Hungary: Downside surprise in headline and services inflation paves the way for a February rate cut

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

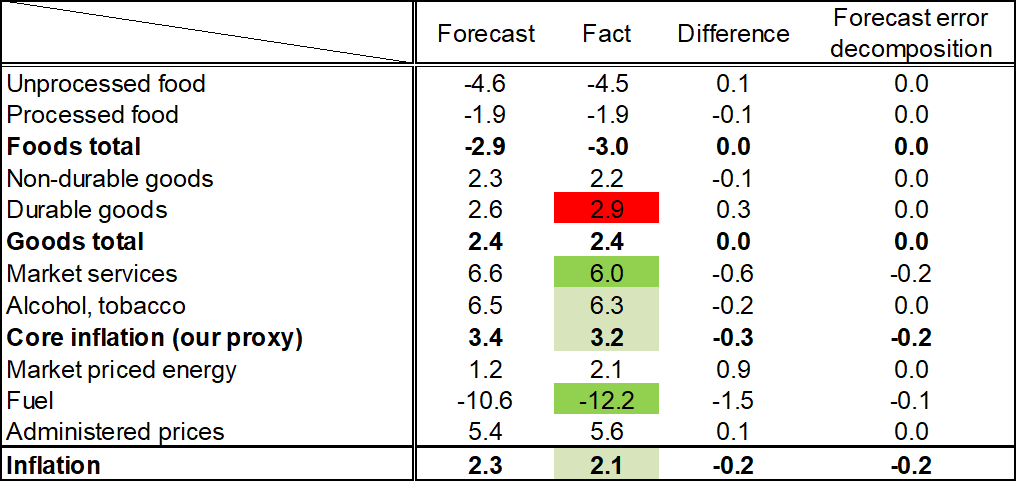

Hungary's headline inflation declined to 2.1% year-on-year in January, from 3.3% in December. A significant fall in the YoY index was anticipated, as the very strong repricing at the beginning of 2025 has dropped out of the base, fuel prices have been decreasing for months, and we expected very modest increases for regulated prices. However, even with this information in mind, the published data came as a surprise as it was lower than both the consensus (2.3%) and our forecast (2.3%). The main reason for the slower inflation was lower-than-expected services inflation. The MNB has been awaiting data with this structure for a long time, so the January inflation data pave the way for an interest rate cut.

