Novo Nordisk: The Pioneer in Obesity Treatment Regains Momentum

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

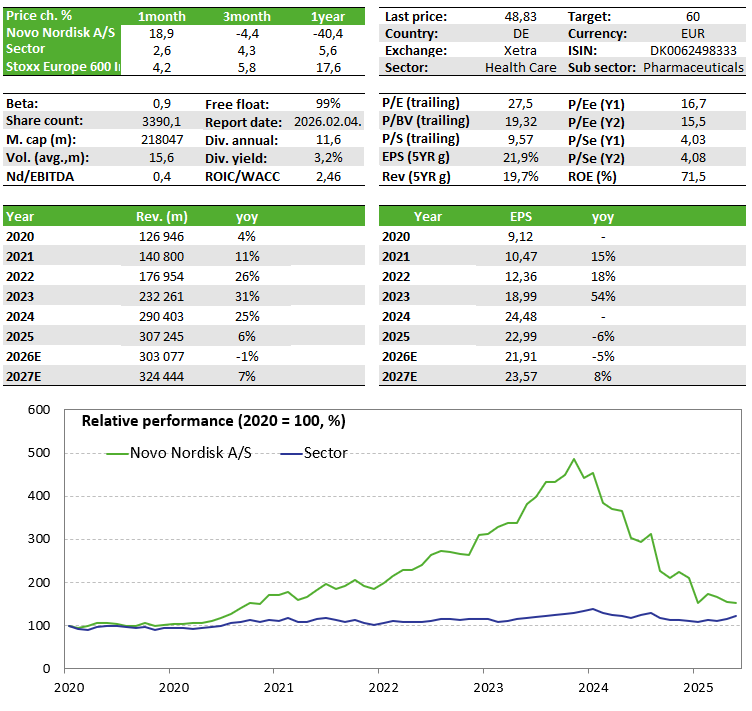

Novo Nordisk, a pioneer in anti-obesity medications, delivered exceptional performance for years, but more recently faced significant challenges. Profit warnings, capacity constraints, and intensifying competition from Eli Lilly pushed the share price to multi-year lows. However, since August 2025 the company has been led by a new CEO, who initiated strategic restructuring and cost-cutting measures, while the approval of the oral Wegovy tablet may provide new tailwinds for the Danish pharmaceutical giant. Following last year’s de-rating, the stock now trades at attractive valuation levels; and although the growth outlook is no longer as strong as in prior years, its outstanding profitability profile remains intact. As a result, we are adding Novo Nordisk to our Preferred Stock List.

Company Overview

Novo Nordisk is a Danish pharmaceutical company and a global leader in diabetes and obesity treatment. Its core products include insulin and GLP-1-based therapies, such as Ozempic and Wegovy, which also play a crucial role in managing cardiometabolic diseases (hypertension, high cholesterol, diabetes). The company also participates in treatments for rare diseases and hemophilia, although these areas contribute only modestly to revenue. Novo Nordisk operates subsidiaries in around 80 countries, and distributes its products in approximately 170 countries.

From 2021 onward, Novo Nordisk shares entered a strong upward trajectory as the company became the pioneer of obesity treatment, with the rally continuing until the first half of 2024. Thereafter, the stock began to decline due to intensifying competition from Eli Lilly, inflated expectations, and capacity issues affecting supply.

In November of last year, the share price fell to its lowest levels in four years, as the company issued several profit warnings in 2025. This prompted investors to significantly reprice the stock. However, around current levels the valuation appears compelling, and a notable reversal in market sentiment emerged during the holiday period, potentially marking a local bottom.

Investment Thesis

Since August of last year, Novo Nordisk has been under the leadership of its new Chief Executive Officer, Maziar Mike Doustdar, a long-tenured executive with more than a decade of senior-level experience within the organization. Under his direction, the company has embarked on a comprehensive organizational restructuring, reallocating resources and discontinuing several R&D initiatives deemed less strategically relevant. Operational efficiency and cost rationalization have also become central priorities, highlighted by the announcement of approximately 9,000 workforce reductions shortly after his appointment.

