4.5% deficit is projected for 2025, and 5% for this year as goverment measures kick in

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

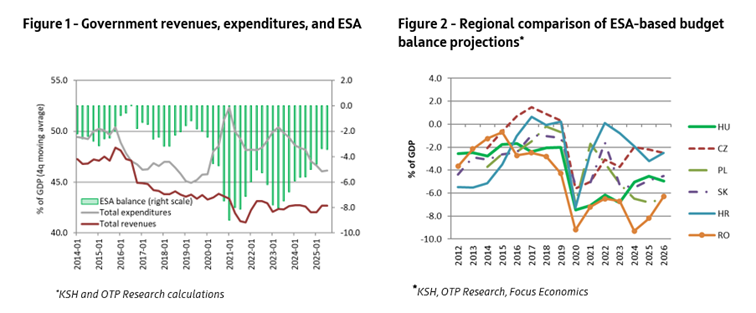

After many years of 7-8% deficit, an adjustment was made in 2024, despite the unfavourable macroeconomic environment. This brought the deficit down to 4-5% of GDP, which could be considered as an average level in regional comparison.

In Q3, the four-quarter deficit stagnated at 3.4% of GDP, supported by the surprisingly low deficit in Q2, which could result in a marginally lower figure (4.5%) for 2025 as a whole than the 5% deficit target, even in case of a really high deficit in the fourth quarter.

In 2026, even with the recently announced government measures, the 5% deficit target could be met due to lower interest expenses, and strict cost control in the case of operating expenses and investments.

Hungary's ESA-based fiscal deficit stagnated at 3.4% of GDP in 2025Q3, compared to 2025Q2 on a four-quarter (4Q)rolling basis, due to a 4.2% deficit in Q3 (Figure 1). This was 0.1 ppt lowerthan the 4.3% published in the financial accounts on the last day of 2025. Similarlyto the 4Q deficit, both the expenditure-to-GDP ratio and the revenue-to-GDPratio were unchanged. Compared to a year earlier, the 4Q deficit wasconsiderably down from 5.6% of GDP in 2024Q3, because of 2.1 ppts lowerexpenditures, and 0.1 ppt higher revenues.

Expenditures as a % of GDP on a 4Q basis were affected to the largest extent by lower interest expenditures (-0.3 ppts) and higher other expenses (+0.4 ppts). In the case of the latter, lower current and capital transfers in Q2 jumped back to the Q1 level, partly owing to budgetary expenditures related to state property, which was higher in Q3 following a lower level in H1, based on monthly cash-based data.

Investments declined by 0.2 ppts, while operating expenses were lower by 0.1 ppt compared to 2025Q2. On the other hand, subsidies were up 0.2 ppts, public wages increased by 0.1 ppt because of wage hikes in the public sector, partly financed by EU funds, and financial transfers were also 0.1 ppt higher, which could be partly explained by the food vouchers sent to pensioners. The remaining expenditure items were unchanged (Figure 3).

On the revenue side, taxes on production, income taxes, social security contributions and market output were up by 0.1 ppt on a 4Q basis, while other revenues were down by 0.2 ppts and interest income decreased by 0.1 ppt due to lower interest rates and the exceptionally high dividends in Q2. The remaining revenue items were unchanged (Figure 4).

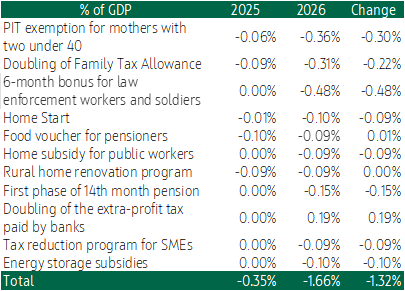

The government announced important measures, which have moderate effect on the deficit in 2025, but will have a bigger impact in 2026. Key among these are tax policy changes: PIT exemption for mothers of four children was extended to mothers of three from October 2025, and from January 2026 further extended to mothers of two under 40 years of age. The exemption will be gradually extended to all mothers of two children by 2029. From H2 2025, the family tax allowance was also raised by 50% and that will be increased again from the beginning of 2026, so that it will be doubled compared to H1 2025. A VAT refund for pensioners' fruits, vegetables, and dairy purchases was also announced but later that was substituted with a HUF 30,000 food voucher in 2025. We assume that food vouchers for pensioners will be maintained and adjusted for inflation in 2026. Last summer, the government also initiated a new subsidised program from September 2025 for home buyers, called Home Start. We assume that the program’s terms will be revised from the second half of 2026, so that budgetary expenses will be capped in the long run. Additionally, a new initiative starting in 2026 will provide public employees with HUF 1 million annual support for mortgage repayments or down payments, which we also expect to be tightened, alongside Home Start. The rural home renovation program, which is now available with looser conditions, is scheduled to end in June 2026. In our previous flash report we assumed that employers’ social security contribution rate will be cut by 1 ppt, which did not happen, but it turned out that the government will pay an extra week of pension in 2026 as the first phase of the 14th month pension, and cuts taxes for SMEs. On the other hand, the extra-profit tax on the banking sector was doubled. The government also announced a HUF 100 billion program in December to subsidise the installation of energy storage systems from January 2026.

We project that the deficit will be 4.5% of GDP in 2025, which is below the government’s current, 5% target.

In the third quarter, the budget ran 4.2% deficit, so the Q1-Q3 deficit was only 1.9% of GDP. Due to this, the 4.5% deficit can be reached even with a double-digit fourth-quarter deficit, which would be higher than the 8.2% in Q4 2024, so we decided to take the more conservative position following the trend of decreasing fourth-quarter deficits since 2023.

The measures that already had an effect last year will also widen the deficit in the last quarter of 2025. These include the 50% increase in the family tax allowance, PIT exemption for mothers of three from October, the launch of the Home Start program, food vouchers for pensioners, and the rural home renovation program. These measures cost around HUF 300 billion (0.35% of GDP) for the budget last year.

The deficit in 2026 is expected to increase to 5%, in line with the government’s latest target published in December. On the other hand, the government measures that increase household revenues will also heighten tax revenues through higher consumption. Strong wage growth in the private sector will also boost tax income, as well as the doubling of the extra-profit tax on the banking sector, announced in November, and interest expenses will decrease further in 2026 (by 0.2% of GDP), while the HUF 192 billion budgetary reserve was already locked for 2026 (0.2% of GDP). So, with strict cost control mainly in the case of operating expenditures and investments, the 5% government target is reachable.

In the case of EU funds, we assume that the agreement between Hungary and the EU will be further delayed,

meanwhile EUR 1 billion of EU funds were permanently lost at the end of 2024 and 2025. In addition, the dispute over the penalty between Hungary and the EU Court of Justice has not settled, and the European Commission has already started to deduct the penalty plus default interests from EU funds. In the case of the RRF funds, the tight schedule is a risk, as all projects must be finished before the end of 2026, otherwise a part or all the funds will be lost. On the other hand, the EU will launch the Security Action for Europe (SAFE) credit line as part of the ReArm Europe initiative, from which Hungary is expected to receive around EUR 16 billion preferential credit and the country may receive 15% of that in Q1 2026 as pre-financing if the National Defence Investment Plan is evaluated positively.

Table 1 - Effect of major government measures on the budget balance*

*OTP Research

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more