Hungary: Inflation in May was 1.8% YoY and still running below the expectations, but not all details are so rosy what the headline figure suggests

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

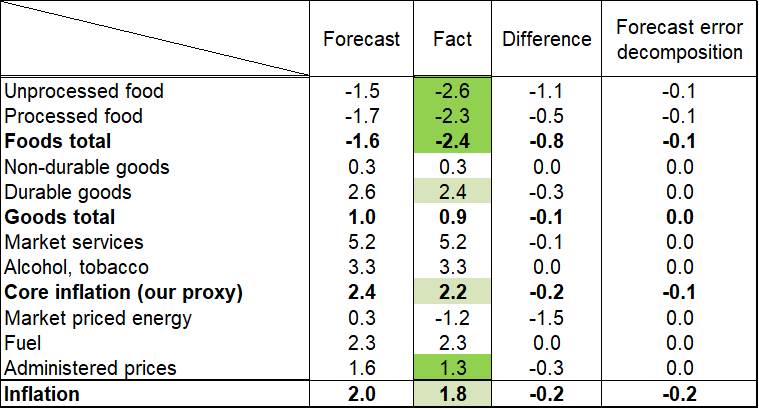

Hungary's headline inflation decreased from 2.1% year-on-year in April, to 1.8% in May. The published data was lower than the consensus (2.2-2.3% depends on the pollster) and our forecast (2.0%), as well. Mainly the food inflation, minorly the goods inflation stand behind the lower-than- expected inflation figure.

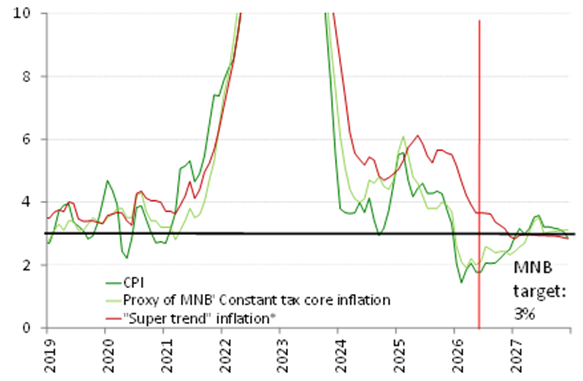

Underlying indicators remained favourable in May. The MNB’s constant tax core inflation decreased from 2.2% to 2.0% YoY, while the sticky price inflation decreased further from 4.0% to 3.8% YoY. We should highlight that the MNB’s constant tax core inflation contains some items that were affected by the margin cap measures and it also contains the mainly backward-looking pricing of telecom and financial services, which are also affected by the "voluntary" price freezes proposed by the government. Hence, we think our “super trend” inflation (Chart 9) indicator is the better underlying gauge in the current environment as it does not contain telecommunication or financial services, and it is filtered from the margin cap’s effect, therefore it is not affected by any administrative measures. The annualized MoM change of our trend inflation indicator stagnated accelerated to 3% in May from 2.6% in April. Our “super trend” indicator hit its low in February (at 1.7%) and since then it has gradually accelerated. This level is still roughly the half of the average of the last four months of 2025 (5.3%), but at the same time, the data also highlights that there is still work to be done in improving underlying inflation, as with a less favorable food inflation than this year, the headline CPI could easily exceed the central bank’s current 3% inflation target (which, due to the planned euro adoption, would need to be reduced within the foreseeable future). The fact remains unchanged that households received significant income transfers before the elections, and since then the consumer confidence has strengthened considerably. At the same time, pricing expectations have increased in business confidence surveys. Although this is likely more a consequence of the uncertainty related to the Strait of Hormuz, it is nevertheless a development that cannot be ignored in the context of strong consumer confidence and strong real income growth.

Another key issue regarding the outlook for Hungarian inflation is the sustainability of administrative price controls—namely, the capped fuel price and the margin cap on food products—as well as their impact on longer-term inflation prospects. In the case of fuel, average prices across the region are broadly in line with the current “protected” price in Hungary. Although historically Hungarian prices have been around 3% higher than the regional average, even taking this into account, the removal of the price cap would not have a significant inflationary impact. According to data collected by holtankoljak.hu, the market (non-capped) price of gasoline in Hungary is about 7% higher than the “protected” price. However, this likely overstates the true market price due to cross-pricing practices, whereby retailers compensate for lower margins on capped products. Even so, a 7% increase in fuel prices would raise inflation by only around 0.4 percentage points, implying that even in this scenario, a sharp acceleration in inflation would be unlikely.

The lower-than-expected inflation was largely driven by favorable food price dynamics. Food prices continue to decline on a year-on-year basis, despite the fact that the impact of the margin cap measures introduced in March–April last year has already dropped out of the base.

Primarily due to favorable food price developments, we are lowering our inflation forecast for this year from 2.5% to 2.3%. We leave our 2027 forecast unchanged at 3.1%. The main driver of the expected pickup in inflation in 2027 will be the fading (or disappearance) of the very strong disinflationary effect coming from food prices this year.

In its most recent statement, the central bank strongly indicated that it intends to cut the policy rate in June. Unless an event occurs in the Strait of Hormuz before the June rate-setting meeting (23rd of June) that would push oil prices above USD 150, a rate cut is highly likely to materialize. Further rate reductions, however, carry greater uncertainty. The current inflation environment provides the central bank with a good opportunity to anchor inflation expectations lower, which will be necessary to achieve the inflation level required for euro adoption. Therefore, the central bank may wait for greater clarity regarding the situation in the Strait of Hormuz, as well as for the medium-term macroeconomic and fiscal outlook due in the autumn, before proceeding further. After that, there could still be room for two additional rate cuts this year. If all of the above-mentioned factors develop favorably, the path could open next year for a more significant rate-cutting cycle, at the end of which Hungarian interest rates could converge toward euro levels.

Inflation forecast (annual changes, %)

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more