Noble: favorable results despite the war in Iran

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

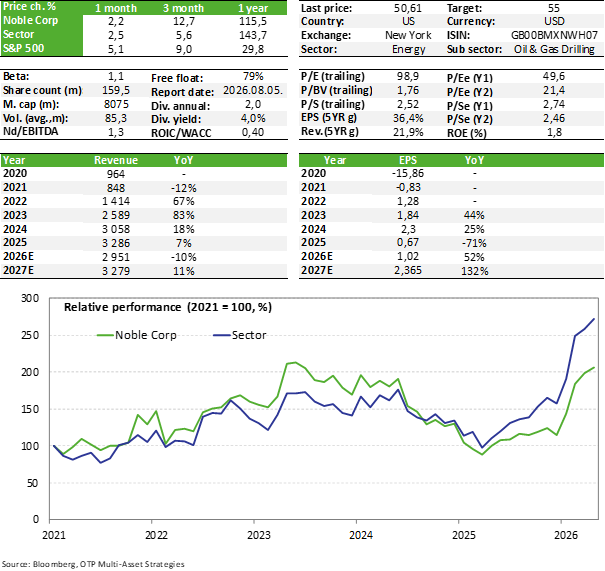

Noble’s first quarter was generally positive, with the company outperforming analyst expectations in what could be described as a relatively weak market environment. Free cash flow remained strong, so maintaining dividend payments is not an issue, and management has also reaffirmed its 2026 targets. However, a positive market turnaround is not expected until next year. The war in Iran primarily has a negative impact on the shallow-water jackup market as Middle East demand is significant in this segment, which may decline temporarily. We note, however, that this does not have a significant impact on Noble’s outlook, as most of the company's fleet is suited for deepwater drilling. The stock is no longer cheap, but for now we are keeping it on our Equity Top Pick List, as there may still be some room for the share price to rise.

Quarterly report

Noble released its Q1 results on Sunday, which is somewhat unusual, but the results nonetheless exceeded analysts’ expectations in terms of both revenue and earnings. Revenue was thus more than 7% higher than expected, but down 10% year-over-year. Earnings per share was $0.26 (vs. $0.21 FactSet estimate), representing a year-over-year stagnation.

Despite the decline in revenue, operating cash flow remained stable at $273 million in the first quarter, while capital expenditures were around $104 million. The company’s free cash flow thus remains significantly positive (approximately $170 million in Q1). This more than covers Noble’s dividend payments, which currently amount to $80 million per quarter, or $0.50 per share (an annualized dividend yield of approximately 3.9%).

In light of these results, management maintains its 2026 guidance, which projects revenue of $2.8–3.0 billion and EBITDA of $940 million to $1.02 billion. The only slight downside is that capital expenditures may be moderately higher by approximately $25 million, but this is not a significant amount. Management continues to expect a significant positive market turnaround in 2027 (compared to the temporarily weaker year of 2026).

At the end of March, the company’s gross debt stood at $1.9 billion, while its net debt was $1.3 billion. This is not considered high; the net debt-to-EBITDA ratio currently stands at around 1.3.

Fleet utilization declined moderately on an annual basis, standing at 69% (vs. 74% in Q1 of last year). Structurally, utilization of deepwater rigs declined more sharply (65% vs. 74%), while the shallow-water jackup segment performed better (78% vs. 74%). However, average daily rental rates rose year-over-year in both segments, which is a positive development. At the end of the quarter, the company's backlog was exceptionally high, totaling $7.5 billion.

It should be noted that during the quarter, the company also received $206 million in cash from the sale of assets (this amount is not included in the free cash flow calculation above due to its one-off nature). This represents the cash portion of a previously announced transaction in which Noble sold five shallow-water jackup drilling rigs to Borr Drilling.

The impacts of the Iran war

The U.S.-Iran conflict is also affecting the offshore oil drilling market, as Middle Eastern countries account for a significant portion of global demand for shallow-water jackup drilling rigs, particularly Saudi Arabia. Naturally, the conflict is having a negative impact on demand in this market segment in the short term. However, this has less of an impact on Noble’s outlook, as the company’s fleet consists predominantly of deepwater drilling rigs (25 out of a total fleet of 31 units). In the longer term, the conflict could even have a positive impact on demand for deepwater drilling rigs, as some investments may shift from shallow-water areas in the Middle East to regions requiring deepwater drilling (e.g., Brazil, Namibia, etc.).

Valuation

The year 2026 may still be relatively weak for the offshore oil drilling sector, but there is broad industry consensus that demand could grow significantly starting next year. This is worth considering in relation to Noble’s valuation, which is already high based on the expected 2026 EPS (approx. 49x P/E). However, based on the projected 2027 EPS, the P/E ratio is 21x, while for 2028 it is 14.7x. If we examine the valuation picture on an EV/EBITDA basis, it looks much better: based on the estimated EBITDA for 2026, this is 10x, while for 2027 it is 8x.

Overall, Noble performed well in the first quarter, and the company generated significant free cash flow even in a relatively weak market environment, so the dividend payout appears sustainable (and may even increase if the external environment improves over time in line with expectations). However, the valuation can no longer be considered low, though there may still be some room for the share price to rise further, so we are raising our target price to $55. For now, we are keeping the company’s shares on our Equity Top Pick List, but partial profit realization might be adequate at these levels.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more