Hungary: Base effect drove inflation to 2.1% in April, underlying processes remained modest. The strong HUF could keep inflation at the target next year

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

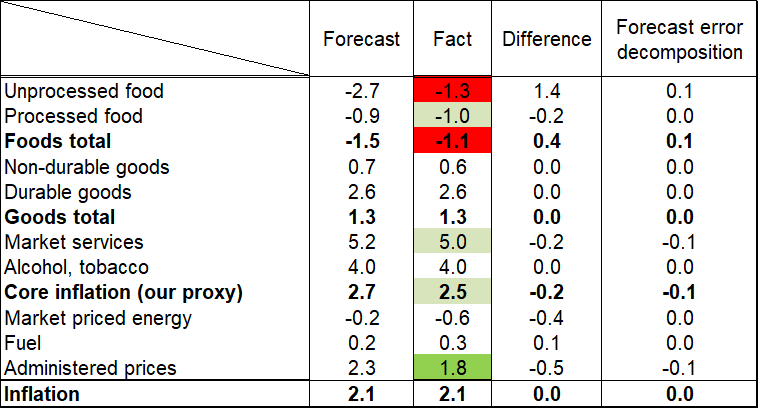

Hungary's headline inflation increased from 1.8% year-on-year in March, to 2.1% in April. The published data was somewhat higher than the consensus (2.0%) but matched with our forecast (2.1%). Food inflation accelerated significantly as the margin cap’ effect fell out from the basis.

