Netflix: Strategic Clarity Unlocks Earnings Momentum

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

For Netflix, walking away from the acquisition of Warner Bros. ultimately proved to be a liberating decision. By abandoning the deal, the company avoided taking on a massive debt burden and eliminated the execution risks associated with a transformational transaction. As a result, Netflix can once again refocus on its core business: growth and monetization. The market is increasingly rewarding this strategic clarity. The share price has staged a material rebound, earnings visibility has improved, and the world’s largest streaming platform continues to build new revenue streams. With Netflix reporting quarterly results on Thursday, we are adding the stock to our Equity Top Pick List already ahead of the announcement.

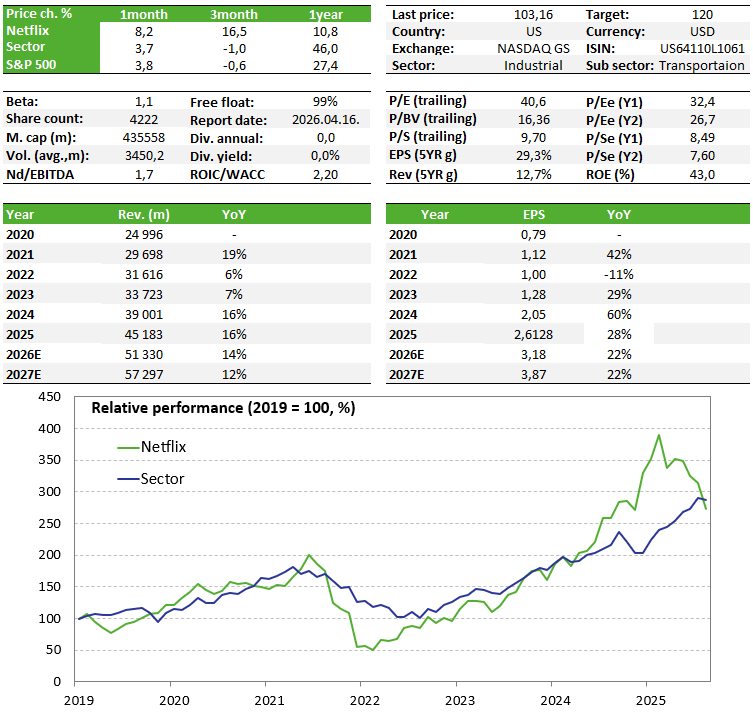

Company Overview

Netflix hardly requires an introduction. It is the world’s leading streaming service and is present in most households globally. The company operates on a global scale (with the notable exceptions of China and Russia) and produces films and series, while also offering live events and sports content. Access to the platform is based on a monthly subscription model. In addition to licensed content, Netflix has built a vast portfolio of original productions. Importantly, approximately 45% of total viewing hours are generated by Netflix-owned content, which plays a critical role in subscriber retention.

Investment case

Our investment case is built on Netflix’s decision not to proceed with the Warner Bros. acquisition. Had the transaction gone ahead, Netflix would have been forced to assume a substantial debt load, resulting in elevated interest costs for years and persistent pressure on margins. At the same time, the realization of potential synergies would have been far from guaranteed.

The media sector offers numerous cautionary examples over the past 20–25 years where large-scale acquisitions failed to deliver on expectations. By stepping away from the deal, Netflix avoided many of these structural risks.

With the transaction off the table, management can fully refocus on the company’s core operations — an area where Netflix has historically executed well. The stock had suffered a sharp sell-off, exacerbated by the bidding war with Paramount for Warner Bros. However, since abandoning the acquisition, Netflix shares have rebounded meaningfully and have continued to perform well even amid recent market volatility.

Netflix remains the largest streaming platform globally, with approximately 325 million subscribers. Disney follows with close to 200 million subscribers including Hulu. Paramount and HBO Max together may also exceed 200 million subscribers, although the overlap between the two user bases is uncertain.

Overall, Netflix remains the clear leader in terms of subscriber scale. However, when it comes to total screen time, Netflix now trails YouTube. In many respects, Netflix is no longer primarily competing with Disney or HBO—those rivals have largely been surpassed. Instead, the true competitive benchmark is increasingly YouTube, despite the fundamentally different business models.

Estimates for Netflix’s total addressable market (excluding China and Russia) range between 700 million and 1 billion households, though the realistically accessible portion is naturally smaller. This suggests that there remains room for growth, albeit increasingly constrained in developed regions such as North America and Europe. As a result, the strategic emphasis since the early 2020s has shifted from subscriber growth to monetization. This has driven significant margin expansion. Key initiatives include: cracking down on password sharing; introducing an ad-supported subscription tier and implementing regular price increases.

To cater to its vast global audience, Netflix has also diversified its content offering beyond films and series. This includes sports and live events such as NFL games, baseball, wrestling, boxing, and unique live broadcasts (e.g. the recent live stream of the Taipei 101 tower climb). The company is also expanding into podcasts this year, directly challenging YouTube and Spotify.

Financial Outlook and Valuation

Consensus expectations for 2026 point to 13–14% revenue growth, while net income is projected to increase at an even faster pace (+19.8%). Advertising revenue is expected to double this year from approximately USD 1.5bn, becoming a meaningful new growth engine. These figures represent a material improvement compared to earlier expectations, when the Warner acquisition was still considered likely and profit projections were significantly lower.

In addition, Netflix received a USD 2.8bn break-up fee from Paramount following the abandoned transaction. Free from balance sheet pressure, the company now has greater flexibility to invest in content development. Netflix has budgeted USD 20bn for content spending this year, up 10% year-on-year, while still operating with expanding margins—driven primarily by price increases.

In March, Netflix announced widely anticipated price increases in the US—earlier than the market had expected. The ad-supported tier increased by USD 1 to USD 8.99, while the Standard and Premium plans rose by USD 2 to USD 19.99 and USD 26.99, respectively. The price changes apply immediately to new subscribers and will be rolled out to existing customers over the coming weeks. Historically, US price increases have been followed by similar adjustments internationally with a slight lag. Importantly, past experience suggests that these increases should not trigger meaningful subscriber churn. Even after the hike, Netflix’s pricing remains competitive: the ad-supported tier is still cheaper than competitors such as HBO Max (USD 10.99) and Disney+ (USD 11.99), while ad-free plans remain broadly in line.

With the Warner deal pending, Netflix had suspended share buybacks. These can now resume. Despite high content spending, the company generates substantial free cash flow (2026E: USD 11.8bn, +25%) and maintains a modest debt profile.

Netflix currently trades at a forward P/E of ~32x, supported by strong earnings growth and high profitability. This represents a meaningful moderation from the ~44x multiple seen last summer.

We are adding Netflix to our Equity Top Pick List, supported by improved earnings quality, strong cash generation, renewed strategic focus, and sustained pricing power.

Key risks

- Content spending risk: USD 20bn in annual content investment is substantial and could rise further, especially with increased exposure to sports rights. If revenue growth disappoints, content costs may weigh on margins.

- Market saturation: With a large installed base, explosive growth is unlikely. Expansion opportunities remain primarily in emerging markets, where pricing power is limited.

- Competitive intensity: Switching costs are low in streaming. Strong execution by competitors could result in subscriber losses, although historical evidence suggests Netflix remains the platform to beat.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more