Palantir: Another Outstanding Quarter

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

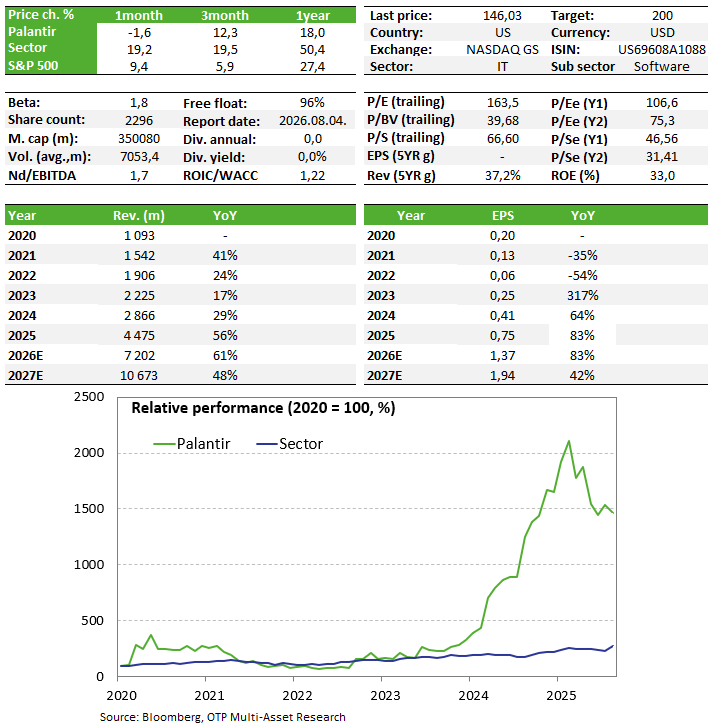

Palantir delivered yet another exceptionally strong quarter. The company not only posted robust revenue growth and outstanding profitability, but forward-looking contract metrics pointing to future revenues also improved materially. The results reaffirm that Palantir’s U.S. business — particularly enterprise AI adoption — remains on a very strong growth trajectory. While higher guidance inevitably raises market expectations, Palantir continues to offer a rare combination of rapid growth, high margins, and strong cash generation.

Palantir shares remain on our Equity Top pick List.

Quarterly Report

Palantir once again reported an outstanding quarterly performance. Revenue increased 85% year-on-year to USD 1.63 billion, the highest level since the company’s IPO, while adjusted operating margin reached 60%. Beyond headline revenue, forward-looking indicators also strengthened significantly. Remaining Deal Value (RDV) — the value of signed contracts not yet billed — rose to USD 11.8 billion, up 98% year-on-year. Remaining Performance Obligations (RPO) surged 134% year-on-year to USD 4.5 billion, further underscoring strong demand visibility.

The company generated USD 871 million in GAAP net income, implying a 53% net margin. In other words, Palantir is achieving extraordinary growth without sacrificing profitability: accelerating revenues are translating directly into net income and free cash flow.?

The U.S. segment continues to be the main driver of the investment thesis. U.S. revenue grew 104% year-on-year to USD 1.28 billion, accounting for approximately 79% of total revenue. U.S. commercial revenue surged 133% to USD 595 million, while U.S. government revenue increased 84% to USD 687 million. The commercial segment is particularly important, as a key historical question around Palantir was whether it could evolve beyond its government-centric roots into a scalable enterprise AI platform. The Q1 2026 results clearly suggest that it can.

Management raised full-year 2026 revenue guidance to USD 7.65–7.662 billion, well above the USD 7.245 billion consensus estimate. On the U.S. commercial front, management now expects more than USD 3.224 billion in revenue for 2026, implying at least 120% growth. This is a powerful signal, indicating that enterprise AI adoption in the U.S. is not slowing but accelerating further.

That said, higher guidance also brings higher expectations. From here, the market will demand sustained strength in U.S. enterprise growth alongside stable government demand. The negative post-market reaction suggests that some investors believe a meaningful portion of the good news may already be priced in.?

Palantir does not position itself as an AI model developer, but rather as an operating layer that enables AI to be deployed effectively in large-scale enterprise and government environments. According to CTO Shyam Sankar, declining inference costs are not a threat but a tailwind: as AI becomes cheaper, organizations will want to automate more workflows — but doing so requires control, auditability, and a trusted platform. Under Palantir’s narrative, cheaper AI does not undermine the business model; instead, it increases the value of platforms such as AIP that sit at the intersection of AI, operations, and governance.

Investment story

- Palantir offers a direct way to gain exposure to the AI momentum. Over the next four years, consensus expectations point to 30–40% average annual growth in both revenue and profits. The company operates with net margins above 40%, generates strong free cash flow, and holds a net cash position.

- If Palantir can retain its dominant position in the government sector while continuing to scale meaningfully in the commercial space — something it has demonstrated so far — elevated valuation multiples could persist for an extended period. In an optimistic scenario, rapid earnings growth could quickly compress valuation metrics even without a share price correction.

- Key risks: The primary risk remains valuation. The stock is priced at extremely high multiples, meaning that any shortfall versus growth expectations could trigger a sharp correction. In a broader risk-off environment, a 40–50% drawdown cannot be ruled out.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more