Meta: more is needed if money is being spent at this rate

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

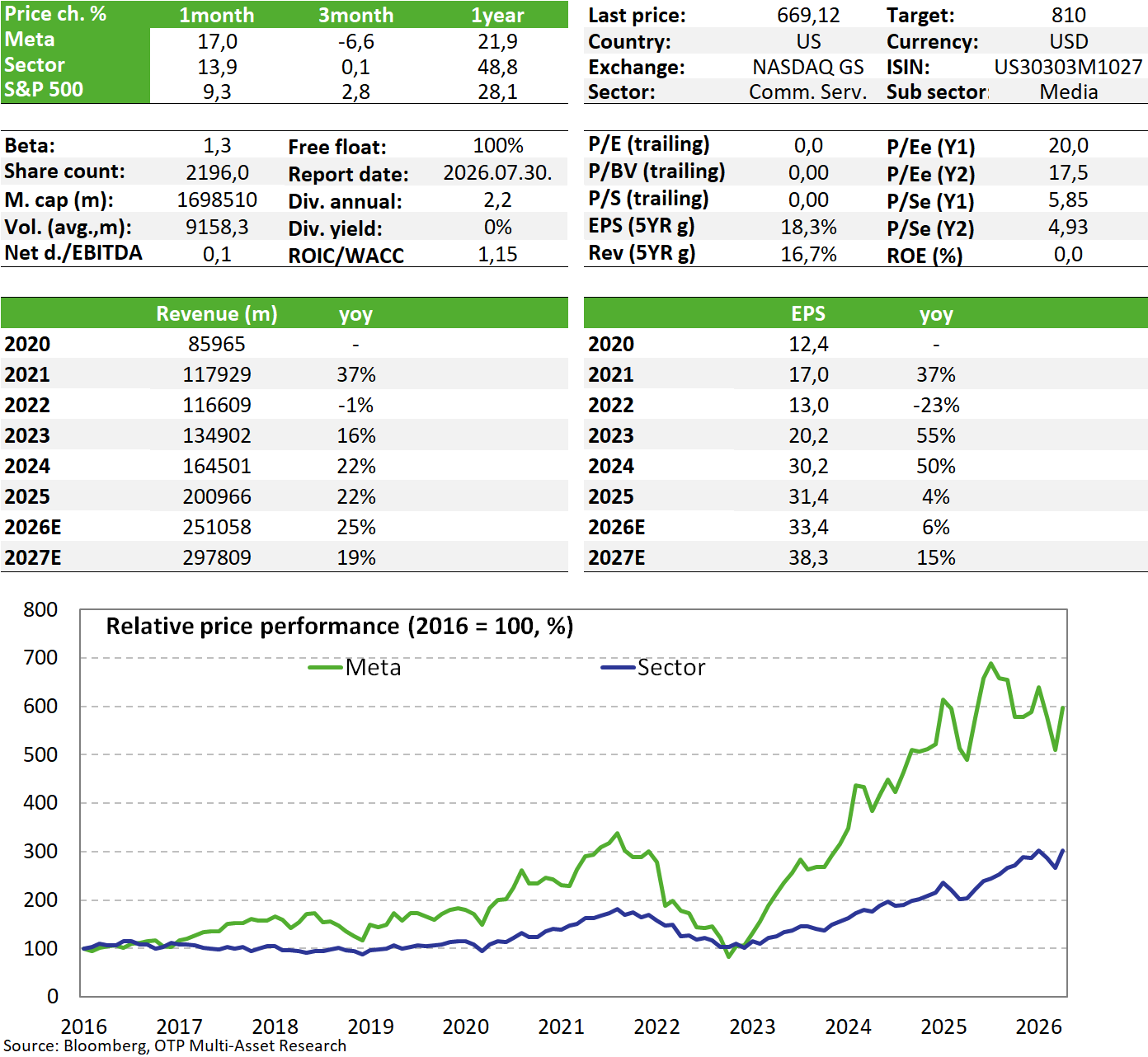

While the first-quarter figures “only” met market expectations overall, Meta raised its full-year capex plan due to rising AI spending. Since Mark Zuckerberg was unable to provide a reassuring answer during the earnings call regarding the product roadmap, timing, and expected returns of AI investments, this may have stirred up bad memories among Meta investors, who presumably do not want to run into a fiasco similar to the metaverse. In the short term, this kind of uncertainty could keep the stock under pressure; however, in our view, the company’s performance is strong enough (and may already reflect early returns from AI) to validate these investments over time.

Meta is included in our Equity Top Pick list.

