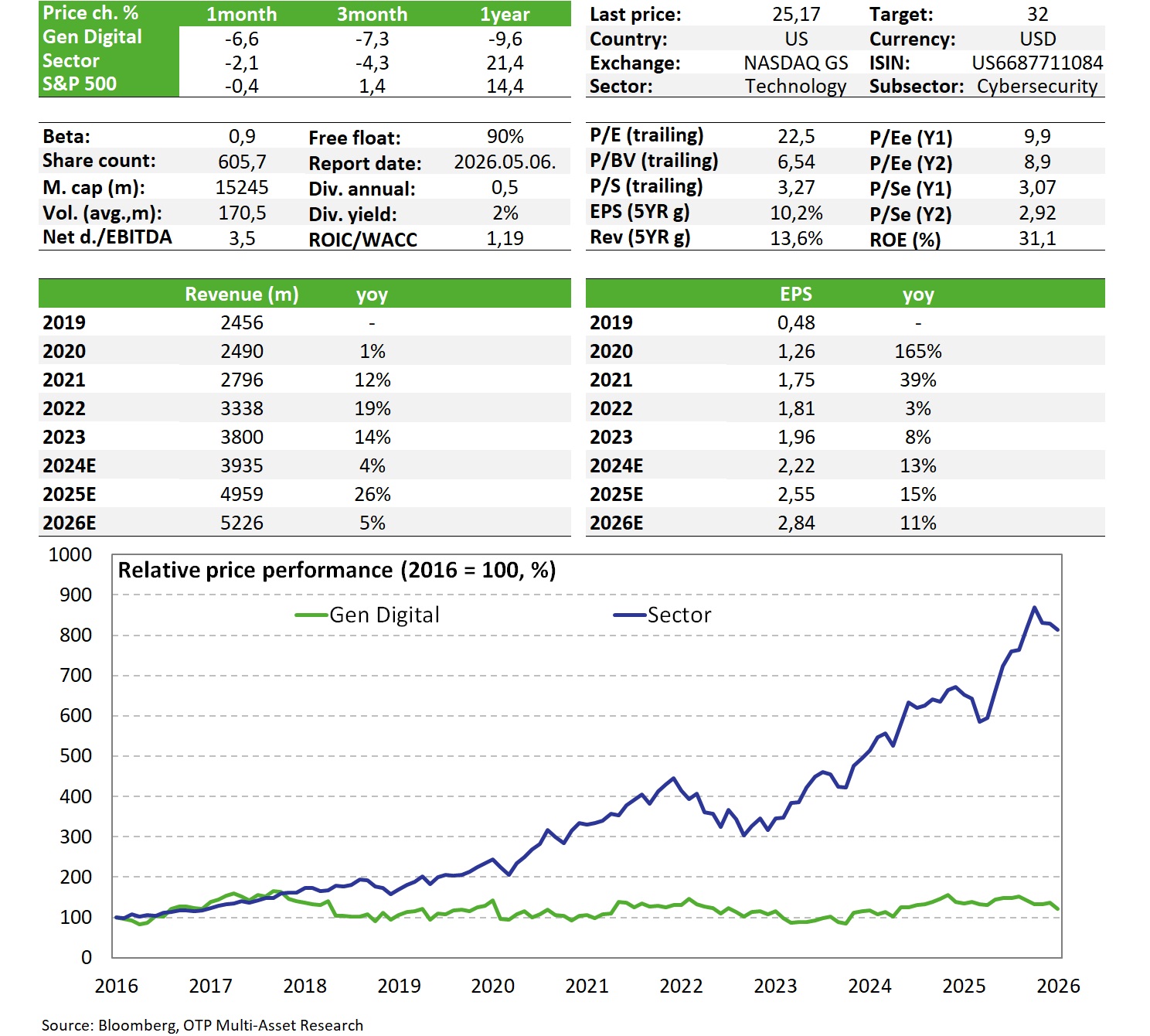

Gen Digital: still going strong

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

After the company delivered positive surprises in its main lines and annual forecasts, in addition to the return of share buybacks, the stock's performance could temporarily diverge (outperform) from the negative trends seen across the software sector as a whole. For this reason, and due to the continued attractiveness of the stock, we are maintaining it on our Equity top Pick List for the time being, but we would like to point out that we may make changes to this in the future depending on price movements. Primarily for the reason that, although the company's cyber security activities appear to be less threatened by AI solutions, the business model of MoneyLion, a financial advisory service acquired last year, could be particularly vulnerable, which could cast a shadow over the company's longer-term growth prospects.

Quarterly report

The subscriber base grew by 11% in the fourth calendar quarter (year-on-year), from 67 million to 78 million, which represents a slight increase compared to the previous quarter, with half a million new customers acquired in the cyber security segment. Revenue growth in the partner-mediated segment (which accounts for one-fifth of total revenue) remained stronger at 87%, while direct sales, which carry greater weight, grew by 18%, also representing a slight acceleration compared to the previous quarter.

