AI-driven demand boosted Palo Alto

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

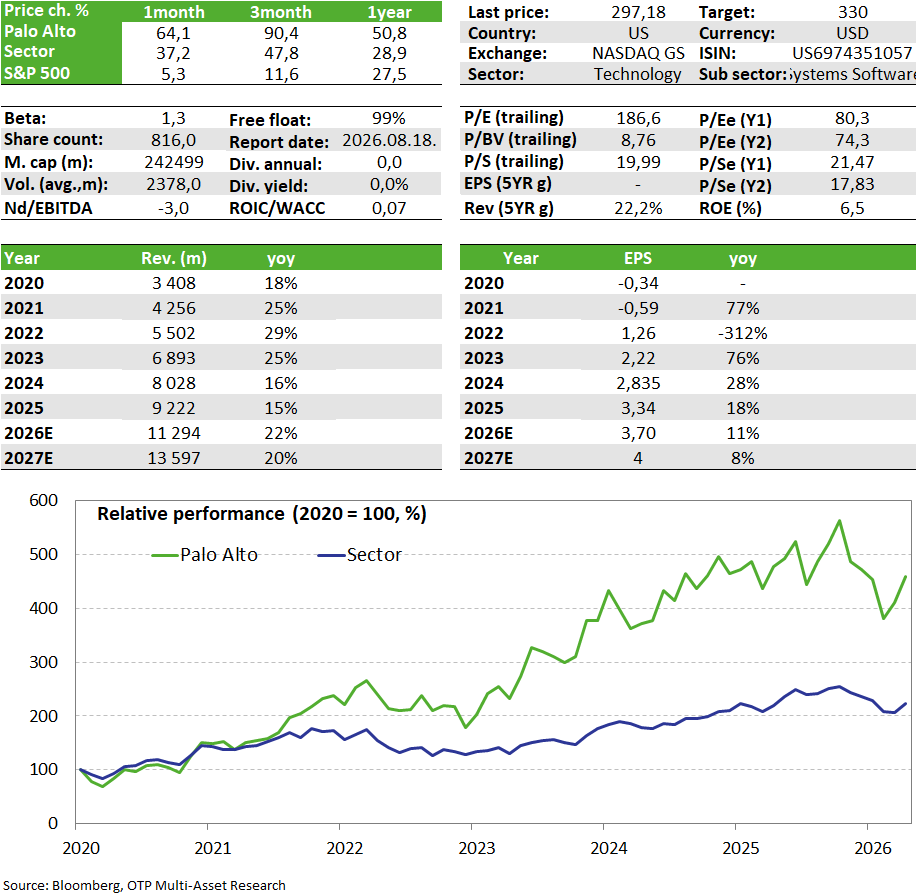

Yesterday after the market closed, Palo Alto, the market-leading cybersecurity company, published its earnings report. The company exceeded analysts’ estimates across the board and issued a more optimistic outlook for the current fiscal year than expected. The strong results were primarily driven by growing demand for cybersecurity services generated by the increasing use of AI. The company’s earnings report sends a positive message to all industry players, demonstrating that, contrary to fears at the beginning of the year, the spread of AI is fueling accelerated growth in the cybersecurity sector. We continue to view the fundamental outlook for this stock—which is also included on our Equity Top Pick List—as strong, and are therefore raising our fair value estimate from $215 to $330.

Quarterly Report

Palo Alto’s stock has risen nearly 60% over the past month, propelling the company to become one of the leading players in the cybersecurity sector as it rebounded from its losses at the start of the year. This turnaround was driven by a shift in the industry narrative, during which artificial intelligence evolved in investor perception from a risk factor to a growth catalyst. However, following the rally driven by improving sentiment, the company also had to validate the heightened expectations from a fundamental perspective, which, based on the latest earnings report, it has largely done.

