Danish renewable energy giant poised for significant growth

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

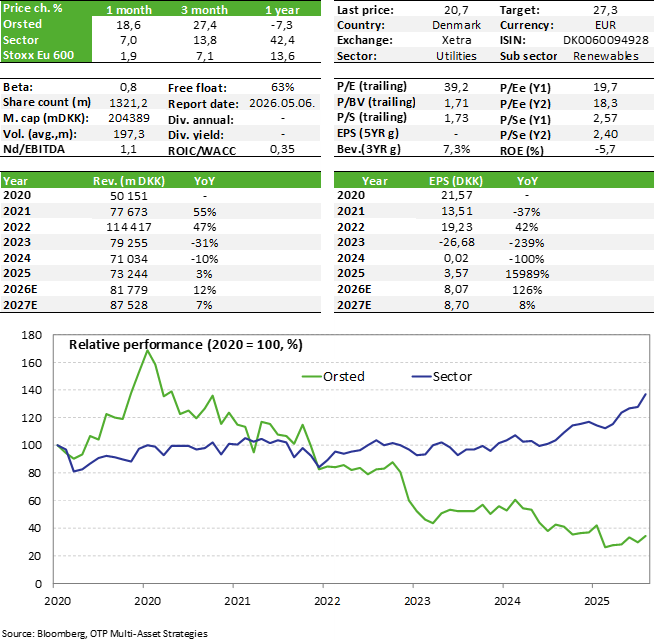

Orsted, the industry leader in offshore wind power generation, has had a difficult few months financially. The company carried out a gigantic capital raise last fall, as the Danish utility company ran into liquidity issues due to significant investment expenditures. However, thanks to the capital raise and the sale of some assets, the balance sheet structure has strengthened in recent months, providing an adequate foundation for the completion of its significant project portfolio. If everything goes according to plan, Orsted's profits could jump significantly in the coming years, while the valuation of its shares is not particularly high and its existing power generation portfolio is already sizable. In the more defensive utility sector, it is relatively rare for a company to have significant growth prospects. Another positive factor is that the Danish state is the majority owner of the company. We are therefore adding the shares of Orsted to our Equity Top Pick List.

Introduction

Orsted is a Danish utility company that primarily focuses on renewable energy production, as well as electricity and gas trading. The company is one of Denmark's largest, with a market capitalization of over USD 30 billion. Most of its electricity production comes from offshore wind farms and a smaller portion from onshore wind farms, solar energy, and biomass. It is also worth mentioning that the Danish state is the largest shareholder in the company with a 50.1% stake, while Norway's Equinor also owns 10%.

The company's total power generation capacity is currently 18.5GW, of which approximately 55% is offshore wind power, 34% is onshore wind power, solar power, and energy storage, and 11% is biomass. In addition, there are a considerable number of projects under construction (approximately 8.9GW), primarily related to offshore wind power, so the growth prospects are strong. If Orsted can complete these projects on time, its power generation capacity could increase by approximately 45% to 27GW by 2028.

Focus on offshore wind power generation

As already mentioned, a significant portion of Orsted's power generation capacity and projects under construction are related to offshore wind power. The Danish company is the largest global player in this field and has decades of experience (Orsted also built the world's first offshore wind farm in 1991).

Offshore wind energy is a relatively small segment within renewable electricity generation. According to data from the International Energy Agency (IEA), this type of energy accounted for less than 2% of renewable capacity in 2024 (solar energy and onshore wind energy dominate production). However, the growth prospects for this sector are favorable, with the IEA forecasting that offshore wind capacity could reach 230GW by 2030, compared to 83GW in 2024. China is expected to be the main driver of this growth, but the European market is also poised for dynamic expansion, where Orsted clearly has a significant advantage. It is also worth noting that in January, nine European countries signed an agreement on offshore wind energy, under which 15GW of capacity would be built annually in the North Sea between 2031 and 2040 (and 300GW of capacity by 2050). For comparison, at the end of 2024, European offshore wind capacity was approximately 37GW.

