Is it worth investing in the Venezuelan oil story?

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

The United States recently announced that it had successfully captured Venezuelan President Nicolas Maduro, essentially bringing a regime change in the country. Oil prices did not move significantly in response to these events, as they are not expected to affect the country's oil production in the short term. In the longer term, there is certainly scope for production expansion, but this could be a capital-intensive process, as a significant proportion of Venezuela's oil reserves are heavy crude oil, which is complex to process and transport. Of course, several oil companies could potentially benefit from the situation, which we discuss in our analysis, but this does not necessarily mean that there are great profit opportunities in the story from an investor's perspective. We also explain the reasons for this.

Maduro's removal did not affect oil prices

The United States recently announced that it had successfully captured Venezuelan President Nicolas Maduro, who had ruled the South American country for more than a decade. Delcy Rodríguez, who previously served as vice president, has taken over control for the time being and has expressed her willingness to cooperate with the US. Essentially, this means that a regime change has taken place in the country, although it remains to be seen what this will mean in the longer term. In any case, it is certain that this move has further increased the influence of the United States in the region.

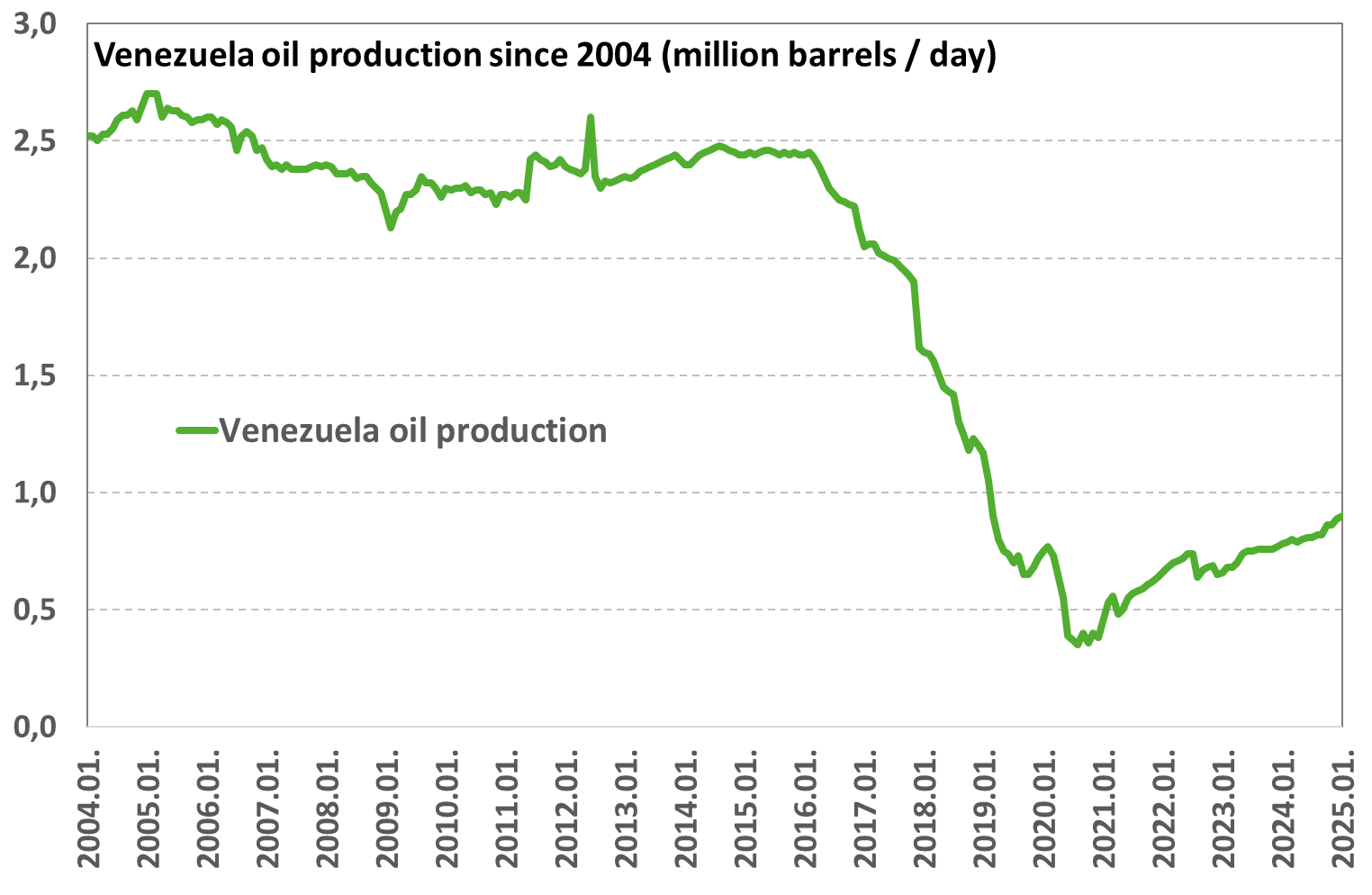

Venezuela is primarily classified as a poorer country, where, according to IMF data, the GDP per capita is around $3,000, which is only slightly more than 3% of the similar figure for the United States. Oil accounts for the majority of the country's exports, making it an important economic product. According to OPEC's December monthly report, Venezuela's oil production was around 1.1 million barrels per day, accounting for roughly 1% of global production.

