Micron reports blowout results

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

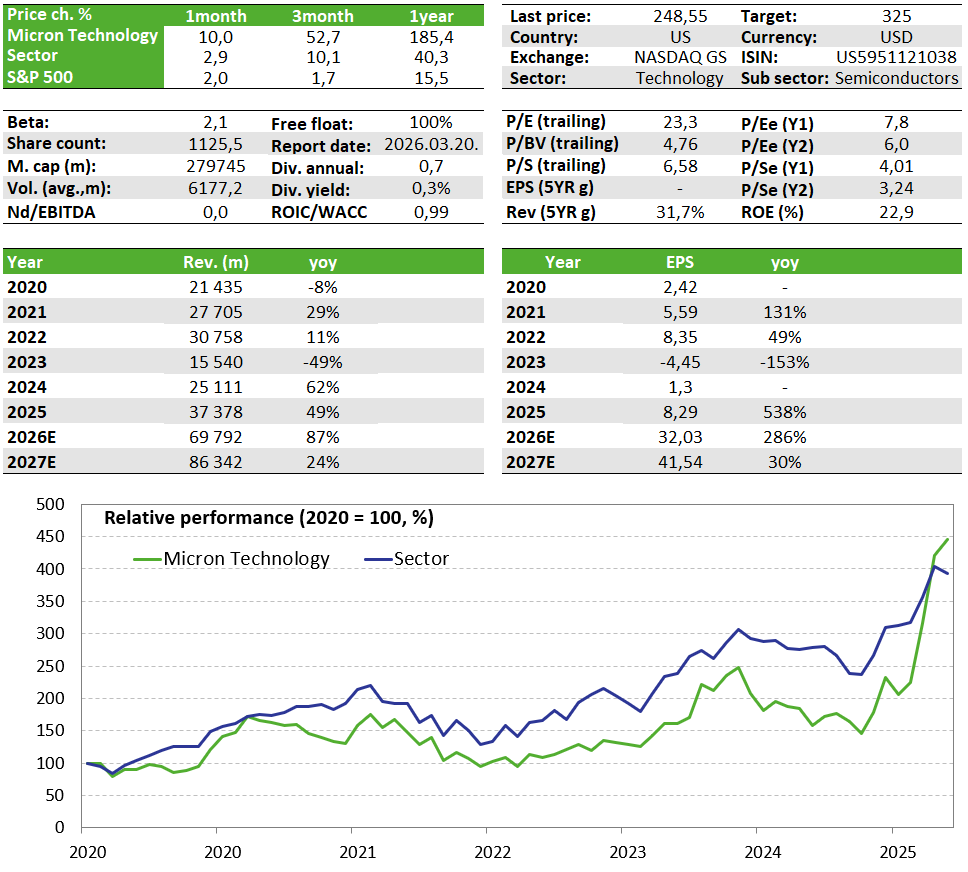

On Wednesday, Micron Technology, the leading US memory chip maker, published its quarterly figures, which exceeded analysts' estimates in terms of both revenue and profit. Furthermore, the company gave a execptionally strong forecast for the current quarter, primarily due to insatiable demand for its products, suggesting that memory chips may have become a bottleneck in the AI value chain. This demand dynamic is expected to continue in the near future, which should continue to create favorable conditions for the company to maintain its pricing power and revenue growth trends. We continue to view the fundamentals of this stock, which is also included in our Equity Top Pick List, as strong, and are therefore raising our fair value estimate from $200 to $325.

We continue to maintain Micron on our Equity Top Pick List

Quarterly earnings report

This fall, Micron's stock nearly doubled in value, making it one of the best performers on the US market. The company, which has evolved from a cyclical memory chip manufacturer into a critical player in AI infrastructure, continues to enjoy the structural growth opportunities offered by the artificial intelligence megatrend. This is reflected in the company's earnings report, with revenue reaching $13.64 billion for the quarter (+57% YoY), exceeding analysts' estimates of $12.95 billion. AI-related revenue accounted for more than 56% of total revenue.

