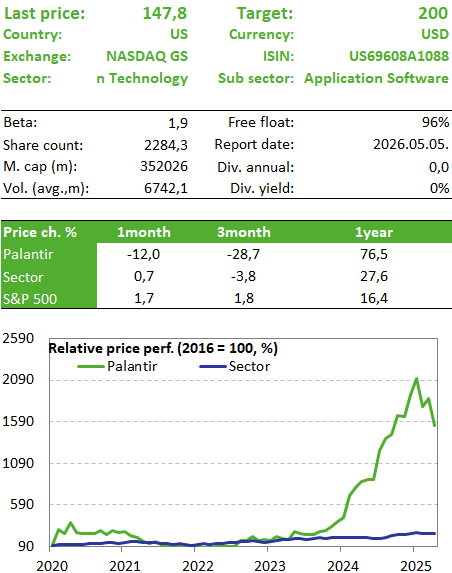

Palantir isn't slowing down

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Palantir has delivered another impressive quarter: while its revenue jumped 70 percent and it posted record profits, the number of orders from both government and corporate clients continues to grow at an unprecedented rate. The company is operating extremely profitably, and the surging demand for AI-based software points to an optimistic outlook through 2026.

Quarterly Flash Report

Palantir has posted another record quarter as demand for its AI-powered software solutions remains strong. Revenue jumped 70% to $1.4 billion, while net income came in at $609 million.

The company operates with an outstanding margin, and last year it even managed to improve on that. In the fourth quarter of 2025, the operating margin was 57 percent. Palantir is truly unique in that it combines 70% growth with a 57% operating margin—in other words, there is little indication that this massive growth is accompanied by margin erosion.

U.S. government revenue rose by 66% in Q4 2025, driven by increased defense spending. But even this impressive figure is dwarfed by the 137% surge in corporate sector revenue. The total number of clients rose by 34% to 954, and the value of outstanding orders exceeds $11 billion.

For this reason, management is also optimistic about 2026, with total revenue expected to grow by 61 percent ($7.2 billion) and the enterprise segment by 115 percent. The latter indicates that management does not currently foresee any slowdown in growth. And, of course, all the numbers came in better than analysts had expected.

The company’s strong connections in Washington also helped it secure several major government contracts, including a $448 million contract with the Navy in January to provide improved data for the maintenance and development of nuclear submarines.

However, criticism has also come from the other side of the political spectrum regarding Palantir’s collaboration last year with Immigration and Customs Enforcement (ICE). ICE signed a contract with the company to use its technology in applications designed to locate and track immigrants slated for deportation from the United States. Events in Minneapolis could even put the company in the crosshairs, but for now, this has had no impact on its financial figures, and presumably should not have any.

The only "weak spot" is the international market, where revenue grew by "only" 22 percent—a figure that isn't particularly strong for Palantir and indicates that this story is primarily focused on the U.S.

Of course, we are aware of the stock’s valuation and that many consider it too high, but we don’t think that alone is a reason to miss out on this growth story. The past few months have also seen significant price swings, but we’ve grown accustomed to that.

Investment thesis

- Palantir stock offers an opportunity to ride the AI momentum. The company is expected to grow its revenue and profits by an average of 30–40 percent over the next four years; it operates with a net profit margin of over 40 percent, generates free cash flow, and holds a net cash position.

- If the company can maintain its dominant position in the government sector while also achieving significant growth in the corporate sector (which it has managed to do so far), then its extreme valuation could persist for a long time, since in this optimistic scenario, the valuation could fall rapidly as a result of a sudden surge in profitability

Risks

The biggest risk is that the stock is currently trading at an extremely high valuation, so if it fails to deliver on its growth targets, a sudden, significant drop in the share price is not out of the question. Even amid a generally negative market sentiment, the stock could easily plummet by 40–50%.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more