Broadcom: Could Benefit from Further Advances in AI

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

Within the AI megatrend, the focus is increasingly shifting from training to usage and inference, which could bring new winners to the forefront in the semiconductor industry. In this phase, the role of custom-designed, task-specific, and energy-efficient AI chips is becoming more important, an area where Broadcom holds a market-leading position. The company’s strong relationships with hyperscale customers, long-term custom AI chip agreements, and secured manufacturing capacity create excellent growth visibility. At the same time, the stable, high-margin IT infrastructure business mitigates risks stemming from cyclicality. Together, these factors result in an attractive risk-return profile. Taking all this into account, we are adding Broadcom shares to our Equity Top Pick list.

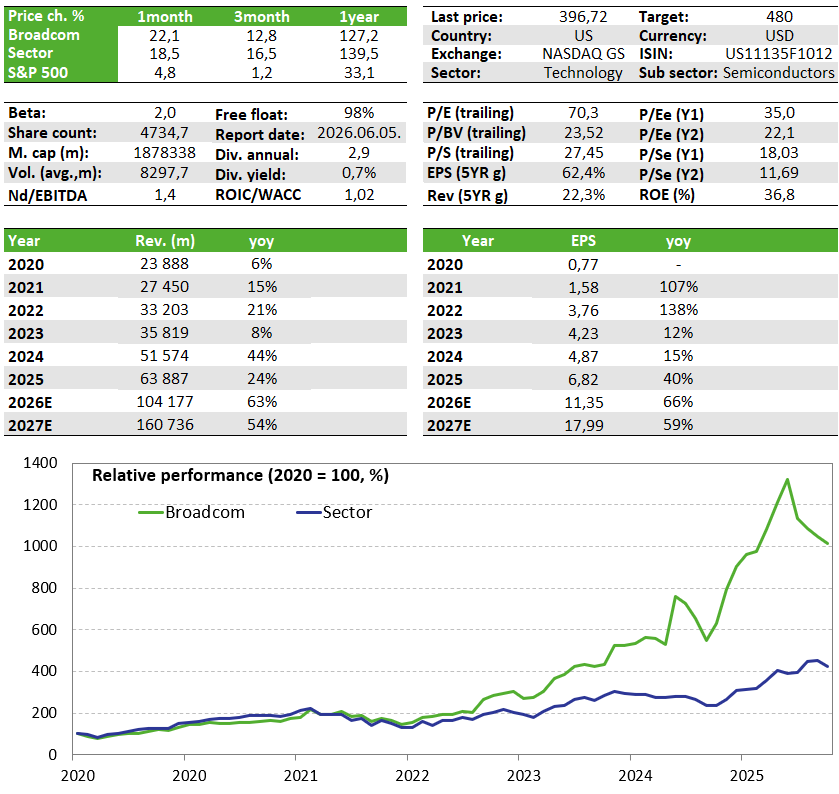

Company Overview

Broadcom is a market leader in custom-designed AI chips (ASICs). The company focuses exclusively on chip design and outsources manufacturing to TSMC. In addition, the company has an IT infrastructure services segment that provides virtualization, cloud-based, and cybersecurity solutions to enterprise customers. The semiconductor segment currently accounts for about two-thirds of revenue and serves as the primary growth driver. In contrast, the IT infrastructure business generates approximately one-third of revenue, supporting the company’s operations with stable and predictable cash flow.

Revenue in the semiconductor segment is highly concentrated, coming primarily from six major hyperscale customers, including Meta, OpenAI, Anthropic, and Google. Among these, Google plays a key role, as the TPUs (Tensor Processing Units) developed jointly with Broadcom represent the company’s most important source of revenue. TPUs have played a key role in the growth of Google’s AI ecosystem, contributing to the Gemini model’s market-leading position (in terms of performance) and strengthening the competitiveness of Google Cloud services. The company also offers AI-focused networking solutions, which also hold significant growth potential in the coming years.

Sales in the IT infrastructure business operate on a subscription-based model, providing bundled offerings to large enterprise customers. The segment generates stable, highly predictable revenue, which mitigates the risks associated with the cyclical nature of semiconductor revenue. The company focuses on a premium customer base in this area, which, combined with cost efficiency, enables outstanding margins (gross margin of 93%), though growth remains in the low single digits.

Investment case

The wave of AI infrastructure development could provide Broadcom with a favorable structural tailwind. Within the AI megatrend, as the focus gradually shifts from training to inference phase in the coming years, it will gain importance, and the winners could be custom-designed AI chips (ASICs), as they can be optimized for specific tasks and are energy-efficient. Broadcom is the market leader in this segment.

The TPUs co-designed with Google are competitive with Nvidia GPUs during the inference phase, while they currently outperform GPUs in terms of energy efficiency; thus, in a scenario where energy becomes the bottleneck in AI, the company’s solution could gain greater value. Furthermore, an Nvidia GPU costs nearly ~3x as much as a TPU, so if hyperscalers find themselves in a tight cash flow situation, the TPU could be a favorable alternative, as it is not only cheaper to purchase but also to operate, given that it offers ~2x the performance-per-watt ratio of Nvidia’s previous-generation product.

In the short term, another catalyst could be the 2026 capital expenditure plans announced by hyperscalers during Q1—particularly in the case of Google (+50% vs expectations) and Meta (+15% vs expectations), which are among the six major customers to whom Broadcom supplies custom-designed AI chips. In the past six months, semiconductor companies without their own production lines have massively underperformed their competitors with manufacturing capacity; however, Broadcom announced in early March that it had secured its supply chain for the 2026–2028 period regarding both memory and TSMC’s high-end manufacturing capacity. Furthermore, in recent weeks, it has signed long-term agreements with Anthropic, Meta, and Google for ASIC deliveries, reporting an agreement with the latter extending through 2031, which could help provide longer-term revenue visibility for the company and mitigate risks related to the sustainability of its growth rate.

Taking all of this into account, we are adding Broadcom shares to our Equity Top Pick list.

Valuation and Debt Level

The company’s profit margin exceeds 50%, while its EBITDA margin approaches 70%; only Nvidia in the industry boasts comparable figures. Furthermore, it is one of the top semiconductor companies in terms of growth; analysts expect annual average revenue growth of around 45% and EPS growth of over 60% for the 2026–2028 period. Despite this, the stock is not trading at a premium compared to either its competitors or its own valuation multiples seen over the past 2–3 years. Based on key metrics, even a price level of $480 appears fair. The company’s debt position is not significant, with a net debt/EBITDA ratio of just 1.1, which, combined with strong cash flow generation, can be considered a healthy level.

Key risks

One key risk associated with Broadcom is potential margin compression resulting from the increasing proportion of AI-related semiconductor product sales in the revenue mix. This has a downward effect on the company’s overall gross margin, given that the IT infrastructure business operates with an exceptionally high gross margin of approximately 93%, compared to the roughly 60% level of AI-focused semiconductor products. Although the market has already priced this in, there may be more positive surprises here than in the early March flash report, which suggests no short-term pressure on margins.

In addition, the proportion of sales in China is relatively high (though declining year over year) at ~17%, which could pose a geopolitical risk. Furthermore, there is a high concentration of customers in the semiconductor business: nearly all revenue comes from six major players, with Google standing out among them (TPU shipments). In addition, any potential increase in risks surrounding the financing of AI infrastructure investments could naturally have a negative impact on the company, as well as on the entire industry.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more