The wind is blowing Orsted's sails in the right direction

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

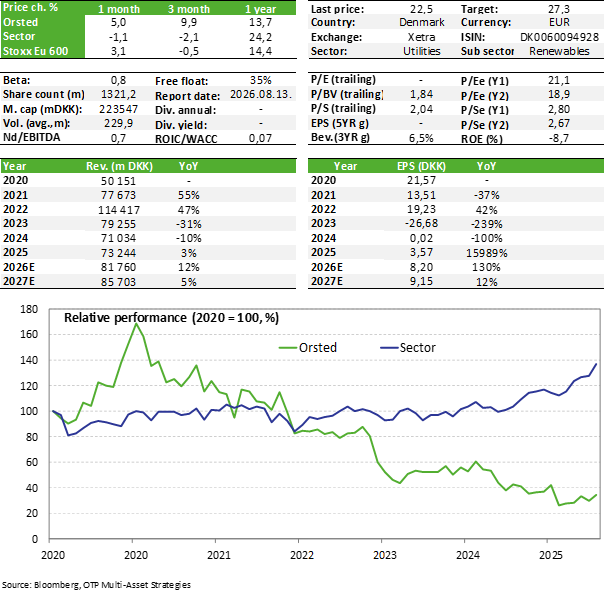

The Danish renewable energy company, Orsted released its first-quarter figures, which were mixed. The company beat analysts’ expectations in terms of both revenue and EBITDA, although its net income fell short of the consensus. Regardless, project developments are proceeding as planned despite some minor delays, while the liquidity position can be described as adequate. In light of the results, management is maintaining its 2026 forecasts. Overall, Orsted is on track as expected, so we are keeping the stock on our Equity Top Pick List for now.

Quarterly report

In the first quarter, Orsted generated revenue of DKK 27.6 billion (approx. USD 4.4 billion), which was 33% higher year-over-year and 25% above analysts’ expectations. EBITDA was DKK 9.5 billion (+8% year-over-year), which also slightly exceeded the expected DKK 9.2 billion. In contrast, adjusted earnings per share of DKK 1.98 fell short of the consensus estimate of DKK 2.95. However, the latter was primarily due to a larger impairment charge and tax-related factors. The impairment charge is largely attributable to the company’s two U.S. offshore wind projects (Sunrise and Revolution) and is due to the rise in long-term U.S. interest rates (higher WACC).

Meanwhile, the company also made good progress on its project developments during the quarter. Among the U.S. projects that had previously encountered difficulties, Revolution Wind began delivering power to the New England grid in March (704 MW capacity, 50-50% joint ownership), while the first wind turbines were successfully installed near New York for the Sunrise Wind project. In the former case, the project is 94% complete, while in the latter it is 47% complete. In parallel, Orsted’s European (United Kingdom, Germany, and Poland) and Asian (Taiwan) projects are also progressing, although the company reported minor delays in two developments. In our view, these delays do not appear significant at this stage. Overall, more than 30% of the total 8.1 GW project portfolio could be completed this year, while the remaining 70% is expected to be completed by Q1 2028. Orsted’s wind power generation could therefore expand significantly over the next two years (current total capacity is 18.8 GW).

In light of the first-quarter results, the company’s management is maintaining its 2026 guidance. Accordingly, Orsted’s full-year EBITDA could exceed DKK 28 billion, while capital expenditures are expected to remain in the range of DKK 50–55 billion. At the end of the quarter, cash reserves stood at nearly DKK 80 billion (DKK 28 billion in cash and DKK 50.7 billion in securities). Additionally, operating cash flow in Q1 was approximately DKK 6.5 billion, while capital expenditures totaled DKK 8.2 billion. Taking these factors into account, there does not appear to be a problem with financing investments, although free cash flow will naturally remain negative for some time. In addition, a credit facility of more than DKK 30 billion is available (total liquidity of DKK 116.6 billion).

Orsted’s total debt stood at DKK 104 billion at the end of March, while net debt was only DKK 21 billion (the net debt/EBITDA ratio is thus currently below 1x based on the EBITDA expected for 2026). Of course, with investment needs remaining high, debt ratios are expected to rise. We note that 93% of the debt is fixed-rate, and its maturity profile is relatively favorable. Nearly 70% of bonds and bank loans mature in 2029 or later—that is, after the expected completion of current projects—while DKK 9.5 billion of these will mature over the next two years.

Valuation

Orsted’s valuation cannot be considered high as based on the expected 2026 EPS, the P/E ratio is 21.1x, while based on the 2027 figure, it is 18.9x. The EV/EBITDA ratio is 8.7 times based on 2026 EBITDA, while it is 8 times based on 2027 EBITDA.

Overall, Orsted is on track as expected and project developments are proceeding smoothly despite minor anticipated delays, and there are no signs of liquidity issues. Taking all this into account, we are maintaining the company’s shares on our Equity Top Pick List with unchanged target price.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more