Noble: This year may be weaker, but signs of a turnaround are already visible

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

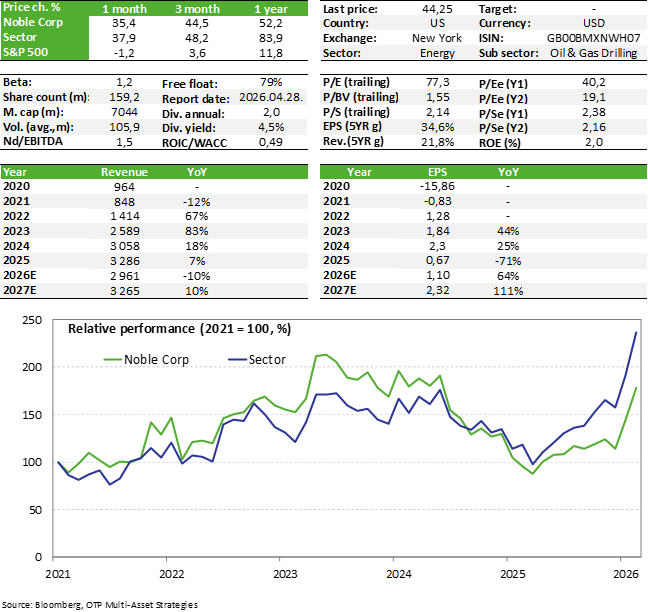

Noble, which is involved in offshore oil drilling, published its Q4 earnings report a few days ago, which shows a mixed picture. The bottom line fell short of analysts' expectations, the whole of 2025 was relatively weak and this year is also not expected to be particularly strong. There were also positives in the report, as free cash flow remains strong and more than covers dividend payments, which appears to be sustainable. However, the really good news is that the backlog for 2027 is already at a similar level to this year's, which points to a revival in demand, so next year's results could be better. For now we are keeping the shares on our Equity Top Pick List, as we continue to see long-term potential in the offshore oil drilling sector.

Quarterly earnings

Noble published its latest quarterly results after the market closed on February 11, with mixed results. Earnings per share of $0.09 fell short of the analyst consensus of $0.16, while revenue exceeded expectations.

Looking at the whole of 2025, Noble's performance was relatively weak, with revenue up 6% but operating profit down 31% and earnings per share down 71% (adjusted EPS).

In terms of operating segments, it is evident that, in a relatively weaker business environment, the utilization rate of the company's fleet declined, averaging 62% in Q4 of last year compared to 73% in Q4 2024. Here, demand for both jackups and floaters declined on an annual basis. However, the average daily rental rate for drilling platforms increased on a year-on-year basis (USD 344,000, +6.5%), but a decline can also be seen on a quarterly basis (-4%). On a slightly positive note, however, rental rates for jackups are higher on both an annual and quarterly basis.

Despite the above negatives, there are also several positives to highlight: full-year EBITDA was $1.1 billion, which is 4% higher year-on-year and within the target range previously set by management ($1.1-1.125 billion). In addition, the company's cash generation remained particularly strong (despite weaker results): operating cash flow was $952 million (+45% year-on-year), while free cash flow was $454 million (corresponding to an FCF yield of approximately 6.6%). These are quite good figures in a relatively depressed oil market environment.

In addition to strong cash generation, Noble has maintained its quarterly dividend of $0.5 per share (approximately 4.6% annualized dividend yield). This represents an annual expense of approximately $320 million, which appears sustainable given the company's free cash flow of more than $450 million.

Outlook

The company also published its guidance for 2026: revenue is expected to be between $2.8 billion and $3 billion (-12% year-on-year at midpoint), while EBITDA is expected to be in the range of $940 million to $1.02 billion (-11% year-on-year at midpoint). Capital expenditure is expected to be $590-640 million this year, which is moderately higher than the $520 million in 2025. These are not particularly strong figures, but they come as no great surprise, as industry players have already indicated that 2026 will not be a strong year.

However, 2027 is expected to be a better year, as evidenced by the size of the backlog, which already totals $7.5 billion. The portion of the backlog for this year is $2.3 billion, but the value of next year's bookings already exceeds $2.3 billion, and there are also orders worth $1.7 billion for 2028. Of course, if the oil market environment weakens, it is conceivable that some drilling projects will be delayed.

Valuation and debts

Noble's net debt at the end of the year was $1.5 billion, which corresponds to a net debt/EBITDA ratio of approximately 1.5. This is not considered high, so there are no debt-related problems.

However, the company's valuation can be considered moderately high, with a P/E ratio of 40 times based on 2026 EPS and 19 times based on 2027 EPS. The picture is more favorable based on the EV/EBITDA ratio, which is 8.4 times for 2026 and 6.9 times for 2027. In the case of Noble, it is worth noting that the company operates in a highly cyclical industry, so the values of the multiples may fluctuate significantly over time (especially in terms of EPS).

Overall, Noble's valuation can no longer be considered low, and in recent days the share price has exceeded our previous target price of $40. For the time being, we are not setting a new, higher target price due to the weaker business environment, but we continue to see potential in the offshore oil drilling sector in the longer term, which is supported by Noble's high backlog for 2027, so we are keeping the shares on our Equity Top Pick List for now.

It is also interesting to note that very recently, further consolidation took place in the offshore oil drilling sector, as Transocean acquired Valaris in a $5.8 billion transaction (all-stock deal). Under the terms of the deal, Valaris shareholders will receive 15.235 Transocean shares for each share they hold. This represented a premium of approximately 32% over Valaris' closing price prior to the announcement of the transaction and corresponded to an EV/EBITDA multiple of approximately 10 times (based on EV of $6.2 billion) on 2025 EBITDA, and a multiple of 12 times using estimated 2026 EBITDA. In Noble's case (using a similar multiple), this would imply a "fair value" of around $58 per share even based on the weaker EBITDA for 2026, but more than $60 based on the 2025 figure. The question obviously arises as to whether Transocean paid too much for the Valaris acquisition, but this will obviously depend on market conditions. In any case, based on this, Noble still does not appear to be expensive.

Investment story

The offshore drilling sector is a relatively small and tight market with few players, so supply is limited. The sector performed particularly poorly in the second half of the 2010s due to falling oil prices, the boom in US shale oil production, and lower oil industry investments, forcing several players to file for bankruptcy.

However, following the COVID-19 pandemic, oil prices rose significantly, global demand rebounded, and with the growth rate of US shale oil production slowing down, many players turned back to offshore production. This is good news for offshore service companies, where daily drilling platform rental rates are rising steadily, capacity utilization is increasing (albeit volatile), competition is limited, barriers to entry are high, and the uncertainty surrounding the future of the oil industry makes it unlikely that new players will enter the market.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more