Quarterly Report

In the first quarter, the company’s revenue grew by 33%, which represents very strong growth despite investment concerns; moreover, the $56.3 billion figure exceeds the expected $55.5 billion. The number of daily and monthly active users on Instagram and Facebook continues to grow, with videos driving all-time high user engagement on both platforms. The latter shows a 19% increase for the apps compared to the expected 16.2%, while the 12% increase in average ad prices was in line with expectations.

These figures already clearly reflect the impact of AI investments, which enable Meta to achieve greater personalization and better targeting in its ads—a strategy it can monetize even in the short term. In the first quarter, they also unveiled their Muse Spark model, which is capable of more advanced reasoning, solving more complex problems, and processing visual, audio, and text content—primarily in the fields of science, mathematics, and healthcare. It can do all this with lower computational requirements, meaning it’s more efficient; they’re implementing it in the Meta AI app and in smart glasses, and since it’s a closed system, they’ll be able to offer it as a premium service. It’s a competitive solution, though not a top-tier model on the market; in any case, it can help with personalized product recommendations based on user profiles, which could improve the conversion of posts into purchases.

There was some bad news this quarter, as the number of active users declined on a quarterly basis (to 3.56 billion, compared to the expected 3.61 billion)—a first since the data series began. Internet outages in Iran and the ban on WhatsApp in Russia played a major role in this; according to the CFO, the company would have recorded further growth had it not been for these factors. Revenue of $58–61 billion is projected for the second quarter, which is in line with expectations of $59.6 billion.

Operating profit came in better than expected, and Reality Labs’ cash burn was also lower than anticipated. The reported net profit figure appears to be significantly higher than expected, but this was also boosted by a one-time tax effect; excluding that, growth was more moderate at 13%, so the adjusted figure of 18.7 billion is not much higher than the expected 17.2. However, according to reports, the workforce reductions that began at the start of the year will continue; on the cost side, the company is increasing efficiency, which is partly attributed to the use of AI. They plan to cut 8,000 jobs (out of 72,000) and leave 6,000 open positions unfilled, which represents a significant step overall.

Since the overall figures are not particularly impressive, the market did not react favorably to the 7.4% increase in this year’s investment plan to $125–145 billion (compared to the expected $123 billion). This is because it brings back bad memories of the metaverse and other past investments that ultimately failed to deliver a meaningful return. At the analyst briefing, Zuckerberg’s remarks only added fuel to the fire, as he stated that the company has no exact plan for how it will scale and monetize AI-related products on a month-to-month basis.

Valuation

For now, these risks are somewhat offset by the fact that, thanks to the stock’s sideways movement over the past year, valuation metrics remain at comfortable levels; in fact, the company’s multiples are the lowest among the major tech giants (P/E: ~20, EV/EBITDA: ~14), while profit growth expectations do not justify this at all (~20% EPS and EBITDA CAGR 2025–27). Based on these metrics, we therefore maintain our previous fair value estimate of $810.

Investment thesis

- Meta’s social media platforms are used by 3.5 billion people every day. Its business can be divided into two segments: on the one hand, apps such as Facebook, Instagram, Messenger, and WhatsApp, which account for the majority of its revenue; and on the other hand, products and solutions related to virtual and augmented reality (Reality Labs).

- Among the major tech companies, Meta may be one of the biggest beneficiaries of the ongoing development of AI solutions, as it can leverage them against an existing, sufficiently large customer base: a solution called Meta AI is already in use, which acts as a conversation partner in chats, identifies and edits images, and can even serve as a live conversation partner in theory, with an active user base of over 1 billion. There are still some reliability issues, but these can be overcome as AI advances. The development of its own internal model (Muse Spark) also serves this purpose, as it is capable of solving complex tasks in a more cost-effective manner.

- The company spends most of its advertising revenue on developing AI capabilities; this year’s budget already exceeds $100 billion, but related personnel and other costs are also rising significantly. Cost pressures hang over the stock like a sword of Damocles, but for now, thanks to strong revenue growth, investors accept that the company will eventually be able to translate these expenses into profits.

- For one thing, AI solutions—by identifying behavioral habits and patterns—can greatly help make ads more targeted, and new products could emerge based on this, while there is also further potential for growth across the company’s various platforms (expansion of Threads, tapping into WhatsApp’s potential). What remains a hidden reserve for now—and it’s not yet clear whether the company will be able to capitalize on it—is the emergence and proliferation of AI agents, as well as the development of the “personal superintelligence” envisioned by Mark Zuckerberg. Since Meta possesses a significant amount of our personal data based on our social media consumption and activity, it is well-positioned to offer a truly personalized solution, which could even propel it to a leading role in the AI assistant market. However, this requires investment, and we will only see the return on that investment later.

- TikTok poses strong competition to the company’s platforms, but its large scale also carries the risk of antitrust and other legal concerns and penalties (ongoing discussions with the European Commission may compel the company to make changes that could have a significant negative impact on its European revenues).

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more