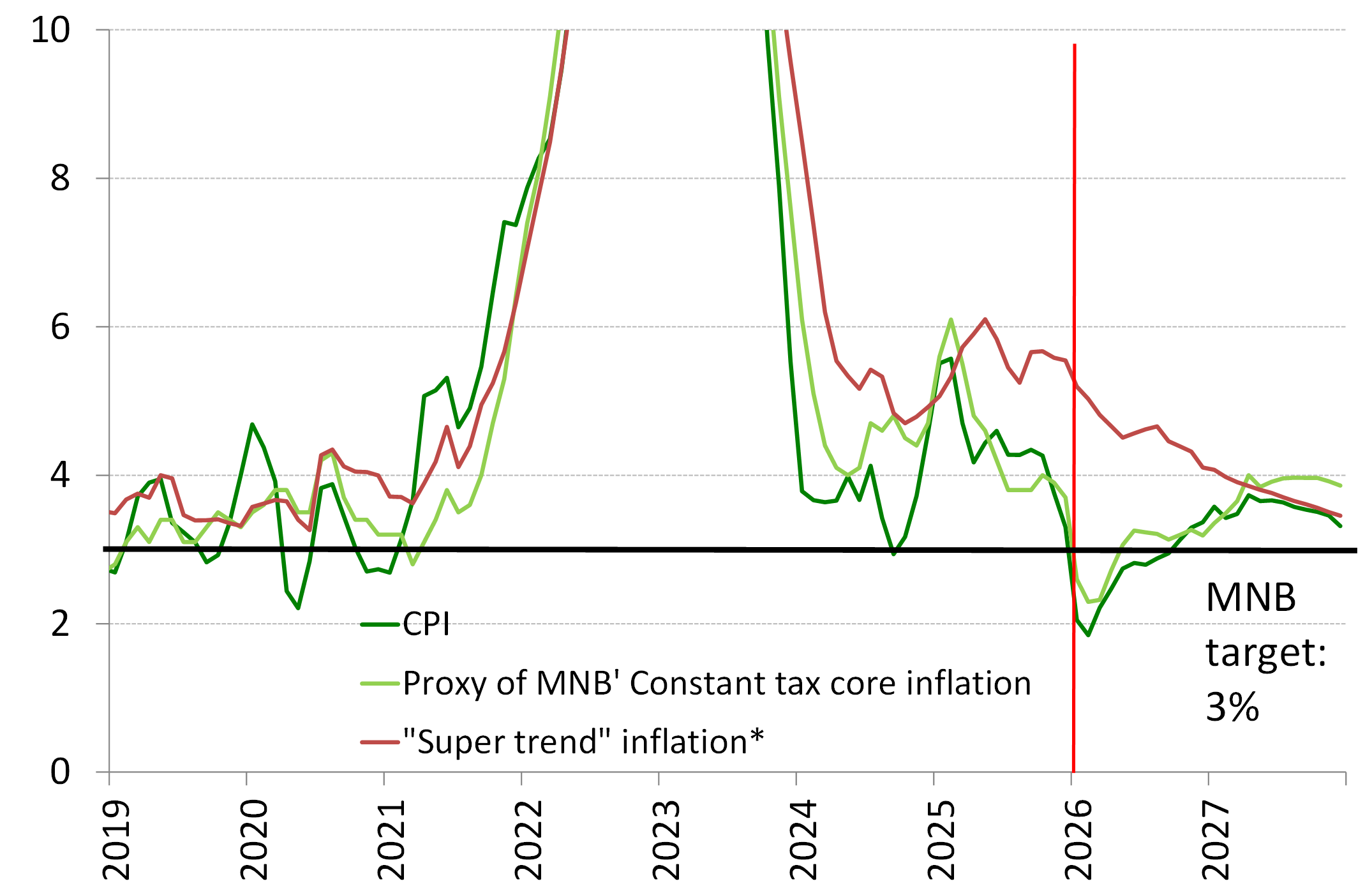

Underlying indicators improved in January. The MNB’s constant tax core inflation declined from 3.7% to 2.6% YoY, and the sticky price inflation decreased from 5.3% to 5.0% YoY. We should highlight that the MNB’s constant tax core inflation contains some items that were affected by the margin cap measures and it also contains the mainly backward-looking pricing of telecom and financial services, which are also affected by the "voluntary" price freezes proposed by the government. Hence, we think our “super trend” inflation (Chart 11) indicator is the better underlying gauge in the current environment as it does not contain telecommunication or financial services, and it is filtered from the margin cap’s effect, therefore it is not affected by any administrative measures. The annualized MoM change of our trend inflation indicator declined from 6.4% to 4% (see Chart 11). The slowdown in our"super trend" inflation indicator is, of course, a favourabledevelopment, especially since it is mainly due to the slowdown in servicesinflation. However, it is important to note that the indicator fell below 4%for several months last summer, then accelerated sharply again in the autumn(to an average of 5.5% in the last four months of 2025). For this reason, webelieve that caution is warranted, especially as the 11% minimum wage increase andthe government's consumption-targeting measures may bring negative surprises inthe coming months.

It is also worth noting that YoY goods inflation did not decrease compared to the previous month, but in general, despite the forint’s strength, there has been no clear decline in goods’ inflation for some time (in August last year, for example, industrial goods inflation was 2%, compared to 2.4% in January). In fact, the 0.3% month-on-month price increase in January is higher than the figures for 2024 and 2025, and is also the highest in a decade, excluding 2022/23. There are also specific stories behind the relatively high month-on-month goods inflation (such as computers/ consumer electronics, where the AI boom caused chip prices to rise, pushing up prices, or the explosion in gold prices, which increased the price of jewellery, or the rise in prices of home furnishings items due to the booming real estate market), however, even apart from these items, the strong forint’s price-reducing effect is not very noticeable. This may indicate that companies still do not believe that the EUR/HUF can remain at its current level in the long term, so they are still adjusting their prices to a weaker forint.

Food and fuel inflation continue to contribute significantly to disinflation, as only these two product groups show YoY deflation. The contribution of food and fuel inflation is -1.2 percentage points, which is 0.3 percentage points higher than in December. The favourable price trends for foodstuffs may continue throughout the rest of the year, as China’s import restrictions on milk could lead to oversupply in the EU’s internal market (this could push down the prices of other dairy products, not just a milk) and the trade agreement between the EU and the Mercosur states may also help to reduce food inflation.

Considering that currently the forint is stronger (EUR/HUF: ~380) than we had previously anticipated, price adjustments at the beginning of the year were smaller than anticipated, and food prices may develop even more favourably than we had previously thought, we are lowering our 3.4% forecast for this year (see the chart below). It currently seems likely that inflation will fall below 3% for the year as a whole. However, we expect a renewed increase to 3.5% in 2027. That increase will be the result of expected rises in fuel and food inflation and declining trend inflation. For this reason, we believe that rising inflation in 2027 will not prevent the central bank from cutting interest rates

We think that January will provide the central bank with sufficient ammunition to start cutting interest rates at its next meeting in February. Previously, we expected two interest rate cuts this year, one in Q1 and one in Q3. If there are no major negative surprises in services inflation in February, the two interest rate cuts could happen in February and March. Further interest rate cuts will depend on the economic policy after the parliamentary elections.

Inflation forecast (annual changes, %)

Among the forecasts shown, we previously presented the constant tax core inflation calculated by OTP Research, which filtered out the effect of margin caps, as opposed to the indicator published by the central bank. Since it is likely that the central bank's own indicator will be the guiding factor in its decisions, we will now include the indicator calculated according to the central bank's methodology. In addition to the previous indicators, we also present our "super trend" indicator, which we believe is the best indicator of the long-term inflationary processes.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more