Hungary: The MNB kept the base rate at 6.5%; corporate repricing at the start of 2026 will be key to the path of interest rates

Related content

FX - Technical Analysis

The dollar has remained strong in recent days, so the dollar’s strength has continued to dominate its major currency pairs; there are no signs of a reversal in this regard yet. As for the forint, a minor correction began three weeks ago, but neither its magnitude nor its intensity was sufficient to suggest a prolonged depreciation of the forint. The USD/JPY exchange rate broke through the 162.5 level, confirming the continuation of the uptrend. Meanwhile, the EUR/CHF exchange rate also surpassed the nearest resistance zone, keeping the pair on an upward trend. Due to vacation, there will be no analysis next week. The next article will be published on August 12, 2026.

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

As expected, the MNB’s Monetary Council left the base rate at 6.5% at its January meeting. The forward guidance remained unchanged compared to December, but the tone of the press conference was somewhat more hawkish. The focus will be on repricing at the start of the year.

The MNB's key messages:

· Corporate repricing at the beginning of the year will be a key determinant of the inflation outlook, and the February data will be the first ones to reflect its impact.

· Maintaining tight monetary conditions remains justified, along with a cautious and patient monetary policy approach.

· The MNB’s forward guidance has not changed: decisions will continue to be made carefully, in a data-driven manner, on a meeting-by-meeting basis.

· Inflation remained within the MNB’s tolerance band for the second consecutive month in December and may fall below the target at the beginning of this year, but some figures of underlying inflation have even increased.

· Household inflation expectations remained above the inflation target, while corporate expectations were somewhat more moderate.

· The appreciation of the forint is increasingly being reflected in procurement prices.

· The central bank has no exchange rate target; it is interested in reducing the volatility of the exchange rate.

Market reactions:

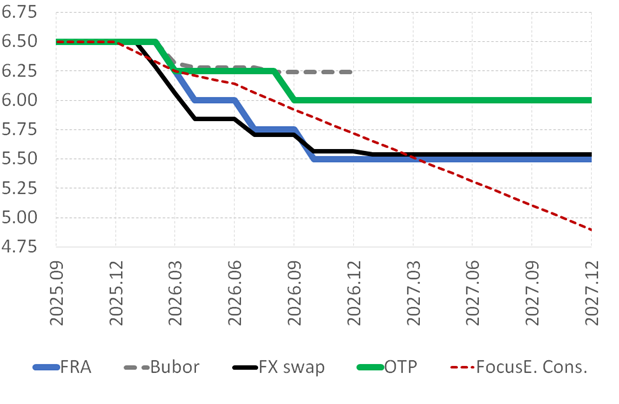

· After the publication of the press release and the conference, financial markets embraced the decision. The HUF appreciated, trading below the 380 level against the EUR – the strongest level in more than two years. Yields moderated, FRAs, swap and bonds yields sank by 2-4 bps across the curve, but this did not change the big picture: four 25-bps cuts are priced in the curve, starting from March, with one reduction in each quarter afterwards.

Before the decision: No rate change was foreseen

· Hungary’s benchmark interest rate has been flat at 6.5% since September 2024, but in December 2025, when publishing its latest Inflation Report, the MNB’s new management hinted at the possibility of interest rate cuts, by adding the information that the Council will take decisions on the base rate in a data-driven manner, from meeting to meeting. The market immediately began to price in interest rate cuts, and the yield curve soon implied four 25-basis-point reductions in 2026, instead of the previous two. After the announcement, the trend of forint appreciation stopped and the EUR/HUF even returned to the 390 level temporarily, while bond yields fell by 20-40 basis points. External data from the past month do not significantly affect the MNB's room for manoeuvre. Expectations of US interest rate cuts have weakened slightly, but the ECB's interest rate path has not really changed. But domestically, December’s inflation rate of 3.3% and core inflation rate of 3.8% came as a double whammy, as these indicators fell less than the MNB or we had expected; moreover, services inflation and several underlying inflation indicators accelerated. It is therefore not surprising that the central bank responded by saying that a more convincing figure is needed for an interest rate cut. In line with the market, we expected interest rates to remain on hold in January – nevertheless, the MNB's communication on its assessment of recent events and the conditions for interest rate cuts could significantly impact the bond and currency markets.

Our assessment: We remain slightly more cautious than the market regarding interest rate cuts; we expect a total of 50-basis-point reductions by the end of 2026, while market pricing suggests 100 basis point lower rates

· The MNB's forward guidance remained unchanged, although the tone was somewhat more hawkish than in December.

· We maintain our view that moderate price setting at the beginning of the year is necessary for looser monetary policy. The market is pricing in four cuts this year: the first one for March, then one in each quarter afterwards. We are more cautious: we expect a total of two reductions, one in March and one in September, if the underlying inflation indicators decline to a level that is consistent with the MNB’s 3% target, thereby confirming that inflation expectations are sufficiently anchored.

· Currently, two opposing effects are influencing our inflation forecast: persistently low energy prices and favourable food prices would pull down our inflation forecast, while the clear slowdown in the improvement of underlying processes would increase it. The net effect of these two factors is currently unclear, so we leave our inflation forecast for 2026 unchanged at 3. 4%. We think inflation will probably sink well below the 3% target temporarily at the beginning of 2026 because of the delayed excise duty hikes, the expectedly very low re-pricing in administered prices, and a significant drop of the oil prices measured in HUF. But incoming data strengthened again our view that inflation persistence has still not been satisfactorily broken, so the central bank’s caution remains warranted. This is particularly true if we take into account the 11% minimum wage hike, effective from this January, and the consumption-stimulating government measures coming into effect these days.

Expectations for the base rate (%)

Sources: Bloomberg, OTP Research, Focus Economics, MNB

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more