Semiconductors: How far out of touch with reality were we in April?

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

The U.S. semiconductor sector posted a spectacular outperformance in April, with the rise in share prices supported by a combination of strong fundamentals and an improving risk environment. The rally was driven by a significant upward revision of earnings expectations and a favorable news flow, while valuations returned to levels around the historical average of recent years. However, due to elevated positioning and heightened expectations, some profit-taking cannot be ruled out in the short term, even if the longer-term investment outlook remains supportive thanks to strong fundamentals. The next significant catalyst could come from the earnings reports released by major technology companies this evening, where the focus may be on capex levels, their financing, and returns, which could determine the sector’s short-term direction for the coming days and weeks.

Semiconductors emerged as the market leaders in April; while the technology sector as a whole posted more modest gains in the first three months of the year — even though chipmakers managed to rise during that period — the magnitude of those gains fell short of the momentum seen in April (+40%). The Philadelphia Semiconductor Index (SOX) has closed in positive territory for 18 consecutive trading days this month, which can be considered an unprecedented historical record. There may be several reasons for this rally, one of which is favorable news flow. Over the past month, all players in the U.S. semiconductor sector have shown positive news sentiment, which may have contributed to the extremely broad-based rally.

In addition, several earnings reports came in from segments of the industry that had previously been considered laggards but now posted excellent results, which helped broaden the rally. One such example was Texas Instruments, whose stronger-than-expected growth boosted all analog chip manufacturers (we wrote about this segment in our previous industry overview here), which had previously been left out of the cycle driven by AI data center investments. Although the market had already begun to price in a turnaround for Intel in the last half-year, this is now showing up in the numbers for the first time. The CPU market, which had also been underperforming in the early stages of the AI cycle, thus received another positive boost, which not only supported Intel’s stock price but also had a favorable impact on the performance of other players in the segment — such as AMD and Arm.

Despite the favorable news flow and positive earnings reports, analysts’ profit expectations have shown only a moderate increase over the past month, with 2026 EPS estimates rising by 3.1% and 2027 expectations by 4.2%. Accordingly, the recent rise in stock prices was driven less by current earnings momentum. At the same time, it is important to note that significant positive revisions to profit forecasts have already occurred over the past three months (2026: +34.3%, 2027: +40.9%), meaning that the improvement in fundamentals had already begun prior to April.

However, these changes have not yet been reflected in prices due to the heightened volatility and risk-averse investor sentiment that characterized the month of March. Starting in early April, diplomatic talks between the U.S. and Iran eased fears regarding geopolitical risks in the Middle East, which, through increased risk appetite, ultimately triggered a capital inflow toward the U.S. semiconductor industry — a sector characterized by higher risk but favorable fundamentals.

Following significant upward revisions to profit forecasts, the market is currently pricing in a strong growth trajectory for the semiconductor sector. Based on the analyst consensus, earnings growth of approximately 85% is expected on average over the next four quarters, compared to the roughly 48% growth realized over the past four quarters. At the same time, revenue growth is also expected to accelerate significantly: forecasts project revenue growth of around 56% in the coming quarters, up from the previous rate of nearly 30%.

