Netflix: Profit-Taking Does Not Undermine the Investment Case

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

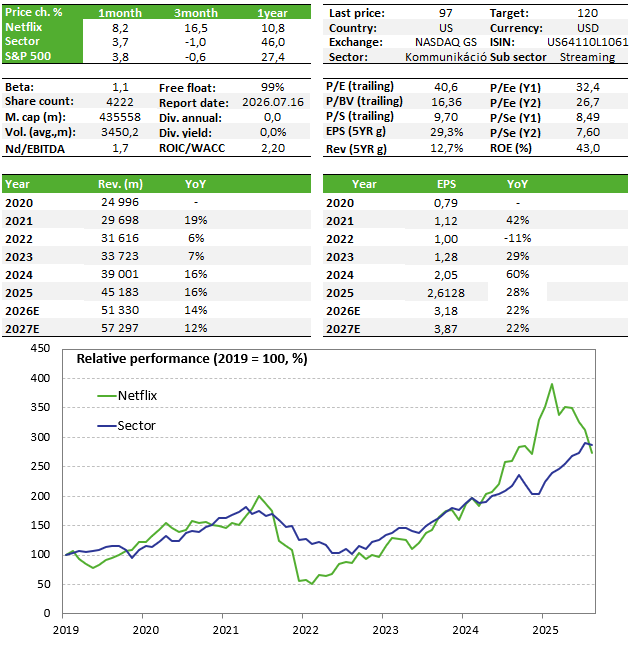

Netflix shares may open sharply lower on Friday following the earnings release, as investors appear to be taking profits after the stock’s strong rally. However, in our view, the current correction does not weaken the underlying investment case. The weaker-than-expected second-quarter profit outlook is primarily driven by timing effects, while management reaffirmed its full-year growth expectations and the advertising business continues to expand rapidly. As such, after the strong rally seen since the February lows, we view the pullback more as a healthy correction than a trend reversal.

Earnings report

Netflix shares are set to begin Friday’s trading session with a significant decline, after the quarterly earnings report triggered profit-taking among investors. This comes after the share price had already risen by 40% from its February lows. We added Netflix to our Equity Top Pick List list earlier this week, and we continue to believe that the company remains a fundamentally attractive investment opportunity, particularly in light of the current correction.

The sharp share price decline was triggered by the company guiding for lower-than-expected net income in the second quarter. The main reason is that Netflix’s content spending will peak in Q2 due to the timing of content releases. At the same time, spending is expected to decline in the second half of the year.

Apart from this, first-quarter revenue came in ahead of expectations, as did profit. However, the latter is more difficult to compare due to the one-off USD 2.8 billion payment received from Paramount after Netflix walked away from the Warner acquisition. Management reaffirmed its full-year guidance for revenue growth of 12–14% and an operating margin of 31.5%. At the group level, the ad-supported tier continues to expand significantly, and management reiterated that advertising revenue could reach USD 3 billion this year, which would imply a doubling on an annual basis.

Selling pressure may also have been intensified by the announcement that founder Reed Hastings will not renew his board membership when it expires in June. Hastings has not served as CEO since 2023 and no longer has an active operational role at the company, but the market nevertheless reacted negatively to the news. Regarding the decision to walk away from the Warner transaction, management commented that the deal would only have created value for Netflix if the company could have been acquired at the right price, which ultimately did not materialize.

The Asia region delivered a strong performance, supported by the streaming of the World Baseball Classic Japan. The event was streamed by more than 31 million viewers globally and generated the largest single-day subscriber additions in Japan. According to press reports, Netflix is also in talks with the NFL over potentially broadcasting not only Christmas games, but a broader slate of matches as well.

Investment case

- The most important positive development is that Netflix did not proceed with the Warner acquisition. As a result, the company avoided taking on significant additional debt, higher interest expenses, and the integration and synergy risks that have historically often destroyed shareholder value in the media sector. Consequently, Netflix’s balance sheet has remained cleaner, while management’s focus has shifted back to the core business.

- Netflix remains the leading player in the global streaming market, with 325 million subscribers, giving it a clear advantage over its competitors. At the same time, real competition is no longer limited to traditional streaming players such as Disney, HBO/Paramount, but increasingly includes YouTube as well, as the battle is now also for screen time. Meanwhile, the remaining room for subscriber growth is increasingly concentrated in emerging markets.

- The centre of gravity of the growth story has shifted from subscriber growth toward monetization, which is particularly supportive for profitability. The crackdown on password sharing, the launch of the ad-supported tier, and price increases all serve to drive revenue growth. This is further supported by content diversification — including live sports events and a move into podcasts — which could create new sources of viewership and revenue.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more