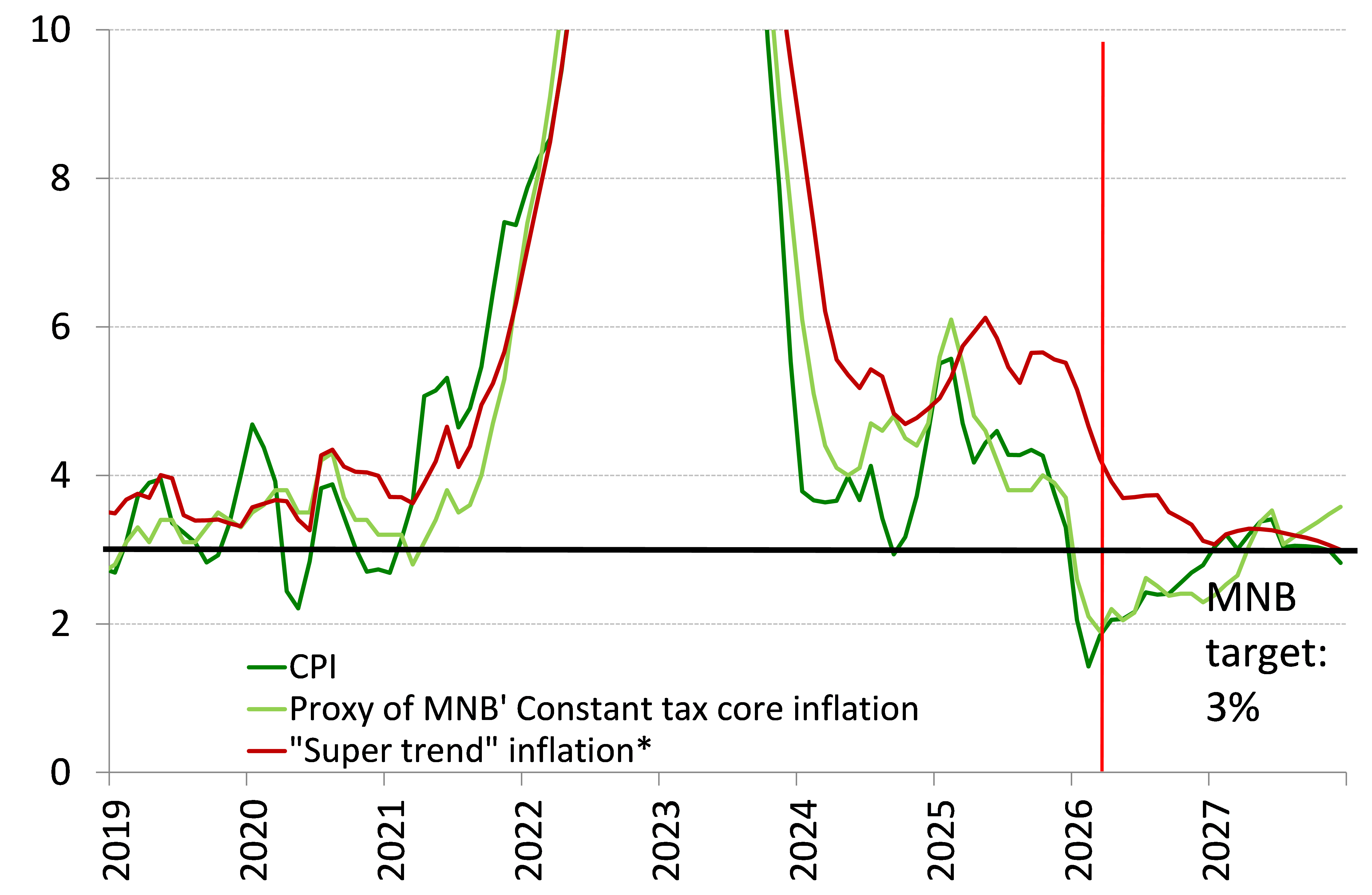

Underlying indicators remained favourable in April. The MNB’s constant tax core inflation increased from 1.9% to 2.2% YoY, while the sticky price inflation decreased from 4.2% to 4.0% YoY. We should highlight that the MNB’s constant tax core inflation contains some items that were affected by the margin cap measures and it also contains the mainly backward-looking pricing of telecom and financial services, which are also affected by the "voluntary" price freezes proposed by the government. Hence, we think our “super trend” inflation (Chart 9) indicator is the better underlying gauge in the current environment as it does not contain telecommunication or financial services, and it is filtered from the margin cap’s effect, therefore it is not affected by any administrative measures. The annualized MoM change of our trend inflation indicator stagnated at 2.6%. Our "super trend" indicator was 2.6% in the average of the first four months of 2026, which is half of the average of the last four months of 2025 (5.3%). So, we can now say with increasing certainty that the inflation risks linked to the 11% minimum wage hike and to the government's consumption-stimulating measures did not materialize, and the strong exchange rate and weak economic growth appear to have brought significant change in the re-pricing behaviour at the beginning of the year.

The most significant change compared to the previous month is that, following Tisza’s two-thirds election victory, the forint’s strength has become permanent, so we expect the exchange rate to be significantly stronger — by approximately 8% — over the forecast horizon. This alone will lower the price level at the end of next year by about 1.5 percentage points.

With regards to the effects of the war in Iran, it can be said that natural gas and electricity prices have so far developed more favourably than was assumed in the baseline scenario; however, oil prices have developed less favourably, despite the HUF having strengthened significantly in the meantime (Chart 11). It is important to note, however, that since households’ energy prices — and currently fuel prices as well — are regulated in Hungary, the direct inflationary effects of rising energy prices are minimal. The new government has announced that it intends to maintain “protected prices” on fuel; however, to avoid supply issues, it plans to do so through a VAT reduction rather than the current simple price cap measure. According to our calculations, the current “protected fuel price” is consistent with an oil price of approximately $82–84, a level to which the oil price could return before the end of the year based on the forward oil price curve. However, despite the price cap for households, the impact of rising oil prices will still passthrough into consumer prices via the production chains. According to our calculations, the rise in oil prices measured in HUF compared to the pre-Iran war situation could increase this year’s inflation by approximately 0.2 percentage points through these second-round effects. However, there is a significant risk that if a satisfying agreement is not reached soon regarding the Strait of Hormuz, oil prices could rise well above current forward prices. In that case, the sustainability of protected fuel prices would be seriously questioned, which would significantly amplify the inflationary impact of the war in Iran.

However, the general disinflationary effect come from the stronger exchange rate will be much stronger than the second-round effects of the higher oil prices and the incoming data are also favourable, so we are lowering our inflation forecast for this year to 2.5% from the previous 2.9%. The inflation will gradually accelerate in the remaining part of the year but it remains just below the 3% at the end of 2026. In 2027 it could accelerate further and it can be 3.1% on the average of the year, mainly due to temporary factors. The reason for this is that, following favourable agricultural prices last year, we expect prices to rise this year, which may be further bolstered by the impact of the war in Iran (e.g., fertilizer shortages). However, the impact on consumer food prices will be slower to materialize and will affect next year much more strongly. We also expect that, following the phase-out of the protected fuel price, the excise duty increase – originally scheduled for July – will take effect, which will also primarily affect 2027. In addition, we expect that price increases postponed this year for certain government-regulated services will take place in 2027. Although inflation will temporarily rise above 3% in 2027 — peaking at somewhere between 3% and 3.5% in late spring — it could fall back below 3% by the end of 2027.

It is important to note, that our current forecast does not yet account for a significant improvement in inflation expectations. Various business confidence surveys currently show that expectations regarding price developments are rising (presumably due to the war in Iran), so we remain cautious on this front for now. But we should highlight as a positive risk, if the new government is able to strengthen further the euro adoption expectations in the remainder of the year, domestic inflation expectations could also decline significantly.

In April, inflation was 0.4 percentage points lower than the central bank had forecast in its latest inflation report. This gap could widen even further in May, as it currently appears most likely that the protected fuel price will not be phased out this month. Given all this, as well as the much stronger exchange rate, we expect the central bank to significantly lower its inflation forecast in the next inflation report in June. If there is no drastic deterioration in Hungary’s risk assessment by the June meeting, the Monetary Council may decide, based on a three-month period, that there has been a sustained improvement in the risk assessment. Nevertheless, the Iranian war situation remains a significant risk, as the inflationary effects of the war are not linear. If a satisfying solution to the Strait of Hormuz issue can be found by the June meeting, the central bank will most likely begin cutting interest rates at that time. Otherwise, however, it may continue to maintain the current interest rate level until the situation in the oil market stabilizes. If interest rates are cut at the June meeting, it is likely that there will be an opportunity for (at least) one more rate cut this year.

Inflation forecast (annual changes, %)

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more