Uber could become a leading player in the robotaxi story

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Uber is a global leader in mobility and delivery services, the company generates stable cash flow and may achieve double digit growth over the coming years. The investment story, however, is increasingly defined by autonomous robotaxis — even though this trend is still in a very early stage and it is far from clear who the winners will be, or what the timeline is for profitability in this segment. In any case, we believe Uber is well positioned to be among the long term winners. As autonomous driving could become one of the hottest capital market themes of 2026, we add Uber’s stock to our Equity Top Pick List.

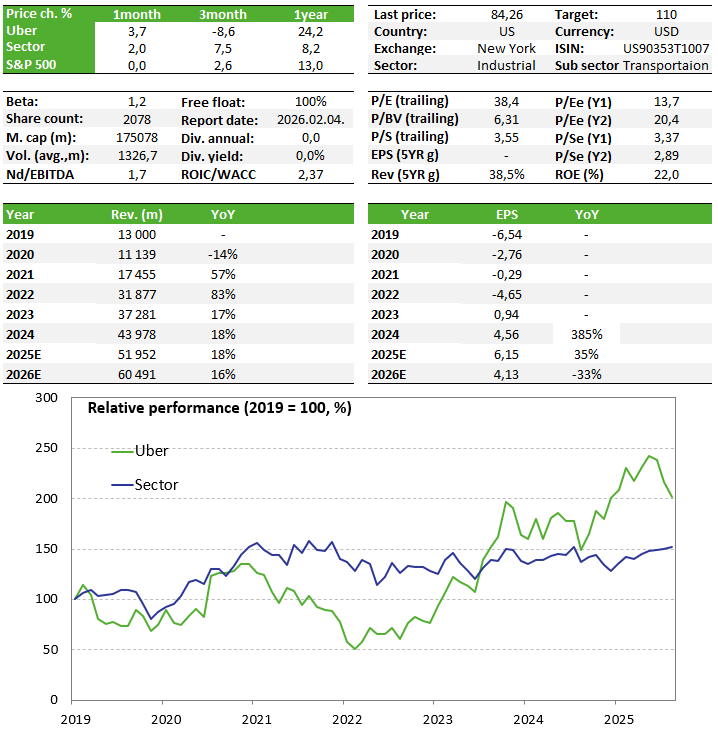

Company overview

Uber is a global mobility platform offering ride hailing, food and other delivery services, and to a smaller extent, freight related logistics. Headquartered in San Francisco, the company operates in over 70 countries and more than 900 cities, with more than 180 million monthly active users. Over the past year, Uber has entered into several strategic partnerships to bring autonomous vehicles onto its platform and has made investments in autonomous vehicle technology, positioning itself as an essential player in this emerging market.

Financial Position and Valuation

The majority of Uber’s revenue (close to 60%) comes from mobility services (essentially the ride hailing business). For each trip completed on the platform, Uber retains roughly 30% of the fare after compensating drivers, a figure commonly referred to as the net take rate. From this amount, the company must still deduct insurance, marketing, and other operating expenses. A similar economic structure applies to the Delivery segment, although its net take rate is lower, typically in the range of 18–19%.

The third business line is Freight, which connects carriers with shippers. This segment is not considered strategic and has reported negative EBITDA in recent periods. A divestiture could therefore be strategically justified; however, no such plans have surfaced, even at the level of market speculation, in recent months.

Analysts’ expectations are solid for Uber: low double digit growth in gross bookings over the next five years and revenue expanding by close to 13% annually. Profitability is expected to improve similarly. The company’s leverage is low, and it generates significant free cash flow — forecast at above USD 10 billion per year in the coming years.

Uber One, the company’s subscription program, is a key focus area aimed at improving user loyalty and providing more stable recurring revenue. Uber One currently has 36 million subscribers, generating about one third of total bookings, although the company does not disclose specific revenue figures.