The company reported revenue of $3 billion for the previous quarter (+31% year-over-year), exceeding analysts’ expectations of $2.94 billion. This growth was supported by the acquisitions of CyberArk and Chronosphere, but organic growth also accelerated thanks to the use of hardware firewalls to secure data center deployments. In addition, as a result of the increased deployment of AI agents at enterprises, subscription revenue from securing these agents also grew at a remarkable rate. The company’s remaining performance obligations (RPO, contracted but not yet recognized revenue) increased by 36% to $18.4 billion (compared to an expected $17.9 billion).

Adjusted earnings per share were 85 cents in the previous quarter, compared with the consensus estimate of 79 cents. Looking ahead, the company raised its outlook for the current quarter as well as its full-year guidance. For fiscal year 2026, it expects revenue of $11.42 billion, exceeding estimates of $11.29 billion, while earnings per share could reach $3.78 instead of the expected $3.70. The forecast for a 59–60% increase in annual recurring revenue from next-generation security services exceeds preliminary expectations by 400–500 basis points. Furthermore, RPO could approach $21 billion, compared to the expected $20.3 billion, driven by bundled offerings and cross-sales to customers of acquired companies.

Overall, Palo Alto’s earnings call demonstrated that the widespread adoption of AI among companies is driving demand for the cybersecurity firm’s services, which is positive news for the entire industry. At the same time, following a nearly 60% rise in the stock price over the past month, the stock has reached stretched valuation levels, with the market effectively pricing in “flawless” fundamental performance. Although the company exceeded expectations on every major metric and its guidance was also favorable, profit-taking began following the earnings release due to overpositioning.

Investment Thesis

Palo Alto benefits from all major, long-term structural technology trends—including platformization, the spread of cloud-based IT architectures, artificial intelligence, and quantum technology. Its competitive advantage is supported by its extensive enterprise customer base, strong distribution channels, one of the market’s broadest and most integrated security platforms, and its leading market position.

The company is particularly well-positioned in key growth segments, such as the SASE (Secure Access Service Edge) solutions market, which is benefiting from the rapid expansion in demand for cloud-based networking and edge security systems. Palo Alto’s platform strategy deliberately focuses on enterprise customers, promoting deeper integration and long-term customer retention, which also significantly reduces the likelihood that its solutions could be easily replaced—even through AI-based automation.

Based on our current understanding of the company’s product and service portfolio, only a marginal portion of it may be directly exposed to the potentially disruptive effects of artificial intelligence. Even in these areas, a collaborative approach to development appears to be emerging, as indicated, for example, by Anthropic’s Glasswing project and developments surrounding the Mythos model. In light of this, it cannot be ruled out that Palo Alto Networks will eventually integrate Anthropic’s AI solutions into its existing product portfolio, which could even support further growth in demand.

In addition, the company has a particularly attractive presence in the field of AI agent security, especially following its acquisition of CyberArk. Through this acquisition, Palo Alto has integrated one of the most significant players in the identity and access management market into its ecosystem, which provides a strategic advantage in safeguarding the security of autonomous and AI-based systems in the future.

Valuation

The growth outlook is in line with that of its direct competitors: for the 2026–2028 period, the analyst consensus forecasts average annual revenue growth of approximately 20% and FCFF growth exceeding 20%. What stands out are the margins and FCFF growth, and there is room for further expansion on this front in the coming years following the acquisitions.

For software stocks, the so-called “Rule 40” figure is of particular importance; it is calculated as the sum of revenue growth and the FCFF margin, and companies that achieve a value above 40 over the long term outperform their competitors, Palo Alto stands out here with a value of over 60, which is expected to remain sustainable in the medium term as well. All of this may justify a premium valuation, although the company is currently trading at higher multiples compared to its competitors—a situation that may be supported by its strong market position. In addition, the company has a net cash position.

Risks

One of the primary structural risks affecting the cybersecurity sector as a whole is the rise of artificial intelligence, which has the potential to transform industry business models and dampen long-term growth, margins, and predictability. Palo Alto currently holds strong positions in segments that are relatively more protected from AI, such as network security, endpoint protection, and identity security. However, if AI-based solutions were able to meaningfully enter these markets and offer alternatives, it would result in increased competition and declining margins. It is also worth mentioning the integration risks arising from the acquisition of CyberArk.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more