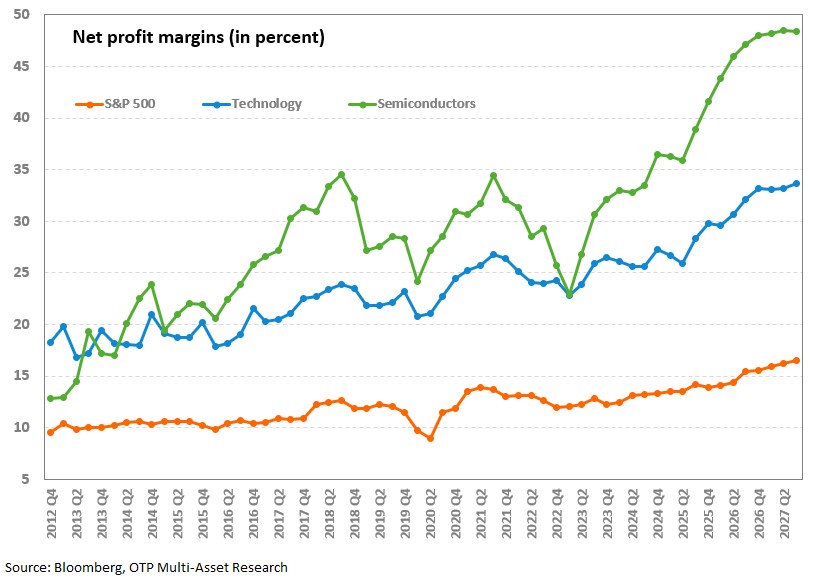

Improving profitability could further reinforce these favorable fundamental trends, as the current net profit margin — which stands at a record-high ~44% — could rise to as much as 48% within a year. This level significantly exceeds the average profitability of both the broader technology sector (~30%) and the S&P 500 index (~14%), which represents the U.S. market, further reinforcing the sector’s relative investment appeal.

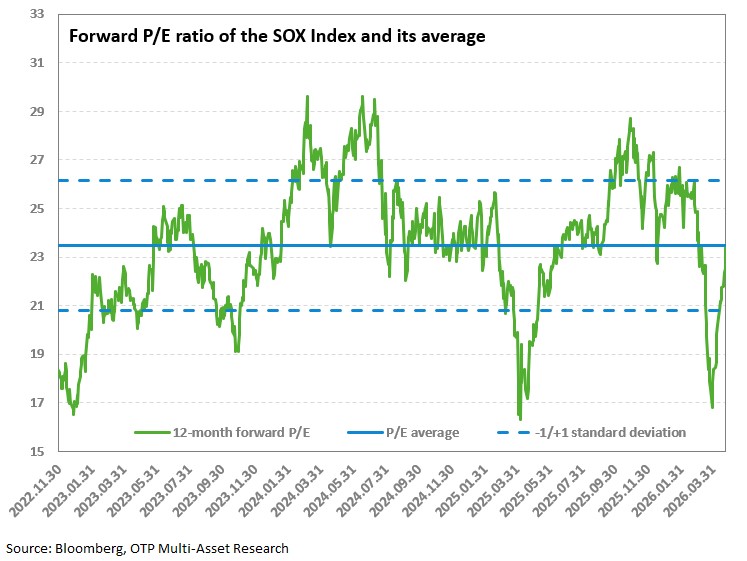

As for valuations, by the end of March, the forward P/E ratio of the Philadelphia Semiconductor Index (SOX) had fallen to 17, a level seen only once in the past three years—more than a year ago, following the tariff measures announced on “Liberation Day.” The semiconductor industry, which has a particularly strong fundamental backdrop, thus offered highly attractive valuation levels following the market correction, justifying its inclusion among the favoured investment topics in our Q2 Investment Outlook.

As a result of the sharp rise in stock prices in April, the index’s valuation has returned to levels consistent with the historical average over the approximately 3.5 years since the AI boom began (the launch of ChatGPT), however, current valuations still cannot be considered excessive, especially in light of expected earnings growth. Nevertheless, from this point on, valuations will be less supportive of further gains.

By the end of April, positions in the semiconductor sector had become overcrowded, which could even trigger profit-taking in the short term. Although valuation metrics are not considered excessively high on their own, the associated future revenue and earnings expectations already reflect significant optimism. The biggest source of uncertainty, therefore, is the extent to which the profit growth currently priced in proves sustainable. From this perspective, the earnings reports of hyperscale technology companies, set to be released after the market closes today, will be crucial, with the focus likely to be on return on investment, potential growth acceleration, and free cash flow generation, in addition to capex data.

A key question may be whether these companies are able to finance further AI-related investments using internal resources. Upcoming earnings reports could be decisive for the sector’s short-term performance in the coming days and weeks, though the longer-term investment outlook may remain supportive thanks to strong fundamentals.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more