Hungary: Inflation in June declined to 1.7% YoY and still running below the expectations, but not all details are so rosy what the headline figure suggests

Related content

Uber: Steady growth wasn't enough this time

Investors have slightly reassessed Uber’s investment case following the Q2 earnings report. Although the company continues to grow rapidly, the widespread adoption of self-driving technology can only yield positive results in the long term—and it requires significant capex. In addition, the acquisition of Delivery Hero will also cost a substantial amount, leaving less money available for share buybacks and potentially resulting in more modest cash generation. In our view, however, it is better for the company to reinvest the money into its operations rather than use it for share buybacks. As a result, shareholders should expect a longer-term investment horizon when it comes to Uber.

Commodities - Technical Analysis

Strong bullish candlesticks appeared in the price action of gold and silver yesterday, following a long accumulation period. These could be enough to push the prices of the two precious metals toward a structural shift. The price of oil is following a strong retest, and a rally should occur within the next few days to sustain its uptrend. No pattern indicating a reversal has yet emerged in the price of natural gas. Copper managed to bounce off an important level, remaining in an uptrend with the potential for further new highs. Wheat and corn are also undergoing strong retests; significant gains within the next few days are needed for them to remain in their respective trends.

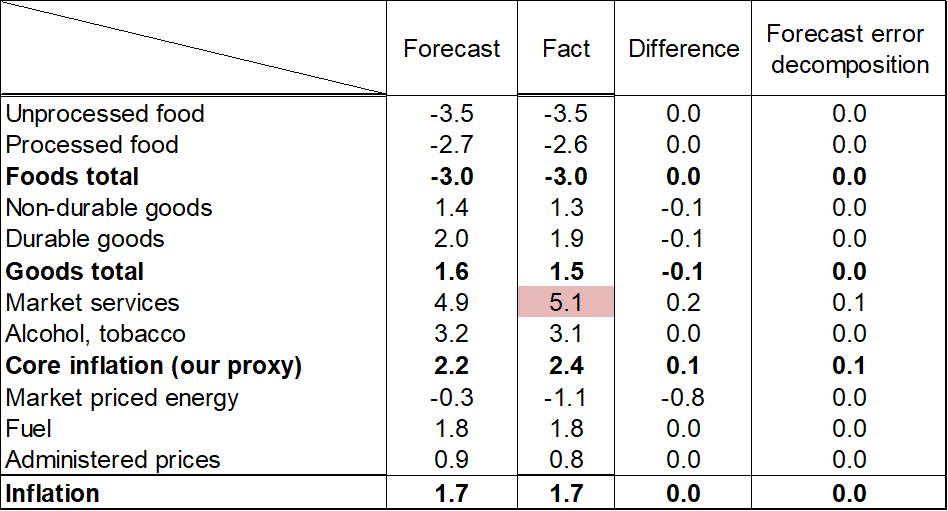

Hungary's headline inflation decreased to 1.7% year-on-year in June from 1.8% in May. The published data was lower than the consensus (1.8%) and met our forecast (1.7%). Not only did the headline CPI figure match our expectations, but there were also only minimal differences between the data and our forecasts for the major inflation categories. The only noteworthy difference appeared in market service inflation due to the unexpected MoM acceleration in catering service inflation and partial reversal of the decline in the transportation service prices (market-priced, so this category does not contain for example public transportation) observed in May.