The CEO transition - and the clear acknowledgment that meaningful operational adjustments are required - has the potential to act as a constructive catalyst for the share price. While corporate reorganizations typically unfold gradually and are often accompanied by execution risks, our current assessment remains cautiously constructive.

The Weight-Loss Tablet Has Arrived

For Novo Nordisk to reclaim its prior momentum, successful drug development remains essential. Positive news arrived in late December 2025, when the U.S. FDA approved the oral Wegovy tablet for chronic weight management. Sales began in the U.S. in January at a starting price of USD 149 per month, with a higher-dose version priced at USD 299.

This development is important because the tablet format greatly expands the potential market, and Novo Nordisk is effectively the first mover in this segment; Eli Lilly has not yet received approval for its own oral obesity drug, although it is expected to secure authorization this year. Even so, Novo retains an early advantage.

The oral formulation may also help retain patients who previously used injectable GLP-1 therapies, as many patients tend to regain weight after stopping injections. A tablet option could therefore support more sustainable revenue streams.

However, meaningful uptake in tablet sales will take several years, and any indication - such as emerging manufacturing constraints - that could limit volume growth may introduce short-term volatility in the share price. Analysts currently expect the Wegovy tablet to generate around USD 1 billion in revenue this year, rising to USD 2.2 billion next year.

In addition to the tablet, the higher-dose Wegovy 7.2 mg injectable formulation is also under regulatory review. This could further expand the addressable patient pool. The EMA has already issued a positive opinion, and the FDA filing has been submitted under an accelerated pathway, suggesting both European and U.S. approvals are expected during 2026. News flow related to this product may also have significant share-price implications.

Another key asset is CagriSema, which combines two active ingredients targeting weight loss and type-2 diabetes. The product is currently being evaluated in a head-to-head study against Eli Lilly’s competing therapy. The results—expected in the first quarter of this year—could prove decisive in shaping future competitive dynamics.

Financials and Valuation

Novo Nordisk continues to operate with an operating margin exceeding 40%, while its net profit margin is expected to remain in the 32–34% range over the next five to seven years—levels that are considered highly attractive by sector standards. Although analysts materially reduced their growth expectations following last year’s profit warnings, revenue is still projected to expand at an average annual rate of approximately 6% over the next five years, with EPS expected to increase by roughly 6.5%. Should the company successfully execute its cost-reduction initiatives and its product pipeline deliver in line with expectations, these conservative forecasts may ultimately prove achievable or even conservative.

The company’s valuation has compressed meaningfully over the past year as growth moderated. Shares currently trade at a forward P/E multiple of roughly 14–15x, which is not elevated and appropriately reflects the more tempered growth outlook. However, relative to Novo Nordisk’s structurally high margin profile, the current valuation appears somewhat undemanding. In light of this, we are adding Novo Nordisk to our Preferred Stock List.

- Intensifying competition: One of the primary drivers of the recent share-price decline was Eli Lilly’s superior product performance, which eroded Novo’s initial advantage. Additional new entrants in the obesity-drug market could pose further challenges, although this risk appears limited in the near term.

- Pipeline and comparative-trial risks: The outcome of the CagriSema comparative study, as well as regulatory developments related to Eli Lilly’s oral obesity drug, warrant close attention. Experts note that the Wegovy tablet contains many active ingredients, potentially resulting in higher manufacturing costs than competitors’. Another disadvantage is that the Wegovy tablet must be taken daily on an empty stomach, with no food or drink for 30 minutes afterward - while Lilly’s pending drug, orforglipron, can be taken at any time of day without such restrictions.

- Regulatory and pricing risks. U.S. drug-price negotiations took place last autumn, resulting in an agreement that is manageable for Novo Nordisk and largely priced in by investors. Nonetheless, similar initiatives may occur in the future. There is also a risk that unforeseen side effects could emerge, potentially limiting product uptake or triggering regulatory action.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more