Hungary: Higher-than-expected inflation in December highlights that the MNB's caution is warranted

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

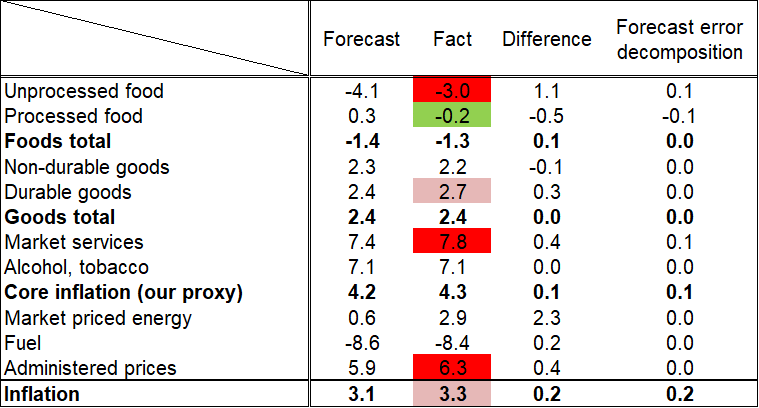

Hungary's headline inflation declined to 3.3% year-on-year in December, from 3.8% in November. In 2025, the annual average inflation was 4.4%. The December figure was slightly above the consensus (Bloomberg: 3.2%), and exceeded our forecast (3.0%), as well. Higher-than-expected inflation was caused by several items: higher-than-expected airfare prices, durable goods inflation, telecom and financial services fees. The impact of the margin cap for additional 14 food products, which came into effect on 1 December, did not reach -0.1%.