Advertising is also becoming an important revenue stream. This business was launched around 2022 and may have reached USD 1.5 billion in annual revenue in 2025 — representing roughly 60% YoY growth. The large user base and data driven targeted advertising provide further upside potential.

Valuation is not high relative to other tech sector names: the 2026 P/E ratio is around 23, and the EV/EBITDA multiple is about 16, with expected earnings growth of around 20%.

Investment Thesis

Both the mobility and food-delivery markets are long-term structural growth industries in which Uber maintains a leadership position while delivering robust profitability. However, the primary investment catalyst in the near and medium term is expected to be the development and commercialization of autonomous robotaxi services, a technology that has the potential to fundamentally reshape road transportation.

Throughout the past year, Uber’s share price was driven largely by news flow related to autonomous-driving progress. The stock tended to appreciate following announcements of new partnerships or service launches by Uber, while updates from key competitors such as Waymo or Tesla often exerted downward pressure. Given that robotaxi penetration remains in its infancy, it is difficult to determine the eventual winners or assess how many industry participants will ultimately be able to generate meaningful profits. What is clear, however, is that autonomous driving is poised to remain a prominent capital-market theme for the foreseeable future.

Uber does not develop autonomous-driving technology in-house, nor does it manufacture vehicles. Instead, its core contribution is its platform: a global network of more than 180 million monthly active users, enabling adoption at considerable scale with significantly lower capital requirements. Uber currently collaborates with Waymo in markets such as Atlanta, Phoenix, and Austin. In larger metropolitan areas such as San Francisco and Los Angeles, however, Waymo operates exclusively on its own platform. Consequently, there is some strategic risk that Waymo, if it continues to scale independently, may limit future cooperation.

Tesla is similarly unlikely to partner with Uber. Elon Musk envisions autonomy within a closed Tesla ecosystem, whereby Tesla owners deploy their vehicles as robotaxis when not in use, and customers subscribe directly to Tesla’s services. Should the fully autonomous, steering-wheel-less Cybercab move into production, questions would arise regarding fleet ownership, deployment, and operational responsibilities. Nonetheless, such developments are unlikely to become material drivers in 2026.

Uber has proactively expanded its autonomous strategy. Last summer, the company entered partnerships with Lucid (carmaker) and Nuro (autonomous technology), committing to purchase at least 20,000 Lucid Gravity robotaxis over a six-year horizon, to be owned either by Uber or its fleet partners. This indicates a strategic intent not to rely exclusively on external service providers.

Uber has additionally signed agreements with Nvidia and Stellantis, although vehicles associated with these collaborations are expected to enter the market only around 2027–2028. Further partnerships include Volkswagen, Avride, and May Mobility in the U.S., as well as international collaborations with WeRide in Abu Dhabi, Riyadh, and Dubai; with Pony.ai in the Middle East; and with Baidu in Asia, although detailed project plans have not yet been disclosed.

The long-term economics of autonomous robotaxi fleets remain uncertain. This ambiguity has contributed to the stock’s decline in recent months, with shares now trading near levels last seen in the spring. While the shift to autonomy eliminates driver compensation, it introduces substantial depreciation costs related to vehicles and technology, as well as ongoing fleet-management expenses (fuel, cleaning, maintenance, operations, etc.), all borne by the operator. As such, autonomous taxi services are unlikely to be profitable within the next one to two years.

Despite these uncertainties, we believe Uber is well-positioned to emerge as one of the long-term winners in the robotaxi market. The company’s considerable scale enables rapid expansion of autonomous services once commercially viable, while its foundational business segments are expected to maintain compelling growth trajectories. Accordingly, we add Uber to our Equity Top Pick List.

Key Risks

- A slowing economy or weakening consumer demand could reduce usage across core operations.

- Adoption of autonomous robotaxis may take longer than expected, and intense competition could erode profitability.

- Regulatory or safety concerns may hinder the rollout of autonomous vehicles.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more