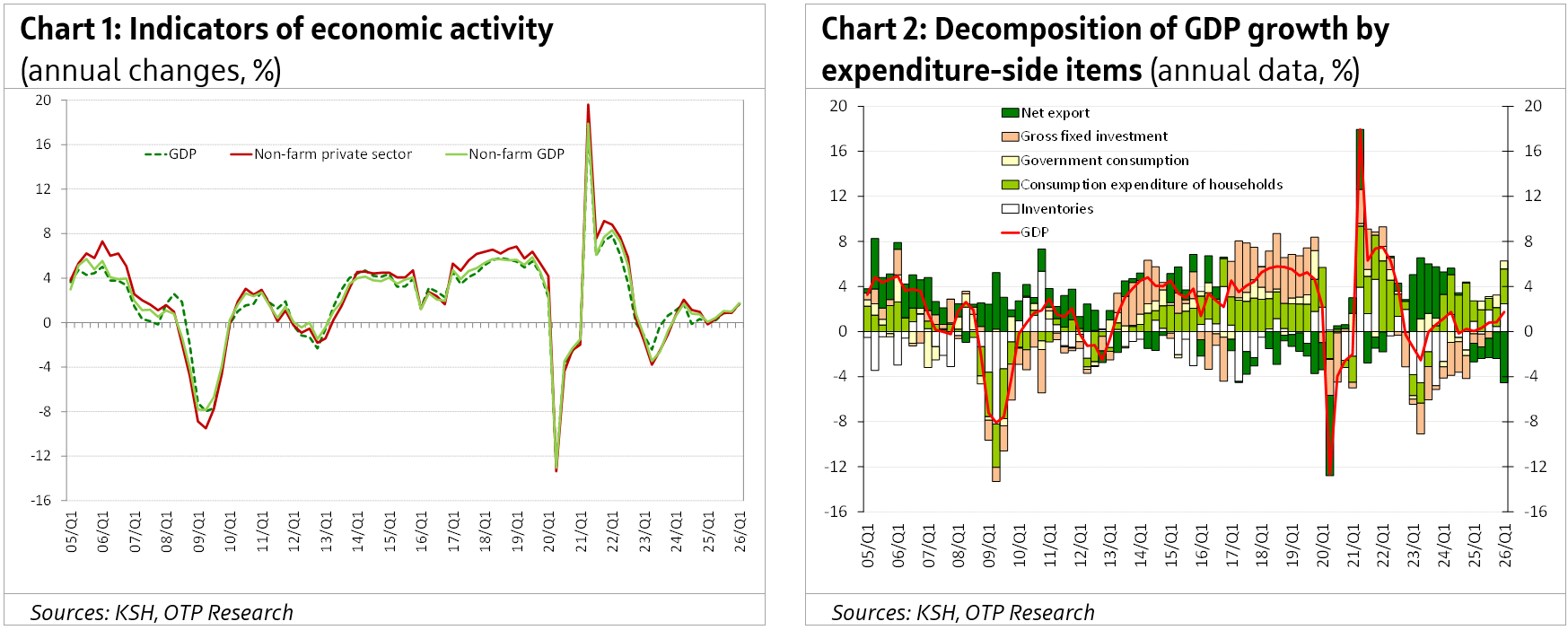

In Q1 2026, Hungary's gross domestic product grew by 1.7% year-on-year (unadjusted), which is in line with the preliminary estimate. As a reminder: the preliminary GDP growth data was higher both than our forecast and the market consensus (both was around 1.2% YoY). On a quarterly basis, in Q1 GDP growth accelerated from 0.2% to 0.8% according to KSH’s data. Our in-house seasonal adjustment shows the acceleration of growth was somewhat lower as the QoQ rate rose from 0.3% to 0.7%. Non-farm GDP and non-farm private sector’s GDP rose by 1.7 and 1.6% year-onyear, respectively. After many years of subdued growth performance, Q1 figures looks promising.

