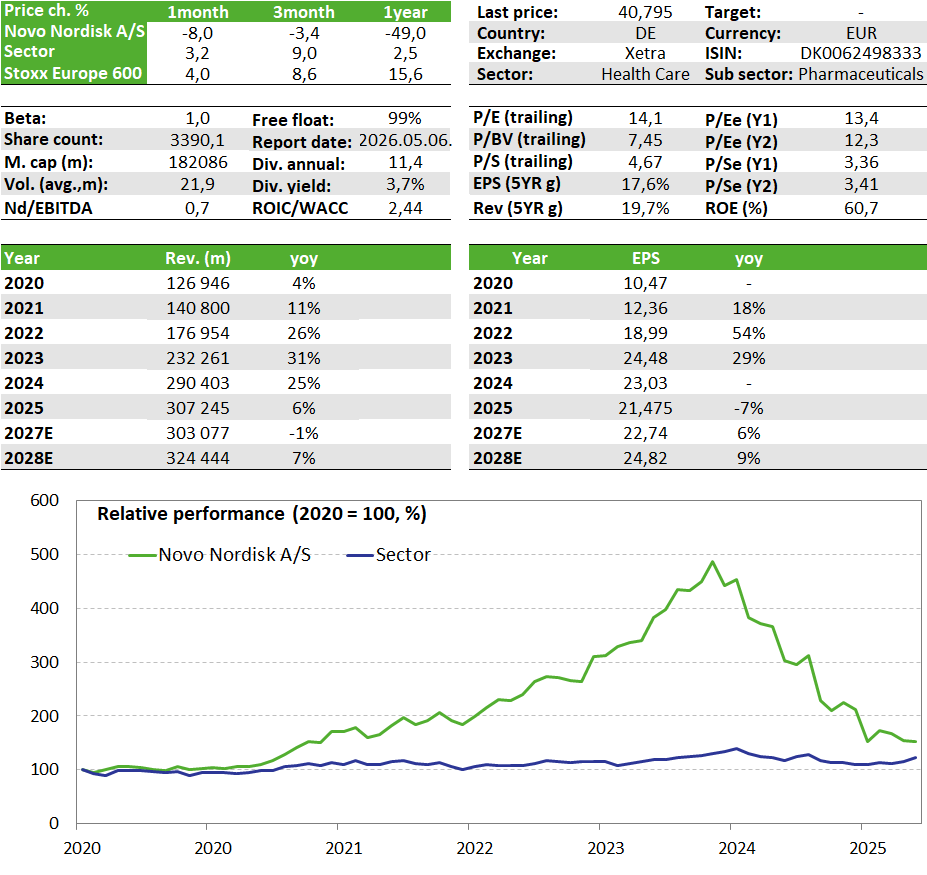

A cold shower from Novo Nordisk

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Novo Nordisk shocked the market with a surprisingly gloomy forecast: the company expects a much larger-than-expected decline in revenue and profits by 2026. Instead of the turnaround previously hoped for, a prolonged transition period is taking shape, as U.S. price cuts and fierce competition are putting such pressure on earnings that investors are being forced to reassess the situation even after last year’s profit warnings.

Quarterly Report

Novo Nordisk shocked investors by forecasting a significantly greater decline in revenue and profits for this year than expected. Prior to the report, analysts had expected a decline of around 2 percent on average, while the company now forecasts a drop of between 5 and 13 percent in both revenue and operating profit (excluding currency effects).

This suggests that the pressure on the U.S. market could be even greater than before. Although it became clear as early as last November just how much the company would have to cut the prices of its consumer medicines, it now appears that this will have a much greater impact on Novo Nordisk’s earnings.

Competition in the market is fierce, though this is nothing new, as Eli Lilly has long been the biggest competitor in this segment. In addition, there is also competition from a gray-market sector represented by certain compounding pharmacies. These are allowed to operate legally in the U.S., but their products are not approved by the Food and Drug Administration (FDA). When there was a shortage of these drugs between 2022 and 2024, they were allowed to produce alternative versions of Wegovy and Ozempic, which were significantly cheaper. And although these should no longer be officially manufactured as of last year, in specific cases where a patient requires a specific modification to an ingredient, it is still legal to produce them. However, this could lead to abusive practices, and the extent of their potential negative impact is unknown.

It should also be noted that while a price reduction has an immediate impact on revenue, lower prices can only gradually attract new patients to the market; in other words, the increase in volume takes time to materialize. It is highly likely that margins will be lower in this scenario than they were previously.

The Wegovy tablet, which the company began marketing in January, got off to a very strong start, reaching 170,000 patients in four weeks, but this is still not enough to offset the price pressure.

Although many may interpret management’s gloomy forecast as overly conservative—intended to make it easier to beat later on—many people thought the same thing last year following the profit warnings, yet that assumption ultimately proved to be incorrect.

We added Novo Nordisk to our Equity Top Pick List in January because we believed the company had already weathered the worst with last year’s two profit warnings and the announcement of price cuts in the U.S., and that a turnaround could begin under the new CEO. However, the recently released disappointing forecast changes this picture, as it appears that 2026—not last year—may be the year of transition, though even this is paved with many risks. The rise of the Wegovy tablet and positive news regarding other consumer formulas that are awaiting approval could still act as a catalyst for the stock price, but it will take a long time to recover from the current decline. For now, we are keeping Novo Nordisk on our Equity Top Pick List.

Investment thesis:

Following the organizational restructuring and layoffs launched last year, it will take a few more quarters for the changes to take effect. The reorganization process may take longer. Sales of the Wegovy tablet, launched this year, could ramp up quickly, providing a boost to growth. The higher-dose 7.2 mg injectable version of Wegovy is also under review for approval, which could further expand the number of patients the company can reach. Another important product is CagriSema, which combines two active ingredients, though the goal here is also weight loss and the treatment of type 2 diabetes. News regarding these products could have a significant impact on the stock price in the near future.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more