Robotics & AI: The Next Revolution

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

A profound structural transformation is emerging at the intersection of robotics and artificial intelligence — potentially one of the most significant economic shifts of the coming decades. While recent market narratives have been dominated by generative AI and software ecosystems, the next true productivity revolution is likely to take place in the physical world. Autonomous robots — rather than chatbots — may become the primary drivers of incremental economic value as demographic headwinds, supply-chain restructuring, and rapid technological advancement converge.

Robotization and automation collectively offer a long-duration structural growth story. Even though generative AI has been the central theme since its acceleration in 2022, the past several quarters have exposed the limitations and cost pressures of software-only approaches: narrowing margins, uncertain monetization, and the questioning of established business models across multiple sectors.

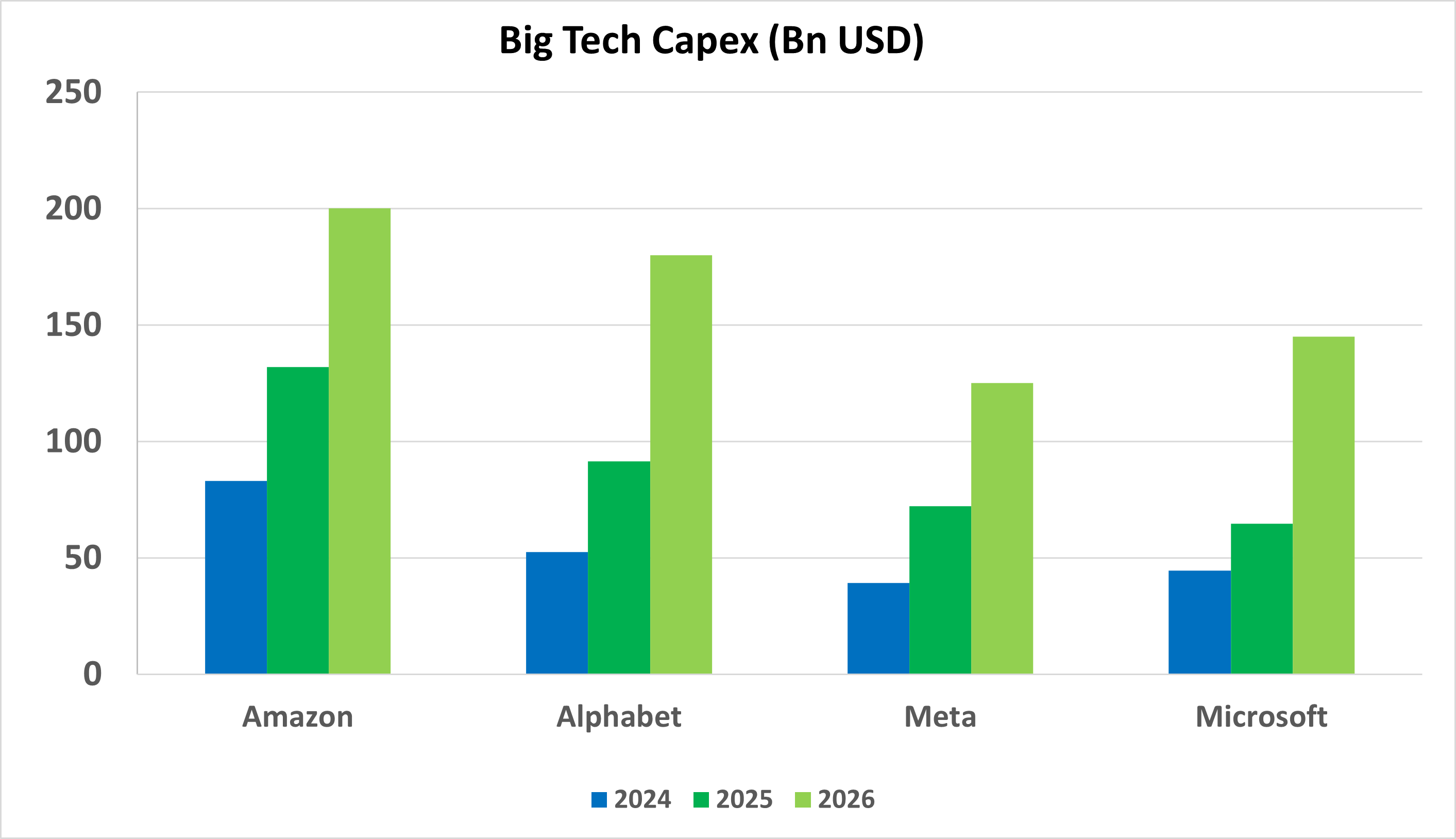

In 1Q2026, the four major U.S. technology platforms (Microsoft, Meta, Amazon, Google) guided to roughly USD 650bn of capex by 2026, equivalent to nearly three times Hungary’s annual GDP. However, investors have become increasingly skeptical that such unprecedented investments will deliver adequate returns. Mega-cap performance has recently lagged the broader market, and the software sector has come under pressure as increasingly capable AI models challenge the sustainability of existing operating models and valuation premiums.

AI’s True Potential Shifts Toward the Physical World

Despite the recent re-rating, AI’s underlying potential has not diminished—if anything, it is expanding. The narrative is shifting toward AI-enabled automation in the physical domain. Robotics may become the field where AI creates tangible economic value in the coming years, potentially at the expense of previously dominant software-centric themes.

Robotics is not a new concept: industrial robots and automated assembly lines have been transforming manufacturing since the 1960s. However, traditional robots were deterministic machines — executing only predefined, programmed actions.

AI fundamentally changes this paradigm. Models capable of simulating reasoning can now integrate structured and unstructured data, execute multi-step tasks, and match or exceed human-level performance in narrowly defined domains (e.g., autonomous driving). Continuous algorithmic and hardware innovation is reducing training and inference costs, improving energy efficiency, and enabling multimodal capabilities—processing and generating text, images, audio, and video — critical for advanced robotic systems, especially humanoids.

AI-driven robotic systems unify perception, reasoning, and action, enabling operation in unstructured environments, execution of novel tasks, and following human verbal instructions—capabilities far beyond traditional automation. Widespread humanoid deployment, however, will depend on rapid declines in manufacturing costs, scalable production capacity, and supportive policy frameworks. The replacement of human labor introduces social and political considerations as well, though these fall outside the scope of this analysis.

