Novo Nordisk: Relief Rally or Real Turning Point?

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

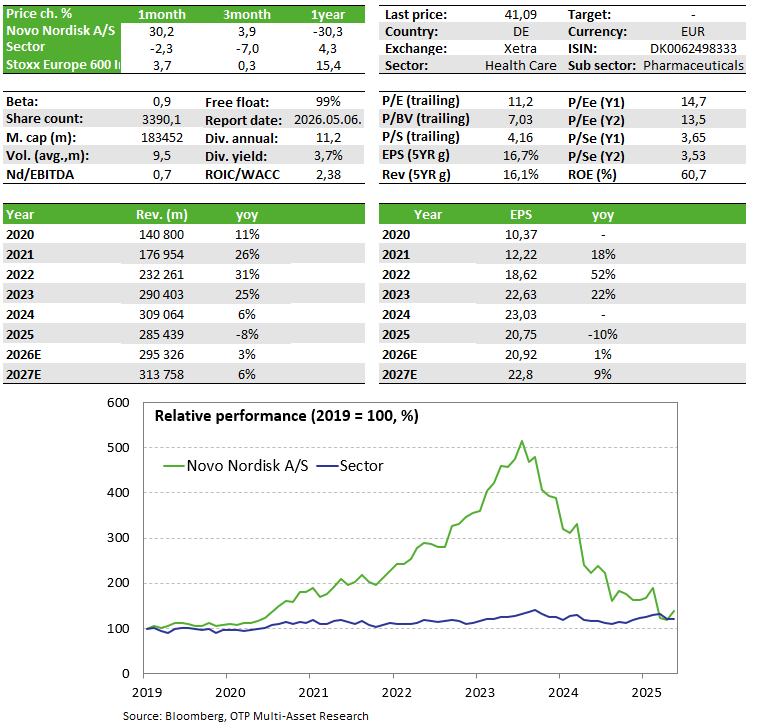

The Danish pharmaceutical company reported quarterly numbers ahead of subdued expectations and slightly improved its 2026 outlook. While the headline figures were flattered by a one-off accounting item, the strong U.S. launch of oral Wegovy is an important positive signal for the market. The key question now is whether this marks the beginning of a genuine turning point after the disappointment earlier this year, or merely a temporary relief rally in a story that remains under pressure.

Novo Nordisk shares remain on our Equity Top pick List.

Earnings Report

Novo Nordisk’s Q1 report may provide investors with some relief, as the share price was up more than 7% intraday on the back of better-than-expected numbers. The stock had performed particularly weakly since February, when the company’s previous earnings report came as a major negative surprise to investors. Following that disappointment, expectations had already been reset materially lower, making it easier for the company to clear the lowered bar.

Revenue increased by 32% at constant exchange rates to DKK 96.8 billion, while operating profit rose by 65% CER to DKK 59.6 billion. At first glance, these are very strong numbers, but they include a sizeable one-off item. The item relates to a U.S. drug-pricing discount program that provides certain healthcare institutions with discounted drug prices. Novo Nordisk had previously booked a substantial provision for potential future rebates, discounts or revenue-reducing adjustments. This provision has now been reversed. Excluding this effect, revenue declined by 4% year-on-year, while adjusted operating profit fell by 6% to DKK 32.9 billion. Even so, operating profit still exceeded expectations, as the Reuters analyst consensus stood at DKK 28.74 billion.

The main area of pressure remains the U.S. market. Adjusted revenue from U.S. operations declined by 11%, mainly due to lower realized prices, although this was partly offset by GLP-1 volume growth. The international business performed better, with revenue increasing by 6%. The most important positive was the U.S. launch of oral Wegovy. The product generated Q1 revenue of DKK 2.26 billion, well ahead of the DKK 1.16 billion expected by the market, representing a meaningful beat. Prescriptions for oral Wegovy reached 1.3 million in Q1, and have already exceeded 2 million since launch. In the week ending April 17, weekly prescriptions surpassed 200,000, marking Novo’s strongest-ever weekly figure in the U.S. This was achieved even as Eli Lilly’s oral weight-loss drug became available from April. This is strategically important because the oral format could expand the overall market. Many patients remain reluctant to use injectable therapies, while a tablet formulation may improve penetration and access. That said, Q1 also included pre-launch inventory stocking by wholesalers and other partners, so the quarterly revenue figure should not be mechanically annualized.

Revenue from injectable Wegovy increased by 12% year-on-year, although this was slightly below consensus expectations. Ozempic revenue declined by 8%, but still came in ahead of expectations. Ozempic will also become available in tablet form from May across different dosages, approved for type 2 diabetes. Novo Nordisk slightly improved its 2026 guidance, but the change is modest: the company now expects adjusted revenue and adjusted operating profit to decline by 4–12%, compared with the previous guidance range of a 5–13% decline. This does not represent a radical change in the outlook.

For now, we are keeping Novo Nordisk on our Equity Top Pick List. The Q1 results could potentially mark a turning point, as Wegovy has had a strong start, markets outside the U.S. continue to show growth, and management has upgraded guidance. The key question is whether these factors can support a sustained share-price recovery, or whether they merely provide temporary relief. If growth in oral Wegovy normalizes quickly, pricing pressure intensifies, or injectable Wegovy and Ozempic continue to deliver mixed performance versus expectations, the market could once again punish the stock.

Investment story

- Following the organizational restructuring and layoffs launched last year, it will likely take several more quarters for the changes to fully feed through. The reorganization process may take longer than expected.

- The rollout of oral Wegovy, which started this year, has so far ramped up quickly and could provide an additional growth leg. The higher-dose 7.2 mg injectable version of Wegovy is also under regulatory review, which could further expand the addressable patient population. CagriSema has not failed outright, but the data have fallen short of expectations, meaning it is unlikely to become the game-changing product investors had hoped for.

- The share buyback program may provide some support for the share price, but it is unlikely to be a decisive catalyst. In addition, Novo Nordisk could expand its portfolio through targeted acquisitions, which, in a favorable scenario, may also help improve market sentiment.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more