Uber: Still in the Fast Lane

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

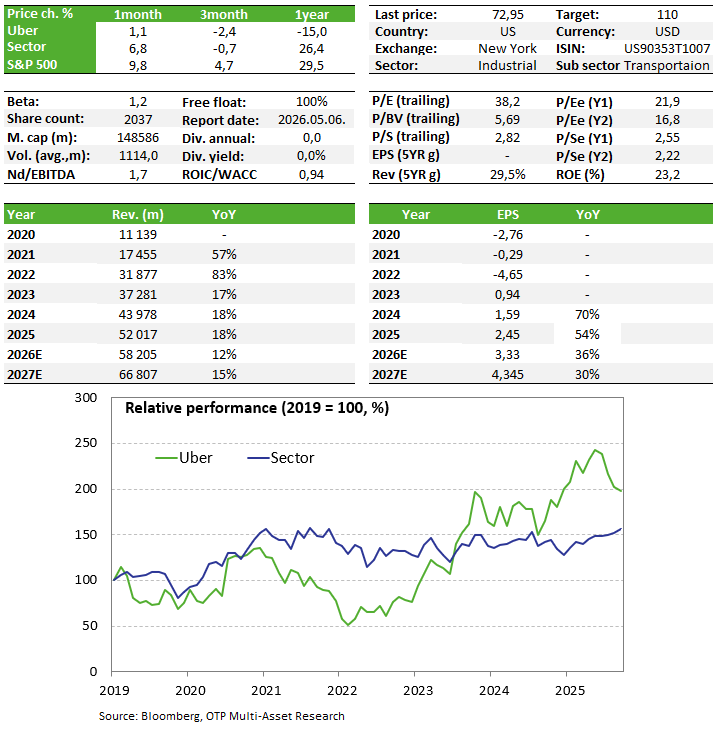

Uber’s quarterly results reinforced the view that the company’s growth and profitability story remains firmly intact. Investors focused primarily on stronger-than-expected gross bookings, robust trip growth, continued adjusted EBITDA expansion, and favorable guidance for the second quarter. The key message from the report is that Uber is no longer merely a mobility platform: the delivery business is increasingly emerging as a second meaningful profit pillar, while autonomous vehicles may represent a longer-term growth opportunity.

Uber shares remain on our Equity Top pick List.

Earnings Report

Uber’s Q1 report carried an overall positive message for equity investors. Although revenue came in slightly below consensus, gross bookings exceeded forecasts, trips increased by 20%, and adjusted EBITDA rose by 33%. Management also raised its gross bookings guidance for the current quarter. The share price reacted positively to the news.

In the Mobility segment, gross bookings increased by 25% to USD 26.4 billion. Revenue, however, rose by only 5% to USD 6.8 billion, falling short of the USD 7.1 billion consensus. That said, the company indicated that much of the divergence between gross bookings and revenue was attributable to a business model changes and possible adjustments in the take-rate structure. This interpretation is supported by the fact that segment operating profit increased by 28% to USD 2 billion, indicating that profitability remains very strong. If the company were facing genuine pricing pressure or a demand issue, operating profit would likely have been materially weaker as well.

In the Delivery segment, gross bookings increased by 28% to USD 26 billion, while revenue grew even faster, rising 34% to USD 5.07 billion. Operating profit expanded by 43% to USD 961 million. This is strategically important, as the Uber investment case was previously predominantly centered on Mobility, whereas Delivery now represents a demand pillar of almost comparable scale. Margins are admittedly lower in this business, but at the group level there is no evidence of profitability deterioration — quite the opposite. Delivery growth was particularly strong in Australia, Japan, and the United Kingdom, suggesting that the growth story is not solely dependent on the U.S. consumer, but is increasingly geographically diversified.

Another important driver has been Uber One. The membership program reached 50 million members, and members now account for roughly half of gross bookings and orders. This is especially important for Delivery, as the subscription model increases order frequency, improves customer retention, and may reduce customer acquisition costs over the longer term. There was limited new information regarding autonomous driving. The company had previously confirmed that it aims to launch in 15 new cities with various partners by the end of this year. Target markets include London, Zurich, Madrid, Munich, Los Angeles, and Hong Kong.

Investment story

- Uber is the world’s largest mobility platform, with 200 million monthly active users, and has already demonstrated that it can generate sustainable free cash flow while continuing to grow. Both Mobility and Delivery operate in structurally growing markets, where Uber holds a leading global position.

- The Uber One program increases user engagement and helps stabilize revenue. Advertising revenue is already at a multi-billion-dollar run-rate, generates high margins, and still offers meaningful additional growth potential.

- Uber is not developing autonomous-driving technology in-house; rather, it provides the demand layer and the platform. As a result, it assumes less capital intensity and technological risk than many competitors. If robotaxis become economically viable, Uber could be one of the most scalable beneficiaries.

- Main risks: The core business could be affected by weaker demand in the event of a slowing economy and softer consumer spending. The adoption of autonomous taxis may take longer than expected, while intense competition could also pressure profitability. Regulatory or safety-related issues could hinder the broader rollout of autonomous vehicles.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more