Hungary: The energy price shock casts shadow over the significantly- lower-than-expected February inflation data

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

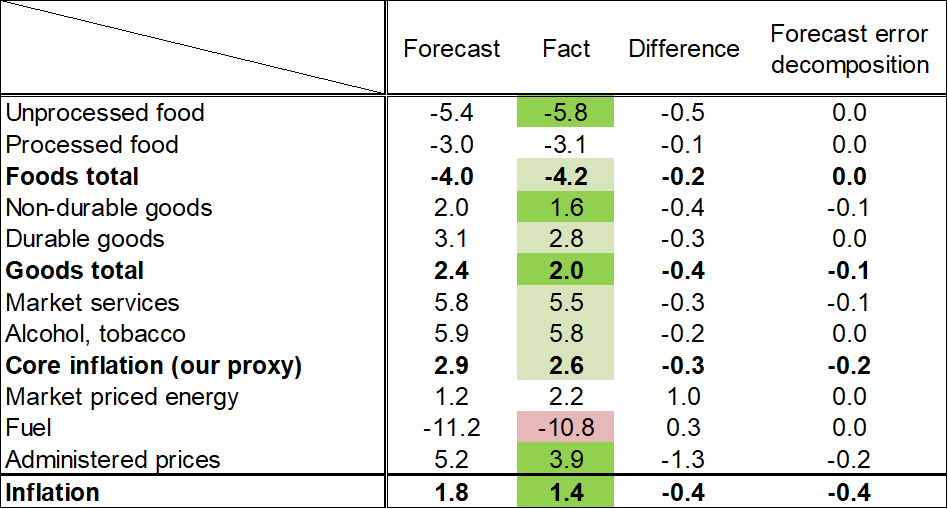

Hungary's headline inflation declined from 2.1% year-on-year in January, to 1.4% in February. The published data came as a surprise as it was lower than both the consensus (1.7%) and our forecast (1.8%). Half of the surprise was caused by lower-than-expected inflation across a wide range of products and services. Another 0.2-percentage-point surprise was due to the accounting of "utility fee refunds" introduced by the government. In January, the weather was unusually cold, and energy consumption significantly increased, therefore the government decided that public utility providers should offer a 30% refund on the energy used for heating (district heating, gas, electricity) in January. It was far from evident that this measure would be accounted in inflation, and the statistical office did not provide any further information on this topic even after the data was released.

