Hungary: A hawkish hold at 6.25%, as expected. If the government decides to adopt the EUR, the MNB will support the process

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

As expected, the MNB’s Monetary Council kept the base rate unchanged at 6.25% at its April meeting. The MNB is still keeping it’s message hawkish; there is no sign that they are in a hurry to cut interest rates.

The MNB's key messages:

· The Monetary Council is committed to achieving the 3% inflation target.

· The external environment is not supportive for monetary policy; the conflict in Iran, the developments in commodity prices endanger inflation targets of central banks.

· Investor sentiment has improved but remains vulnerable to geopolitical tensions.

· The MNB is closely monitoring the decisions of the Fed and the ECB.

· After the parliamentary elections, the risk premium on domestic assets fell, resulting in a country-specific appreciation of the HUF against the euro. The decline in the domestic risk premium led to a downward shift of the yield curve. However, the sustainability of these dynamics and the inflation impact still need to be confirmed.

· The cautious and patient monetary policy approach is still required. Maintaining tight monetary conditions remains justified. In this uncertain environment, the Council makes its decisions in a data-driven and prudent manner.

· If the Hungarian government decides to introduce the euro, the MNB will cooperate.

At it’s meeting today, the Monetary Council also discussed information material relating to the conditions for the steps leading to ERM II membership.

