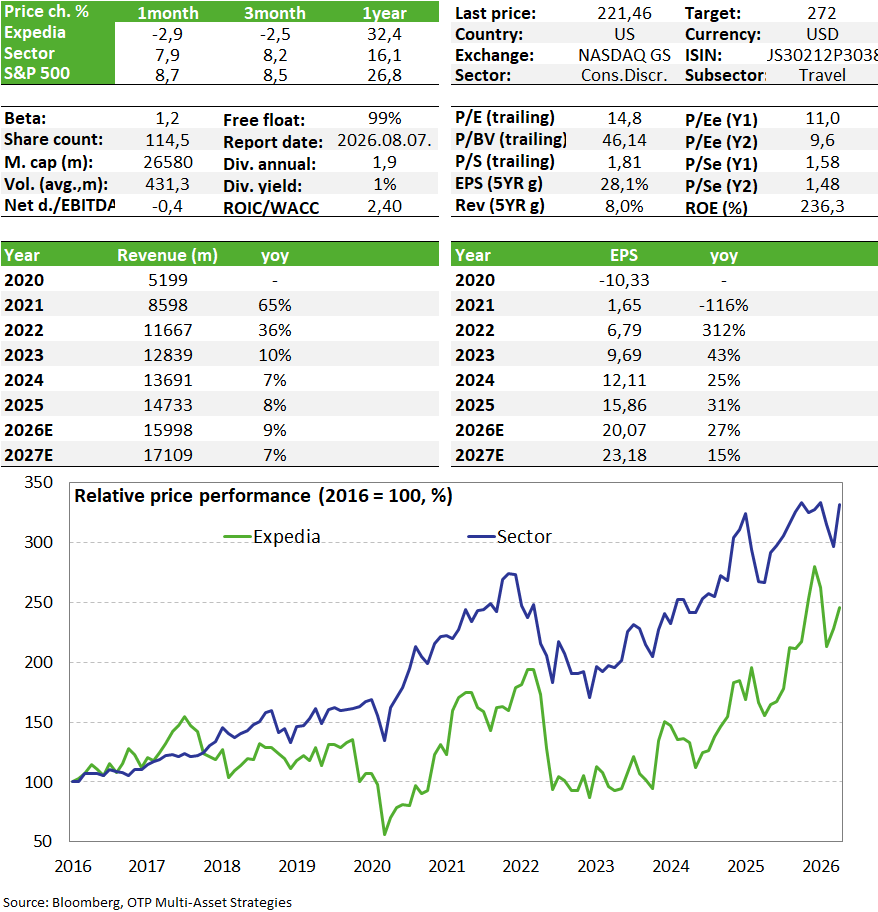

Significant growth at Expedia

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

We really can’t complain about Expedia’s first-quarter results; the company beat consensus estimates by a wide margin and delivered strong growth year-over-year across all key metrics. However, due to the war in Iran, travel sentiment appears to be deteriorating, which could already be reflected in second-quarter booking data, and as a result, the company has forecast more modest growth, which has given investors a bit of a scare (hence the drop in the stock price following the report). In the short term, this headwind may persist, but due to strong performance, a significant share buyback program, and the stock’s low valuation, we are maintaining it on our Equity Top Pick List.

Expedia remains on our Equity Top Pick List.

Quarterly Report

Vrbo recorded its highest number of guest nights in four years during the first quarter, and overall guest nights increased by 6%, while average booking prices also rose. The first quarter delivered truly strong booking figures, reaching $35.5 billion compared to the expected $35.1 billion. Annual growth stands at 13%, with the B2B segment once again driving the outstanding 22% growth; however, the 10% growth seen in B2C cannot be called weak either (in fact, this is the highest rate in years).