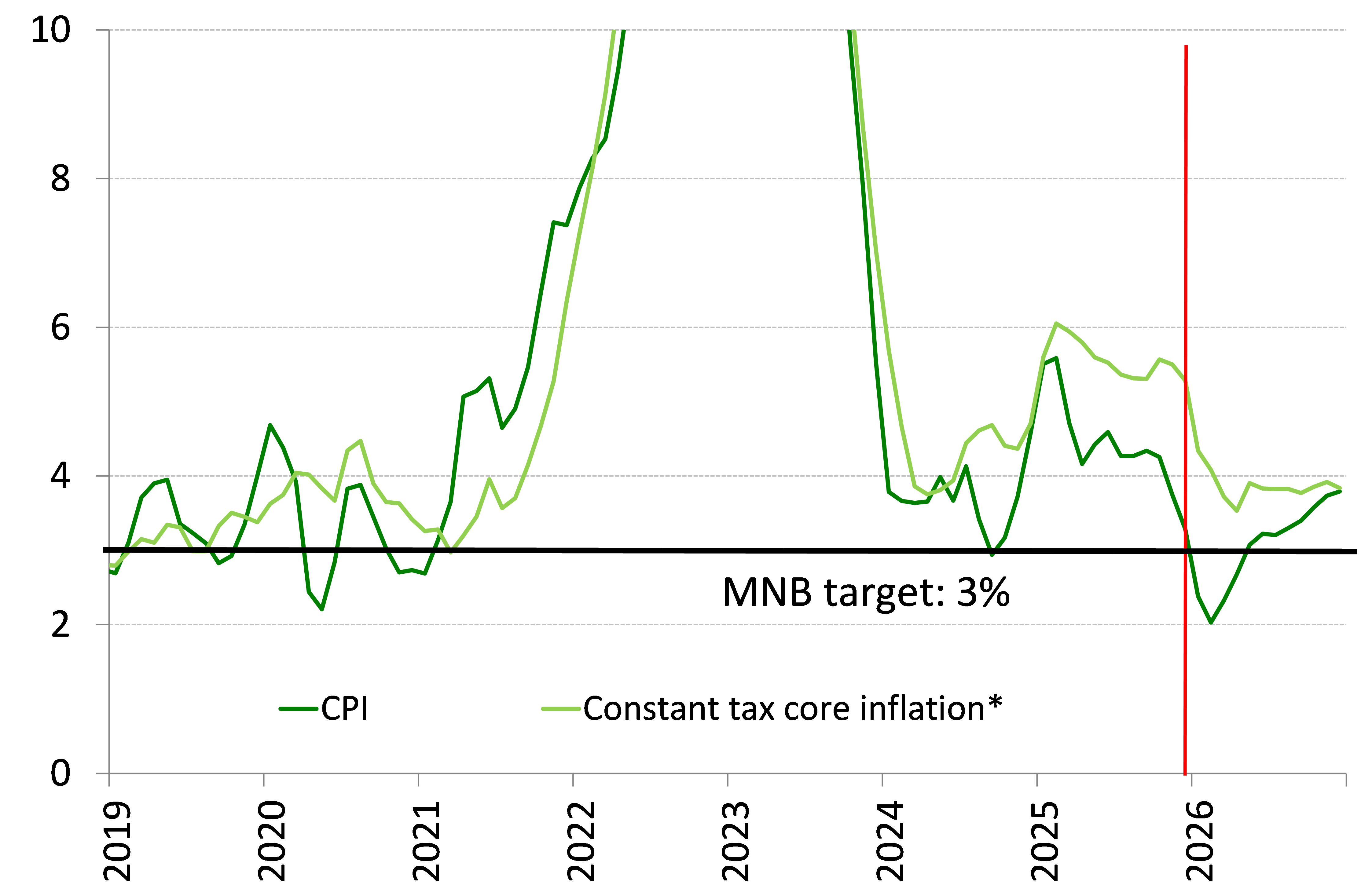

Underlying indicators moved in various directions in December. The MNB’s constant tax core inflation declined from 3.8% to 3.6% YoY, and the sticky price inflation decreased from 5.4% to 5.2% YoY. The MNB’s core inflation without processed food inflation and the profit margin cap’s effect measure has remained above 5% YoY. The latter underlying indicator of the MNB is very similar to our trend inflation indicator, but it still contains the mainly backward-looking pricing of telecom and financial services, which are also affected by the "voluntary" price freezes proposed by the government. Hence, we think our trend inflation (Chart 11) indicator is the better underlying gauge in the current environment as it does not contain telecommunication and financial services, therefore it is not affected by any administrative measures. The annualized MoM change of our trend inflation indicator accelerated from 5% to 6.7% (see Chart 11), while its annualized QoQ rate in Q4 was 5.6%, up from 4.6% in Q3 and 5.2% in Q2. This QoQ figure has almost reached its 2024 Q4 level (5.9%). In general, it can be said that the disinflation seen in the last quarter (inflation fell from 4.3% to 3.3%) occurred as a result of a deterioration in underlying trends, which was more than offset by favourable developments in food and fuel inflation (which are however, much more volatile than underlying trends).

One of the most important surprises is the higher-than-expected inflation in durable goods. This is particularly surprising because this is the most exchange rate-sensitive product group, and the forint’s exchange rate has been strengthening for some time. This development – especially before the main repricing period at the beginning of the year – may be cause for concern for the central bank’s policymakers, as it may indicate that economic actors do not have sufficient confidence in the sustained strength of the exchange rate. In addition, in the case of consumer electronics (part of the durable goods aggregate), the chip and graphics card shortage caused by the "AI frenzy" could bring further surprises.

Among the negative developments, it is also worth noting that intra-year price settings in the core service segment (Chart 6) was essentially the same as in 2024, meaning that there was no real progress in disinflation in this segment. In addition, the annualized QoQ change of the indicator accelerated to 8.3% in Q4, from 7.6% in Q3, and exceeded the 8.2% seen in Q2.

Food inflation continues to develop favourably. Our food inflation indicator (see Chart 10), which filters out the impact of profit margin caps and excludes volatile seasonal foods, has shown a clear improvement since early spring 2025. The favourable price trends for foodstuffs may strengthen even further, as China’s import restrictions on milk could lead to oversupply in the EU’s internal market. This could push down the prices of other dairy products, in addition to milk.

Currently, two opposing effects are influencing our forecast: persistently low energy prices and favourable food prices would pull down our inflation forecast, while the clear slowdown in the improvement of underlying processes would increase it. The net effect of these two factors is currently unclear, so we are keeping our inflation forecast for 2026 unchanged at 3.4%. We think inflation will probably sink well below the 3% target temporarily at the beginning of 2026 because of the delayed excise duty hikes, the expectedly very low re-pricing in administered prices, and a significant drop of the oil prices measured in HUF. But incoming data strengthen again our view that inflation persistence has still not been satisfactorily broken, so the central bank’s caution remains warranted. This is particularly true if we take into account the 11% minimum wage hike, effective from this January, and the consumption-stimulating government measures coming into effect these days.

We maintain our view that moderate price setting at the beginning of the year is necessary for looser monetary policy, therefore we expect two rate cuts in 2026, if the underlying inflation indicators are expected to decline to a level that is consistent with the MNB’s 3% target, thereby confirming that inflation expectations are sufficiently anchored.

Inflation forecast (annual changes, %)

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more