Palo Alto: AI is more of an opportunity than a risk

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

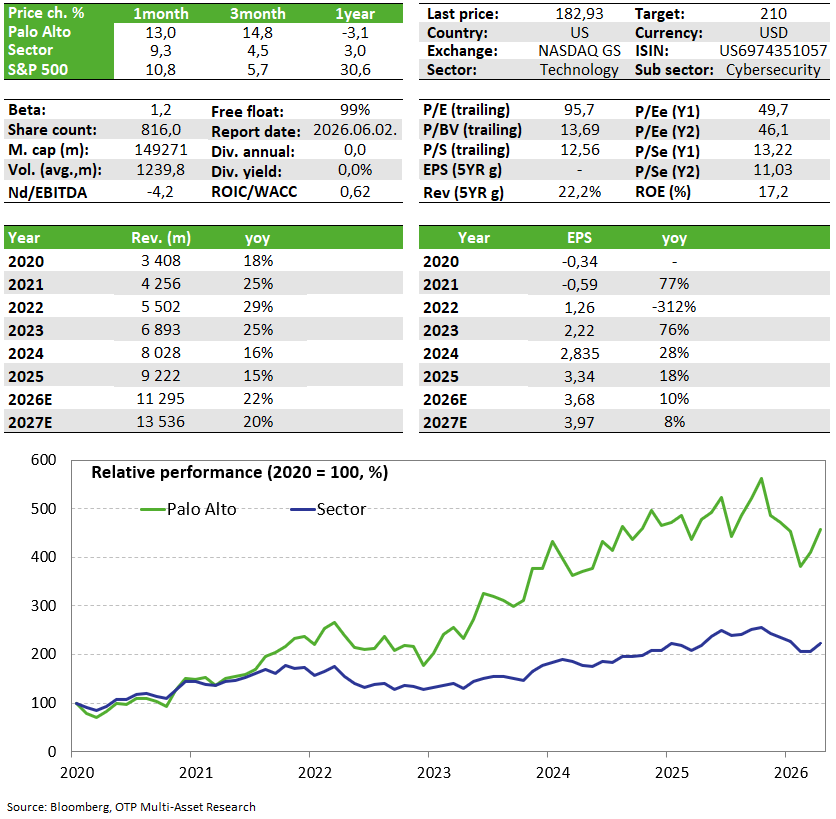

The software sector underperformed the technology sector this year due to fears surrounding AI disruption, even though the market had made little distinction between potential AI winners and losers at the beginning of the year. In our view, however, key segments of cybersecurity — such as network security, endpoint protection, and identity security — may be structurally more resilient to the impacts of AI. Palo Alto holds a dominant market position in these segments, a position further strengthened by its collaboration with Anthropic. Furthermore, following the acquisition of CyberArk, the company stands to benefit from the spread of AI agents, meaning that AI is likely to have a demand-stimulating effect. In our view, the market has so far priced in the risks, while the structural advantages have remained undervalued; therefore, we are adding Palo Alto shares to our Equity Top Picks list.

Company Overview

Palo Alto Networks is a leading player in the global cybersecurity market, offering AI-powered security solutions to protect networks, clouds, endpoints, and security operations. Its solutions are used by more than 80,000 enterprise customers worldwide, while its revenue is heavily concentrated in the U.S., which accounts for approximately 65% of total revenue. 80% of revenue comes from subscription services, while one-time hardware sales (~20%) typically serve as an entry point to longer-term software and cloud subscriptions.

The company holds a leading market position among providers of pure-play cybersecurity services, with a market share of approximately 4–5%. The industry is highly fragmented: only ten players hold at least a 1% market share, indicating potential for consolidation. Accordingly, there is brisk acquisition activity in the sector, from which Palo Alto can benefit due to its size, scalable platform model, and strong net cash position. The company ranks among the leading players in all critical cybersecurity segments — network security, endpoint protection, and cloud security—while, following the acquisition of CyberArk, it has also established a strategically significant position in the identity security market.

In the summer of 2025, the company announced the acquisition of CyberArk, a leading player in the identity and access management market, covering a strategically important segment where Palo Alto previously had no significant presence. The financial closing of the acquisition is expected in the current fiscal year, which will support revenue growth in the short term but may temporarily put pressure on margins of about 2–3 percentage points due to integration costs. Identity security could play a key role in protecting AI agents, while the integration of CyberArk could open up significant cross-selling potential for Palo Alto. All of this could result in substantial value creation in the longer term, although the acquisition also carries execution and operational risks in the short term.

Investment case

Palo Alto benefits from all major, long-term structural technology trends — including platformization, the spread of cloud-based IT architectures, artificial intelligence, and quantum technology. Its competitive advantage is supported by an extensive enterprise customer base, strong distribution channels, one of the market’s broadest and most integrated security platforms, and its leading market position.

The company is particularly well-positioned in key growth segments, such as the SASE (Secure Access Service Edge) solutions market, which is benefiting from the rapid expansion of demand for cloud-based networking and edge security systems. Palo Alto’s platform strategy deliberately focuses on enterprise customers, promoting deeper integration and long-term customer retention, which also significantly reduces the likelihood that its solutions could be easily replaced—even through AI-based automation.

Based on our current understanding of the company’s product and service portfolio, only a marginal portion of it is likely to be directly exposed to the potentially disruptive effects of artificial intelligence. Even in these areas, a collaborative approach to development appears to be emerging, as indicated, for example, by Anthropic’s Glasswing project and developments surrounding the Mythos model. In light of this, it cannot be ruled out that Palo Alto will eventually integrate Anthropic AI’s solutions into its existing product portfolio, which could even support further growth in demand.

In addition, the company has a particularly strong presence in the field of AI agent security, especially following its acquisition of CyberArk. Through this acquisition, Palo Alto has integrated one of the most significant players in the identity and access management market into its ecosystem, providing a strategic advantage in the future protection of autonomous and AI-based systems.

Taking all of this into account, we are adding Palo Alto shares to our Equity Top Pick list.

Valuation and Debt Level

The growth outlook is in line with that of its direct competitors: for the 2026–2028 period, the analyst consensus forecasts average annual revenue growth of approximately 19% and FCFF growth exceeding 20%. What stands out are the margins and FCFF, and there is room for further expansion on this front in the coming years following acquisitions.

In the software sector, the so-called “Rule 40” figure is of particular importance; it is calculated as the sum of revenue growth and the FCFF margin, and companies that achieve a value above 40 over the long term outperform their competitors. Palo Alto has an outstanding value of over 50, which is expected to remain sustainable in the medium term as well. All of this may justify a premium valuation — the company is currently trading at higher multiples compared to its competitors, yet a moderate discount can be observed relative to its own historical averages. In addition, the company has a net cash position.

Key risks

One of the primary structural risks affecting the cybersecurity sector as a whole is the rise of artificial intelligence, which has the potential to transform industry business models and dampen long-term growth, margins, and predictability. Palo Alto currently holds strong positions in segments that are relatively more protected from AI, such as network security, endpoint protection, and identity security. However, if AI-based solutions were able to meaningfully enter these markets and offer alternatives, it would result in increased competition and declining margins.

Another risk factor is that, in the current market environment, investors are still making only limited distinctions between potential AI winners and losers within the software sector; as a result, negative news could trigger a decline in the stock price for all software companies. It is also worth mentioning the integration risks arising from the acquisition of CyberArk.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more