A 4.4% deficit is projected for this year, and 5.5% for 2026

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

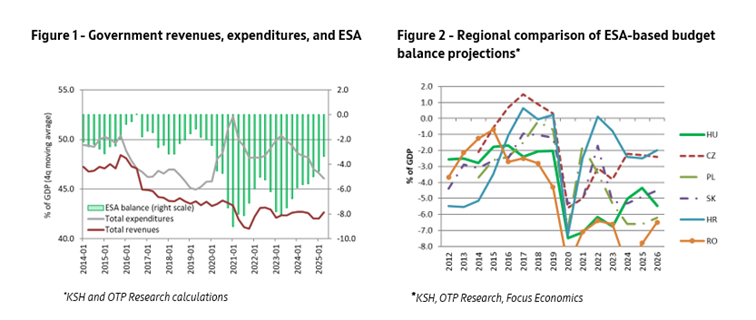

After many years of 7-8% deficit, an adjustment was made in 2024, despite the unfavourable macroeconomic environment. This brought the deficit down to 5% of GDP, still above the deficit target, which was increased from 2.9% to 4.5%. Thus, the deficit fell from a clearly high level to an average one in regional comparison. This year’s deficit is projected at 4.4% of GDP, within the latest deficit target range (4-4,5%) foresaw by the economy minister. Dividend and EU revenues were exceptionally high, and PIT and SSC income were also strong, while operating and other expenditures were under strict control. In 2026, recent government measures will have a much bigger effect (Table 1), deteriorating the deficit by 1.5%, but expected expenditure reallocations between 2025 and 2026 could lower the deficit. This suggests that Hungary’s deficit could be among the highest in the region, with only Poland and Romania expected to post larger shortfalls—both exceeding 6% of GDP.

Hungary's ESA-based fiscal deficit decreased to 3.4% of GDP in 2025Q2, from 4.6% in 2025Q1 on a four-quarter (4Q) rollingbasis, thanks to a 2.2% surplus in Q2 (Figure 1). This was the same as the finalfigure published in the financial accounts on the same day. The smaller 4Q deficit(compared to Q1) is caused by a lower (-0.6 ppts) expenditure-to-GDP ratio, anda higher revenue-to-GDP ratio (+0.6 ppts). Compared to a year earlier, the 4Qdeficit was considerably down from the 5.6% of GDP in 2024Q2, because of 2.3ppts lower expenditures, while revenues were unchanged.

Expenditures on a 4Q basis were affected to the largest extent by lower interest expenditures (-0.3 ppts) and other expenses (-0.4 ppts). In the case of the latter lower current and capital transfers could be partly explained by budgetary expenditures related to state property which was HUF 392 billion lower in H1 than a year ago, based on monthly cash-based data. Operating expenses were also down by 0.1 ppt compared to 2025Q1. On the other hand, public wages and investments were up by 0.1 ppt, the former because of wage hikes in the public sector, partly financed by EU funds The remaining expenditure items were unchanged (Figure 3).

On the revenue side, income taxes and social security contributions were up by 0.2 and 0.1 ppt as a % of GDP on a 4Q basis due to increasing real wages, other revenues were up by 0.2 ppts, while interest revenues increased by 0.1 ppt following five quarters of decline due to lower interest rates but higher dividends. The remaining revenue items were unchanged (Figure 4).