Powerful Megatrends Supporting Adoption

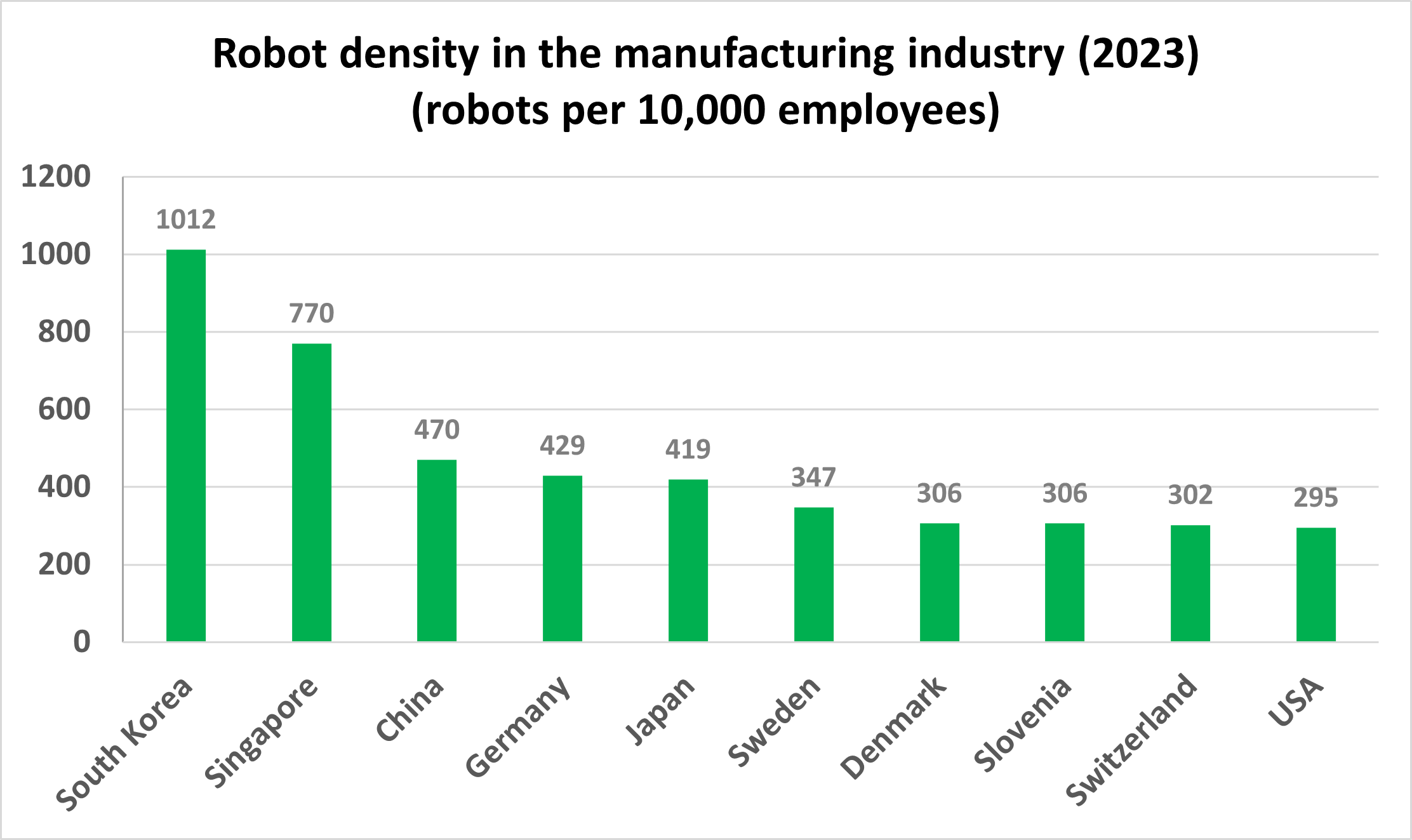

Demographic trends represent one of the most significant structural drivers. Most developed economies — and increasingly major emerging ones such as China — face declining birth rates and rapidly aging populations. Today, individuals aged 65+ comprise roughly 10% of the global population, by 2050 this share is expected to reach 16%, while the working-age population stagnates. Germany’s workforce, for example, may shrink by up to 10% by mid-century. The economic burden of eldercare will rise sharply. Unsurprisingly, South Korea, a country long challenged by demographic decline, already has the world’s highest industrial-robot density.

Urbanization will continue to concentrate populations in cities, exacerbating labor shortages in rural regions and associated industries. In parallel, workers are increasingly unwilling to perform dangerous, repetitive, or physically demanding jobs — roles well-suited for robotic substitution. Supply-chain reconfiguration also represents a major catalyst. Reshoring and near-shoring require the relocation of production to high-cost economies. Such moves are only viable with deep automation, as Western manufacturing cannot compete with East Asia on labor cost — but can regain competitiveness if robotics becomes the backbone of production.

Market Size and Growth Trajectory

Estimating the size of the robotics market is inherently difficult, given the uncertainty around the scope of included technologies (pure hardware vs. full automation ecosystems with software integration). Current estimates for 2026 range broadly between USD 50–100bn. Looking further out, most analysts forecast 15–20% CAGR through 2035.

Among the subsegments, humanoid robots may exhibit the fastest growth due to their currently small base. From roughly USD 1–3bn in 2023, the humanoid market could expand to USD 40bn by 2035 under Barclays’ base case, with a bullish scenario closer to USD 200bn. Morgan Stanley projects a potential USD 1tn humanoid market by 2050. While such long-range forecasts carry significant uncertainty, directionally the growth potential is substantial.

Importantly, this will not be a winner-takes-all market. Value creation will be distributed across the hardware supply chain, software platforms, system integrators, and component manufacturers. End-users across manufacturing, logistics, retail, healthcare, and infrastructure stand to benefit from meaningful productivity gains.

Robotization is emerging as a major multi-decade investment theme. We expect the coming years to be defined by accelerating adoption, expanding addressable markets, and an evolving competitive landscape across both hardware and software ecosystems.

Further robotics-focused analysis will follow in the coming weeks.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more