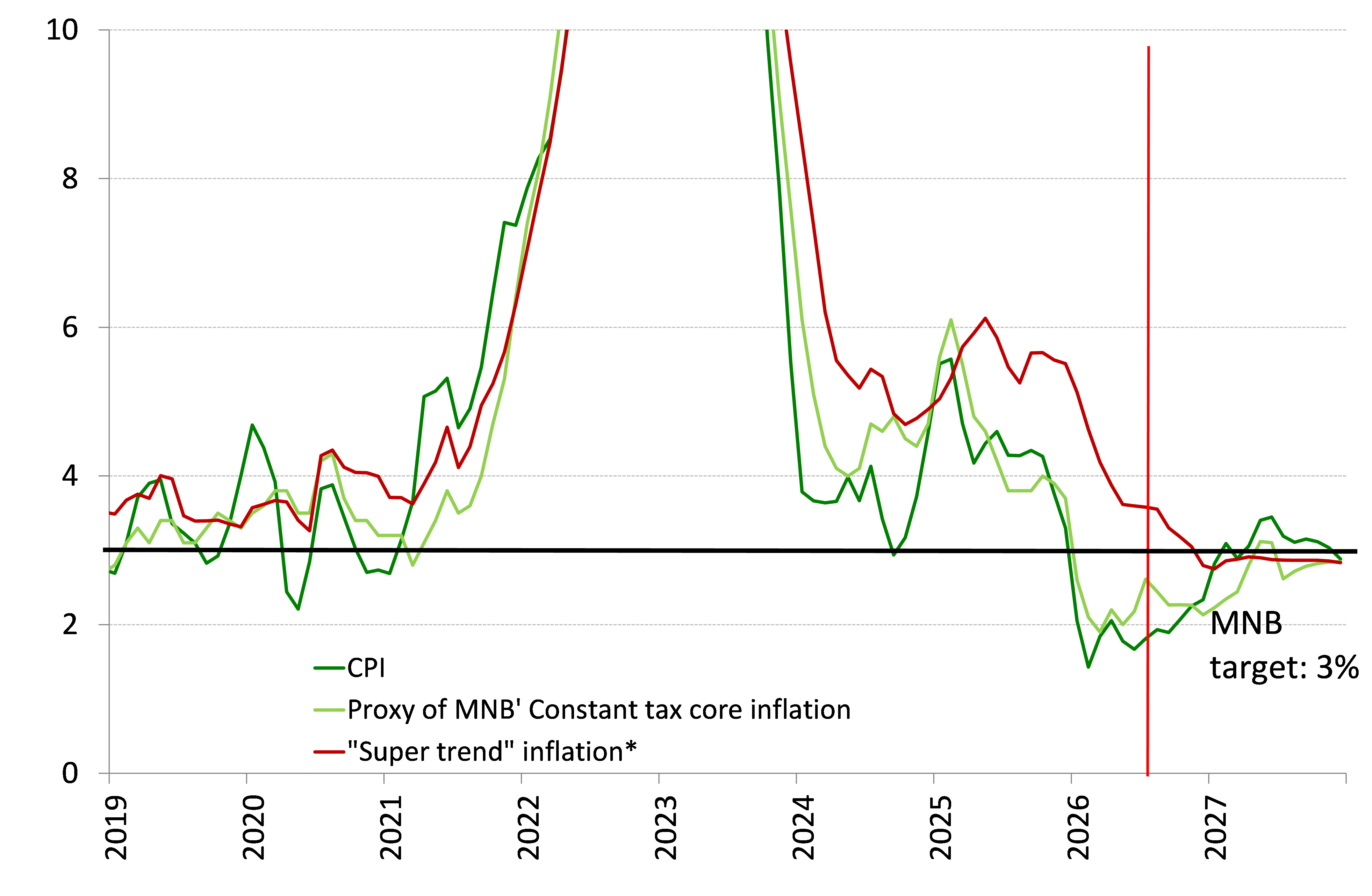

Underlying indicators remained basically favourable, but they indicated the disinflation is running out of steam. The MNB’s constant tax core inflation stagnated at 2.0%, while the sticky price inflation decreased further from 3.8% to 3.6% YoY. The core inflation indicator w/o processed foods increased from 3.0% to 3.1% YoY. Our “super trend” inflation (Chart 9) indicator that is similar to the latter-mentioned MNB indicator but it does not contain the mainly backward looking pricing telecommunication and financial services, and it is filtered from the margin cap’s effect (therefore it is not affected by any administrative measures) also increased somewhat from 2.9% to 3.2% on annualized MoM terms. That was the fourth month in a row when our ‘supertrend’ inflation indicator accelerated and it has gradually climbed from 1.7% in February to slightly above 3% in June. This level is still roughly half of the average of the last four months of 2025 (5.3%), but at the same time, the data also highlights that there is still work to be done in improving underlying inflation, as with a less favorable food inflation than this year, the headline CPI could easily return to the central bank’s current 3% inflation target (which, due to the planned euro adoption, would need to be reduced within the foreseeable future). The fact remains unchanged that households received significant income transfers before the elections, and since then consumer confidence has strengthened considerably and in May the industrial production and retail sales showed clear bottoming out signals which reinforced our view that economic activity is gradually recovering. At the same time, pricing expectations have increased in business confidence surveys. Although this is likely more of a consequence of the uncertainty related to the Strait of Hormuz, it is nevertheless a development that cannot be ignored in the context of strong consumer confidence and strong real income growth.

Due to the significant decline in oil prices and the more favourable-than-we had expected price development of the agro-commodity prices, we are lowering our inflation forecast for this year from 2.3% to 2.0% and from 3.1% to 2.9% for 2027. The main driver of the expected pickup in inflation in 2027 will be the fading (or disappearance) of the very strong disinflationary effect coming from food prices this year while we expect only minor improvements in the underlying inflationary processes. Our inflation forecast for 2027 is higher than the MNB’s figure (2.3%) and we think that for the MNB’s forecast to materialize, either food prices would need to continue to develop very favorably, or there would need to be further improvement in underlying processes, which, however, have been moving in the opposite direction in recent months.

In its most recent statement, the central bank strongly indicated that it intends to cut the policy rate in its next two rate-setting meetings. Further rate cuts, however, carry greater uncertainty. Market pricing indicates two additional rate cuts during the autumn, which is in line with our expectations. However, medium-term macroeconomic and fiscal outlook, which expected to be published in October will be crucial for maintaining the market’s initial trust in the euro adoption and for paving the way for further rate cuts. If all goes well, the key rate may decline to 5% by the end of the year. Regarding the next year’s interest rate cuts in addition to the mid-term fiscal outlook, the development of the underlying inflation processes in the last quarter of the year will also be crucial.

Inflation forecast (annual changes, %)

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more