Direct exposure to the Middle East is low, accounting for less than 2% of bookings; nevertheless, booking cancellations picked up in March, primarily for trips to Europe or Asia, and the escalation of violent incidents in Mexico also weighed on bookings. According to management, this did not affect the appetite for domestic travel in the U.S. The company’s second-quarter booking forecast of $32.58–33.1 billion—which fell short of the $33 billion consensus—may be linked to rising geopolitical risks and the expected negative impact of rising fuel costs. A slightly positive sign for the future is that management did not revise its full-year forecast, which remains at $127–129 billion, and that booking activity stabilized in April and has since begun to pick up again.

Revenues performed well in the first quarter, growing by 15%—exceeding expectations. The B2C segment contributed 8% to this growth, while the B2B segment contributed 25%. What painted a particularly strong picture was the EBITDA margin, as the company achieved its highest first-quarter figure in 15 years, at nearly 16%, thanks to which the $542 million in EBITDA was significantly higher than the expected $452 million.

Over the past 12 months, free cash flow has thus reached $4.1 billion, which amounts to 15% of the company’s market capitalization. Of this, a quarterly dividend of $0.48 will be paid, and in the first quarter, the company also spent $700 million on share buybacks, bringing the total for the past year to $2 billion, or 7.5% of market capitalization. This continues to represent a very strong shareholder return, which remains a strong argument in favor of the stock despite the fact that geopolitical uncertainties and rising energy prices may temporarily dampen the desire to travel and thus the company’s numbers, while AI innovations loom over the company like a constant invisible sword. In addition to strong cash generation, the nearly $6 billion in cash on hand allows the company to continue buying back its own shares; it has already announced a $5 billion buyback program.

Valuation

In recent weeks, the stock has corrected lower, in line with its sector peers, due to heightened geopolitical risks, rising fuel prices, and a slight decline in travel demand. However, since the company’s performance continues to exceed expectations and its earnings growth remains exceptionally strong, the stock’s valuation metrics remain at attractive levels. The P/E ratio of 11 and the EV/EBITDA ratio of around 7 are also attractive multiples compared to sector peers, especially considering that EPS is expected to continue growing by around 17%, while EBITDA is projected to increase by approximately 10%. As the company’s fundamental performance improves but external macro risks are also intensifying, we maintain our previous fair value estimate of $272, determined using the ratio-based method.

Investment thesis

- Expedia is one of the world’s leading online travel marketplaces (most comparable to Booking). Three-quarters of its revenue comes from accommodation booking fees earned for acting as an intermediary, with the remainder coming from airline ticket sales, advertising, and other services.

- Expedia’s commission revenue is largely influenced by trends in tourism spending. Rising real wages driven by falling inflation also have a positive impact, while geopolitical tensions pose a risk.

- The company recently launched a single global loyalty program (One Key) to tap into the potential for cross-selling across its platforms. This cross-brand loyalty program is unique compared to competitors, which partly explains the recent growth in revenue and margin expansion—a trend that is expected to continue having positive effects in the future. Ariane Gorin, the former head of the B2B segment, took over as CEO in May 2024. Since then, the transformation has proven successful; the company has achieved solid growth, and with the AI-based solutions introduced, it has managed to keep pace with the market, with the first signs of this already visible in terms of efficiency.

- Earnings and cash generation are strong, and the company recently resumed dividend payments that had been suspended due to COVID-19, although this represents an annualized yield of less than 1%. The most significant item remains the share buyback program: over the past year, the company spent $2 billion of its $4.1 billion in free cash flow, which represents ~7.5% of its market capitalization. Given the strong performance, this trend is likely to continue; moreover, a new $5 billion share buyback program has been approved, providing strong support for the stock price.

- The activist hedge fund Starboard Value acquired a 9% stake in Tripadvisor, a close industry peer of Expedia, during the summer of 2025. The investor’s move may have been influenced by the relatively low valuation of TripAdvisor shares, which could indirectly draw attention to Expedia, which is trading at similarly depressed valuation metrics.

- However, the concerns among software service providers regarding AI developments may also raise questions about Expedia’s business model. If the role of AI agents in travel planning and booking begins to grow, it could significantly undermine the growth prospects of intermediary companies. This is a serious risk that could negatively impact investor sentiment toward the stock and the sector even within the next year or two.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more