In terms of profit, the company reported adjusted EPS of $4.78 (+167% YoY) compared to expectations of $3.95. The main drivers of this dynamic growth were the continued strong demand for high-bandwidth memory (HBM) chips needed in data centers and the price explosion of less sophisticated memory chips needed PCs and smartphones. The latter phenomenon is due to industry players focusing on the production of higher-margin HBM products, which is causing an increasing shortage in the market for more traditional memory products.

In addition, the chip maker provided excellent guidance for the current quarter, which calculates revenues 30% higher than the market consensus and includes an EPS forecast of $8.42 instead of the expected $4.71 (~80% positive surprise), which would represent an increase of nearly 500% compared to a year ago. Moreover, management expects a gross margin of 68% (analyst expectations are 55.7%), which points to further improvement in pricing power due to favorable supply-demand conditions.

Although the company has increased its capex for fiscal year 2026 from $18 billion to $20 billion in an attempt to increase manufacturing capacity, supply shortages are likely to remain beyond 2026, while demand continues to be strong. According to the CEO, Micron is only able to fulfill 50% to 67% of orders from several key customers. Furthermore, the company has already sold out its entire HBM inventory for fiscal year 2026. In the long term, the company expects the current $35 billion HBM market to reach $100 billion by 2028 (with Micron's share of this market at ~20-25%), which is still considered a conservative estimate.

Since adding Micron Technology to our Equity Top Pick List a little over three months ago, the stock has gained nearly 100%. However, as the only US-based memory chip manufacturer, the company remains uniquely positioned to capitalize on the opportunities offered by artificial intelligence. Given the favorable industry trends and strong growth outlook, we are maintaining the company's stock on our list and raising our target price to $325 from $200.

Valuation

The company's operating margin is around 50%, while its EBITDA margin is over 60%, both of which are among the highest in the industry. It is also one of the best memory chip manufacturers in terms of growth, with revenue growth of over 87% and EPS growth of nearly 255% forecast for fiscal year 2026. Despite this, its shares are trading at a discount to the industry average (2026 P/E of 8.7, while EV/S is 3.8). Based on indicators, the share price of $325 also seems fair. The company's debt is not significant, with a net debt/EBITDA ratio of only 0.1, which is one of the lowest among its competitors.

Investment story

- The wave of AI infrastructure construction could also provide Micron with a favorable structural tailwind. The company is an indirect but increasingly important supplier to the AI ecosystem, providing high-bandwidth memory chips (HBM) for Nvidia and AMD's high-end server platforms, among others. These products are considered the company's primary growth catalysts, but price increases due to supply shortages of simpler memory chips for PCs and smartphones could also support growth through 2026.

- Beyond growth, it is strategically important that the weight of AI-related revenue is gradually increasing, which may mitigate the cyclicality typical of the memory chip industry in the company's fundamentals, such as revenue or gross margin. This improvement in the mix and the resulting potential reduction in volatility on the main lines of the income statements could justify a valuation premium for the stock in the longer term.

- In addition, Micron is also active in the field of data center and cloud infrastructure storage solutions, which means it has a further stake in the AI story. Furthermore, in the longer term, the company could benefit from the expansion of a number of segments with high computing capacity or significant data storage requirements. These include self-driving vehicles, 5G smartphones, robotics, and even quantum computing in the future—essentially any disruptive technology that relies heavily on memory-intensive infrastructure. The company already has a presence in some of these markets: it supplies memory solutions for automotive applications and 5G devices, and recently unveiled a new memory product that is considered groundbreaking in the industry and is also suitable for use in space technology.

- Micron Technology places great emphasis on continuous innovation, which enables it to maintain its technological leadership in the memory industry, giving it a competitive advantage. In the highly concentrated DRAM market, Micron is virtually the only major player in the United States, while its main competitors operate in South Korea (SK Hynix, Samsung). This geographical positioning may be an advantage for the company, as Korean manufacturers may be more sensitive to current tariff and trade uncertainties.

Risks

In Micron's case, the primary risk is volatile fundamentals. Both revenue and gross margin are highly cyclical, which is also reflected in pricing levels (significant discount compared to the broader market). If the increase in the share of AI-related sales within the revenue mix cannot reduce this volatility in the main income lines, the valuation may remain under pressure and reduce the growth potential of the stock.

Source: Bloomberg, OTP Multi-Asset Research

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more