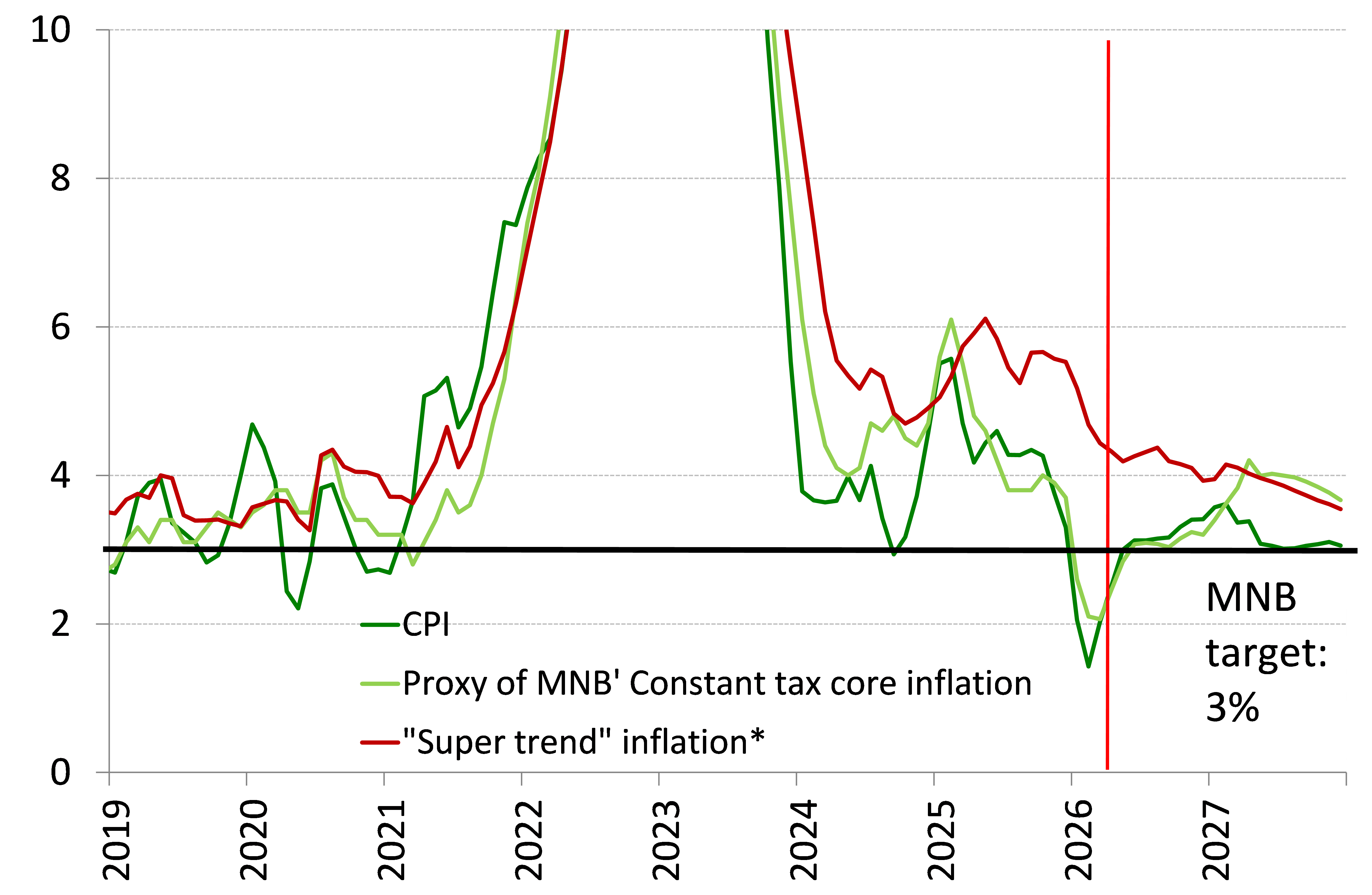

Underlying indicators improved in February. The MNB’s constant tax core inflation declined from 2.6% to 2.1% YoY, and the sticky price inflation decreased from 5.0% to 4.6% YoY. We should highlight that the MNB’s constant tax core inflation contains some items that were affected by the margin cap measures and it also contains the mainly backward-looking pricing of telecom and financial services, which are also affected by the "voluntary" price freezes proposed by the government. Hence, we think our “super trend” inflation (Chart 9) indicator is the better underlying gauge in the current environment as it does not contain telecommunication or financial services, and it is filtered from the margin cap’s effect, therefore it is not affected by any administrative measures. The annualized MoM change of our trend inflation indicator declined from 4.0% to 1.8%, and the repricing of market services, which is closely watched by the central bank, remained subdued in February. As our "super trend" indicator remained favourable in February after January, we can now say with increasing certainty that the inflation risks linked to the 11% minimum wage hike and to the government's consumption-stimulating measures did not materialize, and the strong exchange rate and weak economic growth appear to have brought lower re-pricing at the beginning of the year.

Based on the incoming data alone, we would have lowered our 2026 inflation forecast of 2.9% by 0.3 percentage points. However, taking into account the current energy price developments (see our assumptions in Chart 11), our forecast has risen back to 2.9%. It is important to emphasize that energy prices have the strongest and fastest impact on inflation through fuel and energy prices. In Hungary, household energy prices are regulated, and we assumed that the government would not raise them. Furthermore, the Hungarian government has also capped fuel prices (at around 7% higher than last week's price), so rising oil prices will have only a limited impact on this product group as well. As a result, the effects of rising energy prices are reflected in inflation in a much less direct and slower manner (rising transport costs, corporate energy prices, etc.).

The aforementioned additional inflationary effect may seem low at first glance, especially in light of the fact that Hungarian inflation peaked at 10 percentage points above the regional average during the 2022 energy crisis. However, the current situation differs from that of 2022 in several respects: (1) the expected energy price shock is much smaller, and in our opinion, it does not reach the level at which the effects become non-linear, (2) in 2022, energy prices rose to such an extent that the government was forced to abandon the very low fixed energy prices for households that were in effect at the time. We do not expect this to happen now due to the currently higher regulated prices and a smaller energy price shock, (3) in 2022, the forint weakened significantly (the lasting depreciation exceeded 10% compared to the situation before the energy price increase). Currently, the forint is at its end-of-2025 level, and even in the big sell-off on 9 March, it was only about 3-4% weaker than that. (4) In 2022, food and energy price shocks hit at the same time, and (5) due to the significant amount of economic stimulus during/after Covid, the energy price shock hit an already overheated economy that was already on an upward inflationary path. Currently, however, the Hungarian economy is emerging from a period of weak growth that has lasted for several years, with inflation expectations slowly declining.

Although February's inflation data was favourable, the central bank is likely to wait with the next interest rate cut until the extent and duration of the energy price shock become clearer. If energy prices develop in line with our assumptions, we believe that an interest rate cut will be possible at the end of Q3 or in Q4, as we believe that the assumed energy price developments will not have a second-round effect (raising inflation expectations), which was the main reason for the very slow disinflation in Hungary. We expect an earlier interest rate cut only if energy prices return very quickly to their pre-Iran war levels, but this is currently unlikely.

Inflation forecast (annual changes, %)

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more