Orsted's offshore wind capacity currently stands at 10.2GW, with a significant portion located in Europe (mainly in the UK). In addition, 8.1GW of the 8.9GW project under construction is related to offshore wind power, which means that this will account for a significant portion of future growth. The positive news is that some of the projects are already basically complete or at an advanced stage (approx. 2.5GW), while others are expected to be completed by the second half of 2027.

Two of the company's offshore wind projects are in the United States (Sunrise and Revolution), where implementation has ran into difficulties on several occasions due to suspension orders issued by the Trump administration. Most recently, in December last year, Orsted was ordered to halt work, but a few weeks later, the relevant courts authorised the continuation of work on both projects (while the underlying lawsuit progresses). It is worth noting that the 704 MW Revolution wind farm is already nearly 90% complete, while the 924 MW Sunrise project is 45% complete. Once completed, the former will supply electricity to Connecticut and Rhode Island, while the latter will supply the State of New York under long-term contracts. Obviously, there are still uncertainties surrounding the implementation of the two US projects, but on the one hand, there have been no shutdowns lasting longer than a few weeks so far, and on the other hand, they account for "only" 18% of the total project portfolio.

Financial position, debt and valuation

The company published its annual report on February 6, which was broadly in line with analysts' expectations. Revenue grew slightly on an annual basis, adjusted EBITDA stagnated, and despite Q4 losses, the company remained profitable. Another positive development is that 2025 EBITDA was within the previously expected target range (DKK 25.1 billion vs. DKK 24-27 billion expected). According to management, EBITDA could exceed DKK 28 billion in 2026 and DKK 32 billion in 2027, in parallel with the completion of projects currently under construction. According to the company's previous estimates, the completion of the entire project portfolio under construction could result in EBITDA generation of approximately DKK +11-12 billion by 2028 (approximately +45% compared to the 2025 figure).

The company has no debt problems, with net debt at DKK 29 billion at the end of 2025 and gross debt at DKK 116 billion. The maturity structure of its liabilities is relatively favorable, with more than 60% due in 2029 or later, while more than 90% of its debt has a fixed interest rate. The net debt/EBITDA ratio is therefore only around 1.

However, it should be noted that Orsted carried out a gigantic capital raise last fall, as the Danish utility company encountered liquidity issues due to the capital requirements of its numerous projects under construction. As a result, the company managed to raise approximately DKK 60 billion in capital at a 67% discount resulting in a 115% share count increase. On a positive note, the majority owner, the Danish state, and Norway's Equinor also participated fully in the capital raise. The company also announced in early February the sale of its European onshore energy production portfolio for more than DKK 10 billion (which is not a significant part of its total power production portfolio, with an operational capacity of 578 MW). In addition, Orsted sold partial stakes in two projects under construction (Hornsea 3 and Changhua 2).

The above-mentioned transactions resulted in a significant strengthening of the balance sheet structure, a reduction in capital investment requirements, and a significant improvement in liquidity. For example, according to the company's annual report, investment needs for 2026 are expected to be between DKK 50 and 55 billion, while liquidity, including available credit lines, already exceeded DKK 130 billion at the end of December. Overall, it appears that Orsted has successfully managed to overcome most of its financial problems, although this has come at a steep price.

The company's valuation is not particularly high, the P/E ratio is ~18x calculating with 2026 expected EPS, while EV/EBITDA is ~8x.

Investment story

Orsted has gone through a relatively difficult period financially, as the company overextended itself in terms of investment requirements. As a result, they have been forced to carry out a large capital raise and several asset sales in recent months. However, following the successful completion of these measures, the company's liquidity and balance sheet structure have strengthened significantly, providing sufficient coverage for the completion of the project portfolio currently under construction. The implementation of these investments will result in significant growth in EBITDA and profit generation, while debt levels seem manageable and the existing energy production portfolio can be already considered strong. At the same time, the company's valuation is not high at current levels. In addition, with the gradual reduction of investment needs, financial flexibility may also increase (e.g., dividend payments, share purchases, etc.). Among the risks, of course, the two US offshore projects are worth mentioning, which are at an advanced stage, but further government obstruction cannot be ruled out. Taking all this into account, we are adding the shares of Orsted to our Equity Top Pick List.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more