Hungary: Unchanged base rate of 6.25%, but a shift in tone. The path could be paved for an interest rate cut by June

Related content

Palantir Delivers Another Blowout Quarter

Palantir reported an outstanding quarter, with accelerating growth, expanding margins, and a record contract backlog. Management raised its full-year guidance, continuing its recent pattern of upward revisions. The shares are expected to open Tuesday’s session around 15% higher. Palantir remains on our Equity Top Picks List.

AWS Puts Amazon Back in High Gear

Amazon's stock price surged following the release of a better-than-expected preliminary report. Investors primarily praised AWS's spectacularly accelerating growth and outstanding profitability, and not even the announcement of a capex plan increased to $220 billion could dampen the mood.

As expected, the MNB’s Monetary Council kept the base rate unchanged at 6.25% at its May meeting. The MNB’s message remained cautious, but it opened the door for interest rate cut if the current favourable trends persist.

The MNB's key messages:

· High global energy and commodity prices, as well as rising long-term yields in developed markets, call for caution.

· The Monetary Council is monitoring the monetary policies of major global and regional central banks.

· The stronger forint is moderating the pace of price increases, but the sustainability of these developments must be confirmed.

· The risk premium on domestic assets remains below pre-election levels.

· The improvement in risk appetite for domestic assets is supported by prospects for drawing EU funds and joining the euro area.

· The sustainability of these positive trends expands the room for manoeuvre in monetary policy.

· A key issue is what amendments to this year’s budget the government will be proposed, and how next year’s budget will look like.

· The Monetary Council discussed two scenarios at its May meeting: holding rates and cutting rates. The decision was not unanimous.

Market reactions

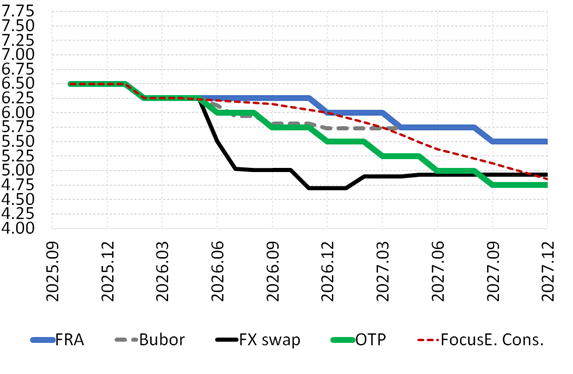

· The decision was in line with expectations, but the dovish tone of the press release had it’s effect on pricing. Regarding the HUF, it appreciated in the morning, but weakened slightly, by 0.2% in the afternoon. The effects were stronger on the fixed income market, where the FRA, the bond and the IRS curve shifted down by 10-15 bps after the publication of the press release. The bond curve fell parallel below 5.5%. Market pricing reflects three 25 bps rate cuts by the end of 2026 and another one in 2027.

Before the decision: No rate change was foreseen

· There were many sigs, that after the low inflation figures in early 2026 the appreciation of HUF might be too fast for the MNB. FX reserves rose fast in the first months of 2026. Three weeks ago, Deputy Governor Zoltán Kurali suggested, that the strong HUF might bring back rate cuts to the table. Furthermore, at its FX swap tender on 13 May, the MNB cut the available rate to the lower band of the interest rate target band, sending a clear signal to FX investors.

· Nevertheless, it was clear that Monetary Council would not begin cutting interest rates before the publication of the new Inflation Report in June. Although the inflation outlook has improved significantly in recent months—with average inflation for this year likely to be around 2.5%—the issue of the Strait of Hormuz remains unresolved. The inflationary impact of the oil-crisis is non-linear, and the oil market is currently drifting toward a negative scenario, which may lead the MNB to adopt a wait-and-see approach. Market pricing had already priced in an interest rate cut for June, while we had expected the first rate cut in September.

Our assessment: Given that the MNB remained cautious but emphasized the importance of data and economic policy decisions to be released by June, we expect that, if the situation in the Strait of Hormuz is resolved, the rate cutting cycle will begin in June, with the publication of the new Inflation Report. in case of a prolonged oil-crisis, rate cuts could be delayed. However If the new government will successfully unblock EU funds and the mid-term fiscal deficit trajectory promised for October will increase the credibility of an early EUR adoption, an aggressive rate cutting cycle could come in late 2026 and 2027.

· After the low inflation figures in Q1 inflation in April was 0.4 percentage points lower than the MNB had forecast in its latest inflation report. This gap could widen even further in May, as the protected fuel price will not be phased out this month. Given all this, as well as the much stronger exchange rate, we expect the central bank to significantly lower its inflation forecast in the next inflation report in June. If there is no drastic deterioration in Hungary’s risk assessment by the June meeting, the Monetary Council may decide, based on a three-month period, that there has been a sustained improvement in the risk assessment. Nevertheless, the Iranian war situation remains a significant risk, as the inflationary effects of the war are not linear.

· The Monetary Council remained cautious in its assessment of the current positive trends and emphasized the uncertainty surrounding their sustainability. At the same time, it repeatedly highlighted the importance of the data and economic policy decisions received by the time of the June interest rate decision meeting, as well as the situation assessment of the June Inflation Report.

· Based on the above, we expect that if a satisfactory solution to the issue of the Strait of Hormuz is reached by the June meeting, the rate cut cycle could begin. However, if the strait remains closed during this period, raising oil prices and inflation pressures could make the Council to keep rates at their current level for a while. But unblocking EU funds soon and a reasonable fiscal plan with a shrinking deficit in the coming years paving the way for euro adoption could result in a fast rate cutting cycle in 2026/27.

Expectations for the base rate (%)

Sources: Bloomberg, OTP Research, Focus Economics, MNB

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more