Revenue grew 26% year-on-year, but this growth was largely due to the fact that, following the acquisition of MoneyLion in mid-April, this was the second full quarter in which it appeared in the books, meaning that this revenue generation was missing from the base period. If it had been included, the so-called pro forma growth would have been more modest, at 8%. Excluding MoneyLion entirely, Gen Digital's core business performance, or so-called organic growth, is even weaker, at just 4%. It should be added, however, that the market is aware of this, and compared to what analysts expected (USD 1.22 billion), the actual figure of USD 1.24 billion came as a positive surprise. In addition, management expects the favorable trends to continue, raising its revenue forecast for the full year (which ends at the end of March ), from the previous USD 4.92-4.97 billion to USD 4.955-4.97 billion, which was also a pleasant surprise, as analysts had previously expected the lower end of the revenue range indicated for the last financial quarter of the year.

The operating profit margin decreased from 59% to 51%, also as a result of the transaction, while the cyber security platform segment, which was unaffected by the transaction, showed an improvement from 60% to 61% (AI-based cross-selling recommendations played a role in this). In the segment supplemented by personal financial services, although revenue growth was more dynamic (+22% pro forma), margins were lower at 30%, but this was entirely expected.

EPS grew by 14% on an annual basis, marking the ninth consecutive quarter of double-digit percentage growth. The adjusted EPS of 64 cents exceeded the consensus estimate (63 cents), and management raised its annual forecast from $2.51-$2.56 to $2.54-$2.56, with the analyst consensus currently still at the lower end of the range.

Another positive message for shareholders is that the company's free cash flow reached $535 million (compared to $318 million in the base period), bringing the total for the year to date to $1.2 billion, which is 8% of market capitalization. Shareholders have also benefited from this, as strong cash generation has brought the debt ratio (which rose again after the transaction) closer to the target (the target is for net debt/EBITDA to be below 3, currently 3.1). As a result, the company repurchased $300 million worth of its own shares during the quarter, which is a significant 2% of the total, and also paid out $77 million in dividends.

After the company delivered positive surprises in its main lines and annual forecasts, and with the return of share buybacks, this could fundamentally help the share price to temporarily diverge (outperform) from the negative trends seen across the software sector as a whole. For this reason, and due to the continued attractiveness of the stock, we are maintaining it on our Equity Top Pick List for the time being, but we would like to point out that we may make changes in the future depending on price movements. This is primarily because, although the company's cybersecurity activities appear to be less threatened by AI solutions, the business model of MoneyLion, a financial advisory service acquired last year, may be particularly vulnerable, which could cast a shadow over the company's longer-term growth prospects.

Valuation

In the technology sector, and within that among software companies, Gen's valuation metrics remain fairly depressed (PE: around 9 vs. sector: 20, EV/EBITDA: 8 vs. sector: 15). Although expected growth is also somewhat lower, at 12% and 7% (at the EPS and EBITDA levels) compared to the sector's ~13% (and the gap would be even greater if we looked at organic, weaker single-digit growth), even these figures do not necessarily justify such a large pricing gap. Our indicator-based fair value estimate is USD 32, which is lower than our previous estimate of USD 35 (primarily due to a significant decline in pricing multiples across the sector as a whole), but still offers upside potential compared to the current share price.

Investment story

- The company provides protection against cyber threats (viruses, malware, ransomware, phishing, hacker attacks) to PCs, tablets, and smartphones through globally recognized brands such as Norton, Avast, Avira, and LifeLock. Norton LifeLock acquired its rival Avast in 2022 and is now the market leader in its field under a new name, Gen Digital.

- The company has a customer base of 500 million, mostly residential, of which 65 million are monthly/annual subscribers. The company is also developing in the field of machine learning and AI, has its own patents, and already offers solutions based on these to its customers.

- The company's free service user base (>400 million) is one potential source of new subscription growth, but customer retention and increased sales through partners could also contribute to the planned average annual revenue growth of around 5% over the next three years.

- The acquisition of MoneyLion was completed last year, representing a cash outflow of $1 billion (at what appears to be fair pricing levels: 9-11X EBITDA multiple) and, subject to certain conditions, could even have a dilutive effect (with the issuance of 1.5% new Gen shares). The company operates an app offering retail financial products and has 20 million users, with little overlap with GEN's customer base. However, the emergence and spread of AI agents could pose a serious challenge to the platform's business model, which could be a significant risk that could also cloud its growth prospects.

- However, cross-selling opportunities are visible for the time being, and with annual revenues of USD 546 million, the new company could make a positive contribution (14% of that amount) from day one, and it is also profitable in terms of earnings. With the closing of the transaction, Gen began to return to its own share purchases at the end of last year (USD 300 million, 2% of capitalization), as we had expected, which had been temporarily suspended due to the acquisition.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more