Hungary: We lower our year-end base rate forecast by 50 bps to 5% after the MNB cut

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

At its June meeting, as expected, the MNB’s Monetary Council cut the base rate by 25 basis points to 6%. However, the Bank’s communication turned markedly dovish, pointing to further significant rate cuts ahead.

The MNB's key messages:

· The Monetary Council is committed to achieving the 3 percent inflation target in a sustainable manner.

· The inflation path in the June forecast significantly shifted downwards compared to the one in the March forecast. The baseline scenario is surrounded by balanced inflation risks.

· In the baseline, the inflation is expected at 1.8% and 2.3% in 2026 and 2027 (before: 3.8% and 3.7%), while will revert to the 3% target by 2028. The GDP growth is expected at 2% and 3% in 2026 and 2027 (before 1.7% and 3%).

· With the easing of geopolitical tensions, the global risk environment has become more favourable and lower risk premiums on domestic assets remained. These factors significantly increase the room for monetary policy to manoeuvre.

· Looking ahead, if favourable developments persist, the Council – while maintaining a positive real interest rate – sees room for further interest rate cuts throughout the summer. The MPC will decide on the continuation of the interest rate cuts based on the September Inflation Report.

Market reactions:

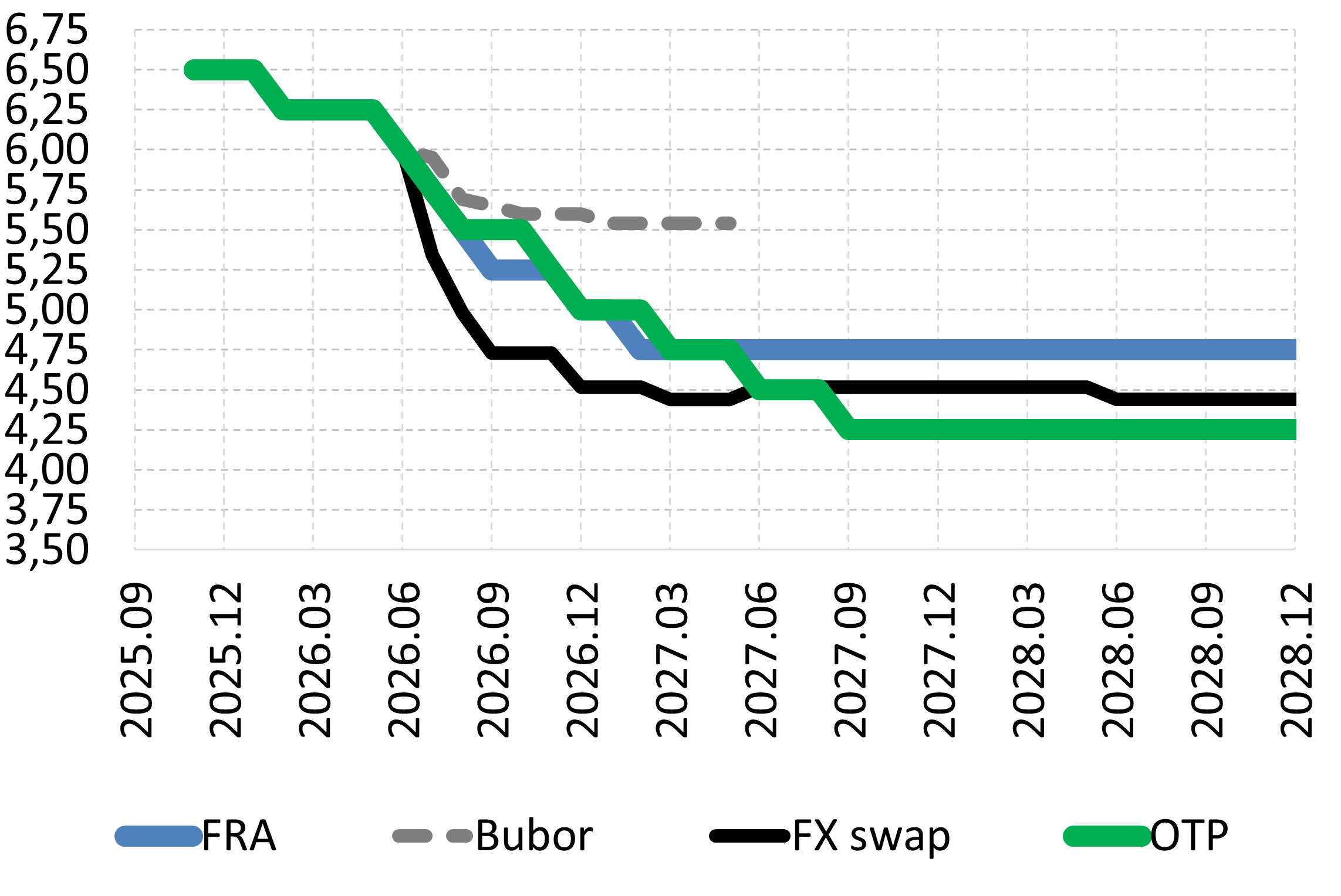

· The decision was in line with expectations, but the dovish tone of the press release and the press conference shifted down the whole FRA curve by around 10-15 bps. The HUF depreciated by around 0.3% after the press release. The FRA-s now price the end-2026 baserate around 5%, down by 15 bps. Therefore, market pricing reflects four 25 bps rate cuts by the end of 2026 and another one in 2027.

Before the decision: the cut was widely expected

· The current stronger exchange rate has contributed significantly to breaking the previously very persistent inflation trends, and risks associated with the 11% minimum wage increase and the substantial pre-election fiscal demand stimulus did not ultimately materialize. As a result, inflation developments have been very favorable since the beginning of the year, and the latest data for May also came in significantly below market analysts’ expectations (1.8% versus the expected 2.2–2.3%).

· With the sharp decline in international oil prices, the last obstacle to rate cuts has also been removed, so the question was rather only the magnitude of the cut. In total four cuts were priced in by the end of the year, and an additional step in 2027, although this latter path may still be significantly influenced by the medium-term fiscal trajectory promised for October, which could validate the strong pre-emptive investor confidence related to a rapid euro adoption.

Our assessment: Given the MNB’s very low inflation forecast for next year and its guidance of a series of rate cuts till September, we revise our end-2026 base rate forecast to 5%. The outlook for rates next year remains more uncertain and will largely depend on the government’s medium-term fiscal trajectory and the details of its euro adoption strategy.

· The new inflation forecast points to 2.3% for 2027, well below the 3% target. While there is considerable uncertainty over whether the recent low inflation readings are temporary or reflect a more permanent shift in price-setting behaviour, the subdued outlook for next year suggests that the MNB believes inflation persistence has been broken and that the target can be achieved alongside significant monetary easing. This is also reflected at the end of the press release in the very open communication on further rate cuts during the summer: “…Looking ahead, if favourable developments persist, the Council – while maintaining a positive real interest rate – sees room for further interest rate cuts throughout the summer, with a decision on their continuation to be made based on the September Inflation Report….”, This latter statement was also explicitly mentioned by Governor Varga at the press conference.

· All the above factors suggest that by August the base rate could decline to 5.5%. However, given the very low inflation outlook of the central bank, we think base rate cuts will continue, probably to 5% by the end of the year. Further cuts in 2027, will depend on how the market assess fiscal announcements during the Autumn and also whether the inflation target will eventually lowered on the path to euro entry.

Nevertheless, given the uncertain global environment and the potential for rising US interest rates, risks to our base rate forecast are tilted to the upside.

Expectations for the base rate (%)

Sources: Bloomberg, OTP Research, Focus Economics, MNB

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more