Hungary: The MNB kept the base rate on hold, as expected; it struck more hawkish tone. We expect rates to remain on hold for a while

Related content

Meta: Trading Idea closing

In early July we sent a Trading Idea related to Meta shares, as we believed that several announcements had been made that could positively influence investor sentiment toward the company in the short-term. This worked well for a short time, but then the stock fell along with the broader technology sector, partly due to the launch of a new Chinese AI model, the Kimi K3. The company published its disappointing earnings report on Wednesday after the market close amid this weaker market sentiment, causing the stock price to reach our previously set stop-loss level during yesterday’s trading. Accordingly, we are closing our Trading Idea.

India would take a step forward and become a developed country

The conflict in Iran and the effects of the El Nino weather phenomenon could cast a shadow over the Indian economy this year, but there is reason to be optimistic in the longer term. India remains one of the world’s fastest-growing economies, but it does not intend to stop there; the country has set an ambitious goal to transform itself into a developed nation by 2047, the centennial of its independence. In this part of our analysis on India, we examined what is currently happening in the Indian economy, as well as what the future may hold for India.

As expected, the MNB’s Monetary Council kept the base rate unchanged at 6.25% at its March meeting. The MNB has essentially struck a more hawkish tone by expressing that all options were on the table.

The MNB's key messages:

· Geopolitical risks are very high, the effects of the war in Iran carry global inflationary risks. At the same time, the fundamentals of the Hungarian economy are considerably stronger than at the onset of the 2022 energy crisis.

· The MNB increased its forecasts on inflation (for both 2026 and 2027) and cut that on growth (for 2026) as a consequence of the sharp rise in energy prices following the war in Iran.

- The inflation forecast for this year was revised up to 3.8% from 3.2%, and for next year to 3.7% from 3.3%. The 2028 forecast remains at 3%. Risks around inflation are tilted to the upside.

- GDP may expand by 1.7% in 2026, 3.0% in 2027, and 2.9% in 2028 (compared with the December forecasts of +2.4%, +3.1%, and +2.7%, respectively).

- Current inflation projections are surrounded by upside risks, while growth projections face downside risks.

· The inflation target can be achieved in a sustainable manner in the second half of 2027. This year, the economic outlook will continue to strengthen; however, the geopolitical events of recent weeks are slowing the recovery.

· A cautious and patient monetary policy approach is required. Maintaining tight monetary conditions remains justified. Preserving stability in the FX market is key to anchoring inflation expectations and achieving the inflation target. Given the high real interest rate, the MNB currently has room for manoeuvre in the period ahead.

· Household inflation expectations have moderated — both those referring to current inflation perceptions and to inflation expected one year ahead. Further reducing inflation expectations remains essential, to which the MNB contributes by maintaining a positive real interest rate.

· On 10 March, the Monetary Council decided to ensure the availability of substantial FX liquidity that may be required for energy imports. This remains an open option with no set expiry date.

The central bank does not see country-specific factors behind the movements observed in government bond yields over the past three weeks.

Market reactions

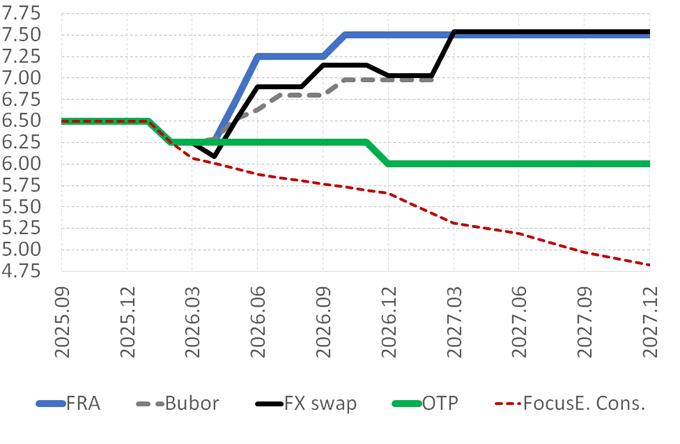

· The decision was in line with expectations, and there was no observable market reaction following the publication of the press release or during the press conference. Later in the afternoon the HUF depreciated, but most likely this had nothing to do with the MNB’s decision as the HUF weakened hand in hand with other CEE currencies and some rise in oil prices. Regarding fixed income effects, FRAs, swap and bonds yields have not changed substantially, especially taking into account the drastic increase in volatility. The market still prices 100 bps rise in the base rate in the following few months.

Before the decision: No rate change was foreseen

·When assessing the February CPI figures, it seemed likely that interest rate cuts would follow in March. But then the war in Iran made energy prices skyrocket, which led to another energy price shock – this is already certainty, only its extent, duration, its inflation-increasing and growth-reducing effects are yet to be seen. The HUF’s rapid depreciation sent the EUR/HUF to 390-400, up from 375. Continuing a previous rally, Hungary’s bond yields surged by more than 100 basis points, interest rate cut expectations were gone with the wind.

· Before the MNB's March decision, prices reflected that the market expects at least 75 basis points higher interest rates in a few months’ time – not only from Hungary’s MNB, but also from the ECB, the Czech National Bank, and the National Bank of Poland.

. Given that Hungary’s external environment suddenly became adverse, we thought that interest rates will remain flat. So did most analysts, although some players anticipated an interest rate reduction.

Our assessment: Given current energy prices, we expect the MNB to keep the base rate unchanged for a while even if risks are tilted to the upside. We think that the market has run ahead with pricing rate hikes of 100-125 bps.

· Based on the February inflation data, we would have lowered our 2026 inflation forecast of 2.9% by 0.3 percentage points. However, taking into account the current energy price developments, our forecast has risen back to 2.9%. Considering the scale of the oil supply shock – the largest on record -, the wide range of affected inputs and industries, inflation, and the uncertainty around the scale and the duration of the crisis, inflation risks are tilted to the upside. It is important to emphasize that energy prices have the strongest and fastest impact on inflation through fuel and natural gas prices. In Hungary, household energy prices are regulated, and we assumed that the government would not raise them. Furthermore, the Hungarian government has also capped fuel prices. As a result, the effects of rising energy prices are reflected in inflation in a much less direct and slower manner (rising transport costs, corporate energy prices, etc.).

· Based on the MNB’s press conference—which had an overall hawkish tone—and considering that the Hungarian economy faced the recent energy price shock with stronger fundamentals than in 2022, we do not expect an interest rate hike in the coming months. However, as we are sceptical about the drastic rate cuts before the war, now we have doubts about the front-loaded drastic tightening priced in now. It is not an impossible outcome of course, but with the current energy prices we would expect the MNB to keep the base rate at the current level for a while. We would still pencil in one more rate cut at the end of this year in case the dust settles fast, but this is uncertain of course.

· But in case of an escalation, when oil prices go ballistic for an endured period, the MNB may implement the rate hikes in the magnitude that is currently priced into the curve

Expectations for the base rate (%)

Sources: Bloomberg, OTP Research, Focus Economics, MNB

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more