Amazon Hits New Highs After Strong Earnings Beat

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

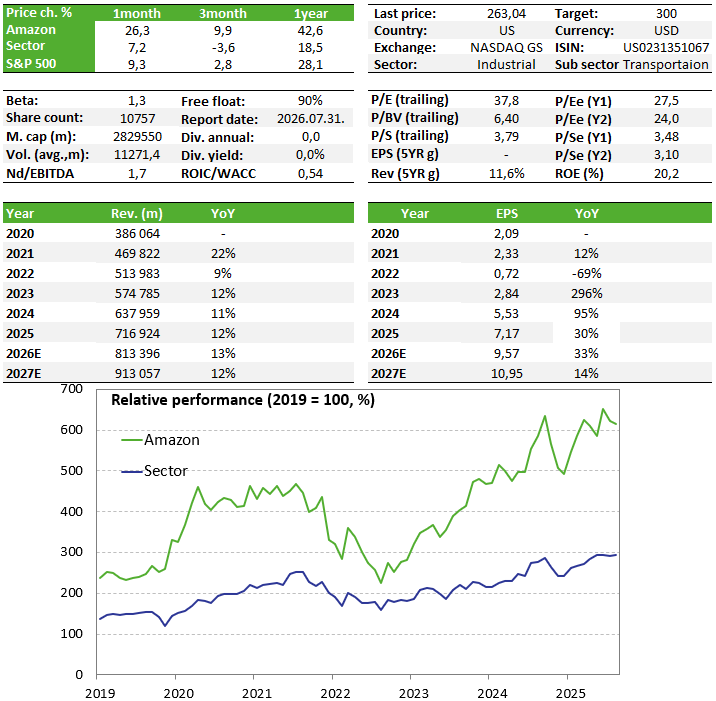

Amazon’s earnings report sent a strong message to the market: the company is capable of reaccelerating growth in its cloud business, maintaining exceptional momentum in advertising, and improving the efficiency of its retail operations at the same time. The share price reached a new high in April, although some risks remain. Investments related to AI infrastructure are putting significant pressure on free cash flow, meaning that the investment case depends on how quickly the company can turn this massive capex cycle into profitable growth. For now, the outlook remains favourable.

Amazon shares remain on our Equity Top pick List.

Quarterly Report

April was an exceptionally strong month for Amazon, with the share price set to finish the month up by 30%, while the stock may open at a new high following the latest earnings release. This comes after a prolonged period during which the share price had mostly moved sideways. First-quarter revenue came in at USD 181.5 billion, up 17% year-on-year, ahead of expectations, while operating income rose to USD 23.9 billion, implying a record operating margin of 13.1%. EPS also came in significantly above analyst forecasts, at USD 2.78 versus USD 1.64 expected.

That said, there were some critical points within the results. Net income was boosted by a USD 16.8 billion pre-tax gain related to the company’s investment in Anthropic, while free cash flow over the past twelve months declined to USD 1.2 billion from USD 25.9 billion, mainly due to investments in artificial intelligence infrastructure.

The company’s emerging satellite internet service is also requiring an increasing level of investment, as Amazon will need to place a large number of satellites into orbit in the near future. In April, Amazon announced that it would acquire satellite communications company Globalstar for USD 11.5 billion. As a result, Amazon could become a major competitor to SpaceX’s Starlink as well.

At the same time, AWS revenue increased by 28% to USD 37.6 billion, also ahead of expectations, implying an annual run-rate of around USD 150 billion. According to management, growth was supported by strong demand for both core cloud services and AI-related services. Demand for Amazon’s internally developed chips, such as Trainium, is also exceptionally strong.

Advertising revenue jumped by 24% to USD 17.2 billion, lifting the trailing twelve-month revenue figure above USD 70 billion. Management highlighted full-funnel advertising, Prime Video, the partnership with Netflix, and AI-powered creative tools as key growth drivers. This business line is also particularly important because it operates with very high margins.

The 15% growth seen in retail was the strongest figure since the end of Covid-related restrictions. Amazon also pointed to rising demand for same-day and next-day delivery as a factor supporting demand. The margin story in retail is no longer merely about cost-cutting. Increasingly, it reflects a combination of regionalisation, automation, robotics, Prime user engagement, and advertising revenue, all built around faster delivery.

For Q2 2026, Amazon expects revenue of USD 194–199 billion, implying year-on-year growth of 16–19% and exceeding the analyst consensus estimate. However, operating income guidance was set at USD 20–24 billion, compared with the consensus average of USD 22.65 billion.

Investment thesis

- AWS is a leader among major cloud service providers, and this quarter has once again demonstrated that it still has room to grow. The advertising segment also has significant potential for growth, and this business line could become a major profit driver thanks to its high margins.

- The rise of AI is still in its early stages, and we can expect even greater growth in this area in the coming years; Amazon is in one of the best positions to capitalize on this expansion. AWS already offers a platform that its customers can use to support their generative AI development efforts, for example.

- The retail sector is constantly seeking ways to improve efficiency, which could continue to have a positive impact on margins in the future. It may also benefit early on from the spread of automation through increased efficiency.

- Risks: Competition is extremely intense in the cloud computing sector and the field of artificial intelligence. It is not certain that Amazon will come out on top. It is unclear over what timeframe and with what returns the tens of billions of dollars the company is spending on AI investments will pay off. This is one reason why sentiment in the stock market was currently negative.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more