· The key question is to what extent one-off, pre-election measures contributed to GDP growth in Q1. The detailed data have reinforced our view that temporary factors may indeed have played a role. On the expenditure side, we observe a significant quarter-on-quarter increase in the ‘Professional, scientific and technical activities, administrative and support service activities’ sector. Fiscal expenditures reached an unusually high level in Q1, as the government paid bills before the election. News also arrived about a framework agreement between the former government (the Ministry of Defence) and the 4IG holding (IT, telecommunication and defence) in a worth of HUF 1300 bn (~EUR 3.6 bn). We cannot rule out the possibility that the exceptional growth in this sector reflects pre-election payments either to the sector more broadly or to 4iG in particular, which may have been recorded in GDP statistics. Another factor suggesting the presence of one-off effects in Q1 GDP is the unusual spike in industrial output and retail sales in March, following relatively subdued figures in January and February. The weakness in goods exports in March and April increases the likelihood that the strong March industrial production data was driven by inventory accumulation, which made a notable contribution to overall GDP growth.

· We expected consumption to remain the main driver of growth in 2026, with investment also rebounding after four years of contraction. We expected the contribution of net exports to decline due to higher imports driven by strong consumption and investment, but we expected export growth to return after two years of decline. So far, Q1 data have only confirmed robust consumption growth (5.5% YoY, up from 2.9% in Q4, and 1.3% QoQ). Investment activity, however, has remained subdued (-0.1% YoY after -0.2% in Q4). This is likely largely due to the fact that the government was much less able to spend on investments than we had anticipated due to the elections, as there are clear signs of a turnaround in private-sector investment. While the contribution of net exports declined as expected, exports themselves continue to contract (-1.8% YoY, broadly in line with the -1.7% recorded in Q4), despite the fact that the BMW plant in Debrecen has already begun production. The current strong exchange rate is unlikely to dampen further significantly the Hungarian export growth, as the depreciating exchange rate of previous years seen so far has not had a meaningful positive effect on export growth; in fact, Hungarian exports have tended to lag behind those of other countries in the region. The stronger exchange rate will instead reduce exporters’ profits, which may help anchor wage hikes at a level consistent with the inflation target.

· Although Q1 GDP growth came in above our nowcast (1.2% YoY), the 1.7% reading is consistent with our medium-term outlook, which points to around 1.8% GDP growth for 2026 as a whole.

Based on the data released so far, we therefore maintain our view that growth in the 1.5–2% range is achievable this year, although some downside risks remain. In our baseline GDP trajectory, we expected strong Q1 performance to be followed by weaker quarter-on-quarter growth in Q2 due to post-election effects. However, we cannot rule out the possibility that this slowdown could be more pronounced than previously assumed. Additional downside risks stem from the emerging oil shock. The impact of such supply shocks can become highly nonlinear once certain thresholds are reached; if oil prices were to rise to around $150, the drag on growth could reach approximately 0.6–0.7 percentage points both this year and next.

· On the other hand, the landslide victory of the opposition TISZA party has significantly improved Hungary’s medium-term growth outlook. While the budget will need to be adjusted in the coming years to meet the euro adoption criteria, we do not expect these measures will have significant negative effect on growth. First, the government will start the adjustment by the unblocking EU funds of EUR 16.4 billion (already negotiated). In addition, a major part of the adjustment could be made through cutting less-productive expenditures and reallocating funds toward growth-friendly areas. In addition, a credible euro-adoption plan could result in a sharp fall in interest rate expenditures (the 200bps downward shift in the yield curve could cut interest expenditure (to GDP) by around 1 percentage points in a few years’ time. The government is also committed to strengthen competition in the economy, to abandon unpredictable legislative practices and to fight corruption (for example via joining the European Public Prosecutor's Office). In addition, energy prices are expected to normalize next year, which will have a positive impact on Hungary’s terms of trade, further supporting growth next year. For all these reasons, we expect growth to accelerate to 2.4% in 2027, with upside risks.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more