The removal of Venezuelan President Nicolas Maduro is not expected to affect the country's oil production in the short term, so oil prices have not moved significantly in response to these events.

What about the longer term?

As a result of the current regime change, the country may become more open to foreign capital investment in the future, which could lead to higher oil production over time. At the end of the 1990s, Venezuela was producing nearly 3.5 million barrels of oil per day, which gradually declined under the presidencies of Hugo Chávez and Nicolas Maduro and, according to Refinitiv data, is now less than 1 million barrels.

Although Venezuela has huge oil reserves on paper (approximately 300 billion barrels, the largest in the world), this figure is rather misleading, as a significant portion of these reserves are extra-heavy crude oil located in the Orinoco oil belt, which is complex to handle, transport, and process.

There are many types of crude oil, but they are basically classified according to density and sulfur content. Accordingly, crude oil can be light or heavy in terms of density, and "sweet" or "sour" in terms of sulfur content. These properties also determine the complexity of processing. Typically, light and sweet oil (lower density and sulfur content) is priced higher than heavy and sour oil. This is because the two most important oil products, gasoline and diesel, are easier to extract from sweet and light oil.

According to data from the Rystad Energy research firm, approximately 70% of Venezuelan oil production falls into the heavy and sour category, meaning that maintaining and potentially expanding production would require significant investment. The research firm estimates that maintaining the current production level of 1.1 million barrels could cost more than $50 billion over the next 15 years. With limited costs, production could only be increased by 300,000 barrels over the next 2-3 years. In order for the country to reach 3 million barrels per day by 2040, an investment of more than $180 billion would be required, which is a very significant amount (this includes various processing plants, pipelines, and other infrastructure requirements).

Overall, it can be said that there are only limited growth opportunities for Venezuelan oil production in the short term (2-3 years). In the longer term, there may be room for more significant production expansion, but this would require significant capital investment. It is questionable whether, given the current relatively low oil prices and taking into account the country risks, the major oil companies will be willing to finance this. It should also be noted that heavy oil is also available in larger quantities in Canada, where production risks are significantly lower. Also, there are other investment opportunities available in many places outside Venezuela (e.g., Guyana, Namibia, Argentina, Brazil, etc.).

Regardless, oil company executives will certainly assess the opportunities and allocate resources accordingly, taking the risks into account. At the same time, a new Venezuelan leadership may also implement favorable changes to encourage investment (reducing state ownership, taxation and licensing procedures, etc.), but these may be more time-consuming processes.

Who can benefit from the regime change?

In recent years, international oil companies operating in Venezuela have declined significantly. Currently, Chevron (US) and CNPC (China) are practically the only major players in the country. Moreover, these companies can only operate in the form of joint ventures, in which the Venezuelan state oil company (PDVSA) holds a majority stake (based on the current structure, this may of course change under the new of regime).

At first glance, the obvious winner in this situation could be the American company Chevron, which is currently producing in the country and is therefore likely to be better able to assess the potential opportunities. However, it is worth noting that the company currently produces around 4 million barrels of oil equivalent per day (approximately 2.5 million barrels of oil with the remaining being natural gas). Therefore, any investments in Venezuela will not have a significant impact on the company, although it is obviously positive. Similar considerations apply to the possible entry of other major international oil companies (e.g., Exxon, Conoco, etc.).

However, oil service companies may fare better, given the amount of investment that would be needed to ramp up Venezuela's oil production in the coming years. It is no coincidence that following Maduro's arrest, the shares of SLB (formerly Schlumberger), Halliburton and Baker Hughes jumped significantly (by approximately 6-10%). In this regard, however, it is also worth considering the business opportunities that Venezuela may offer (and over what time frame). The fact that billions of dollars of investment would be needed to ramp up production does not automatically mean that these sums will be spent by the big oil companies (as detailed above). Regardless, in the longer term, a regime change is also positive for oil industry service providers.

Finally, it is worth mentioning the case of the American company ConocoPhillips, to which Venezuela owes more than $10 billion in compensation awarded by the ICSID following previous nationalizations. The company's assets were seized in 2007 during Hugo Chávez's presidency. Conoco's market capitalization is currently just over $120 billion, so this is a significant amount even relative to the size of the company. However, it is questionable when, how, and in what form Venezuela will pay the compensation, if it ever does (due to the high level of uncertainty, it is difficult to price this, but the regime change is also a positive factor here).

We would also like to mention certain Canadian oil companies as an interesting opportunity, whose share prices fell slightly following developments in Venezuela (e.g. Canadian Natural Resources, etc.). In this case, investors were probably concerned that Maduro's removal would lead to an increase in Venezuela's heavy oil production, which would mean greater competition for certain Canadian producers who supply similar types of oil. However, as mentioned above, this does not represent a significant volume in the short term. In this case, however, the broader oil market outlook should definitely be considered before making any investment decisions.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more