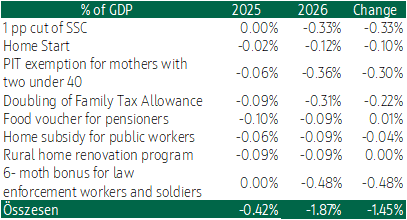

The government announced important measures this year which will affect the deficit in 2025 but will have a much bigger effect in 2026. Key among these are tax policy changes: PIT exemption of mothers of four children will be extended to mothers of three from October 2025 and extended to mothers of two under 40 years of age from 2026, and gradually to all mothers of two children by 2029. From H2 2025 the family tax allowance was also increased by 50% and that will be increased again from the beginning of 2026, so that it will be doubled compared to H1 2025. A VAT refund for pensioners' fruits, vegetables, and dairy purchases was also announced but later that was substituted with a HUF 30,000 food voucher in 2025, which has a lower cost for the budget. We assume that food vouchers for pensioners will be continued and adjusted with inflation in 2026. Since our previous flash report the government has initiated a new subsidised program from September 2025 for home buyers called Home Start. We assume that the program’s terms will be revised from the second half of 2026, so that budgetary expenses will be capped in the long run. Additionally, a new initiative starting in 2026 will provide public workers with HUF 1 million annually to support mortgage repayments or down payments, which we also expect to be tightened alongside Home Start. The employers’ social security contribution rate is likely to be cut by 1 ppt from the current 13%, following a request from the tripartite council (VKF), which the economy minister did not reject. This could be a condition for employers to accept a double-digit minimum wage hike in 2026. The rural home renovation program, relaxed in 2025, is scheduled to end in June 2026.

We project that the deficit will be at 4.4% of GDP in 2025, which is in the 4.0-4.5% range that Márton Nagy foresaw in an interview in September, but higher than the original 3.7% target. In the second quarter, the budget had a 2.2% surplus, so the H1 deficit was only 0.7% of GDP according to the Central Statistical Office, better than our expectation. Based on this, the deficit could be lower, but we expect that the government will reallocate some expenses from 2026 to this year to cushion the effect of the pre-election measures on the deficit – as there is a certain flexibility in accrual accounting to allocate certain revenues and expenditures between two periods. Operating costs increased slower than expected in Q2, so they are still under control which is now expected to be maintained this year given themodest increase so far. Interest expenses have fallen as expected, which willlower the deficit by 1 ppt this year compared to 2024. In case of otherexpenditures, instead of the previously expected rebound after the steep fallin Q4 expenses fell further, which suggests that at least part of the cutscould be permanent. EU revenues exceeded expectations in Q2 (HUF 751 billion ona 4Q basis vs. HUF 594 billion in Q1), although this likely contributed tostronger-than-expected investment growth. Income tax and SSC revenues remained strong,and interest and dividend income grew faster than we foresaw.

However, the deficit could widen in the second half of the year, as several government measures’ effect will kick in. These include the 50% increase in the family tax allowance, PIT exemption of mother of three from October, food voucher for pensioners, and the start of the Home Start program (which kicked off very strong based on the first couple of weeks’ data). These measures will cost around HUF 337 billion (0,4% of GDP) for the budget this year. Additionally, operating expenditures may accelerate, investments may begin to recover after the deep cuts, and other expenditures could partially rebound.

The deficit in 2026 is expected to be 5.5% much above the 3.7% target in the budget, given the measures which will have a significant effect in 2026. Most of the earlier mentioned programs will have a significantly bigger effect in 2026 than in 2025 (Table 1). We expect that the Home Start program will be tightened in the second half of next year, so the outflow will be reduced but it will still cost HUF 110 billion (0.1% of GDP) for the budget which will gradually increase in the next years. The 1 ppt cut of employers’ social security contributions will also reduce revenues by HUF 300 billion (0.3% of GDP). The extension of PIT exemption to mother of two below 40, and the second step of the doubling of the Family Tax Allowance will also have a major effect on the budget, as well as 6-month salary bonus for law enforcement workers and soldiers before the 2026 elections. So, all the measures listed in Table 1 will inflate the deficit by 1.45 ppt in 2026 compared to 2025. On top of that, wage hikes for teachers will continue and others (like judicial workers) will also get a raise, inflating the public wage bill further.

On the other hand, the government measures which increase household revenues will also increase tax revenues through higher consumption, and interest expenses will also decrease further in 2026. Strong wage growth in the private sector will also boost tax revenues, however, the size of the minimum wage hike will likely be renegotiated. Pensions will again increase at a lower rate than nominal GDP. Additionally, the previously mentioned expenditure reallocations will help to lower the deficit.

In the case of EU funds, we assume that the agreement between Hungary and the EU will be further delayed. Meanwhile EUR 1 billion of EU funds was permanently lost at the end of 2024, and a similar amount is likely to be lost at the end of this year. Plus, the dispute over the penalty between Hungary and the EU Court of Justice has not settled, and the European Commission has already started to deduct the penalty plus default interests from EU funds. Current EU transfers are expected to decline as the funds granted to wage hikes for teachers will be lower. In the case of the RRF funds, the tight schedule is a risk, as all projects must be finished before the end of 2026, otherwise a part or all the funds will be lost.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more