Market reactions

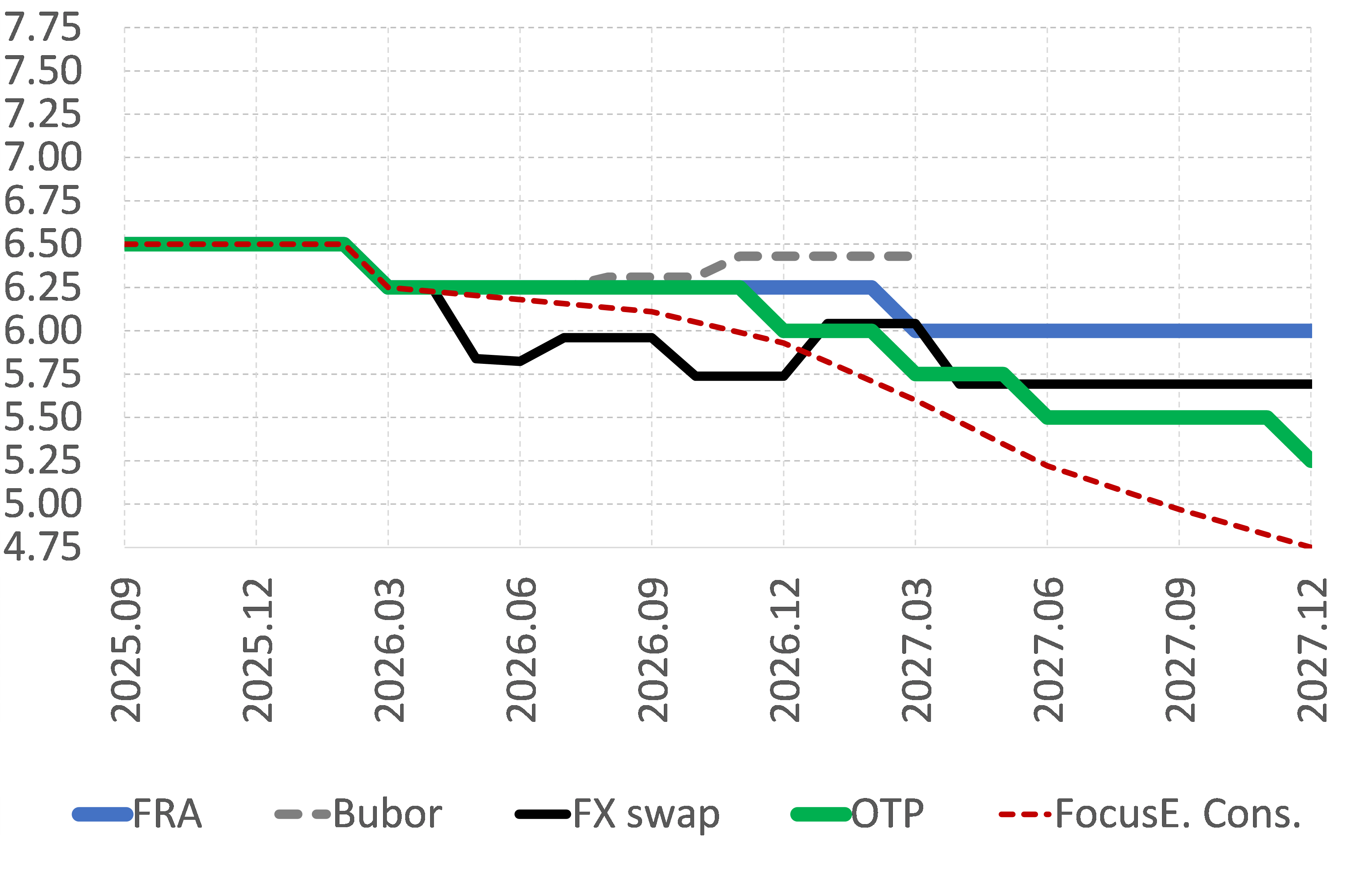

· The decision was in line with expectations, but the hawkish tone and the supportive approach to EUR adoption could contribute to the positive sentiment on Hungarian financial markets in the afternoon session. After the press conference theHUF appreciated by 0.5% against the EUR, while yields on the fixed incomemarkets fell by 2-5 bps. Market pricing reflects a flat base rate at 6.25% thisyear and one rate cut for 2027.

Before the decision: No rate change was foreseen

· Even though following the elections the domestic risk premium fell sharply, the forint strengthened, and inflation was favourable in the first three months of the year, we believed that the central bank would not change the base rate at this point.

· The central bank had previously communicated that it would react with interest rates in the case of a permanent change of risk assessment; therefore, it was expected that monetary policymakers would wait for the new government’s economic policy measures before cutting interest rates further.

Our assessment: Given the oil price shock and the MNB’s hawkish communication, the base rate could remain at 6.25% for some time; The outlook will depend on the policies of the new government, announced likely in the Autumn with the new budget: a credible fiscal consolidation strategy, unblocking EU funds and putting a reasonable plan for euro adoption on the table could pave the way for multiple rate cuts from 2026Q4.

· Due to very positive inflation developments in the first three months of 2026, we can now say that the inflation risks linked to the 11% minimum wage hike and to the government's consumption-stimulating measures did not materialize, and the strong exchange rate and weak economic growth appear to have brought lower re-pricing at the beginning of the year. The March inflation data reinforced the view that the effects of the war in Iran are hitting the economy at a point when the inflation situation is relatively favourable. With the current strong forint, inflation this year could remain below 3%, and there is a good chance it will stay around that level in 2027 as well. We expect 2.9% inflation in 2026 and the effect of the Iranian war can be around only 0.5ppts in our baseline scenario (included in the forecast figure above, with oil prices following the forward price curve).

· But inflation will accelerate later this year, and oil price and inflation risks are tilted to the upside. In this uncertain environment the favourable trends in EURHUF and the risk premium after the parliamentary elections and their positive impact on the inflation still might be temporary.

· Still, the new economic policy could be a game changer for Hungary. So far, we understand that the 2027 budget plan will be announced somewhere in the Autumn: a credible fiscal consolidation strategy, unblocking EU funds and putting a reasonable plan for euro adoption on the table could pave the way for multiple rate cuts from 2026Q4. We have pencilled in one cut in 2026 and in three cuts in 2027. Risks are tilted to both sides. Should the Iran war end soon, risk appetite toward HUF assets might increase further even before new economic policy announcements. In that case, rate cuts could come earlier. At the same time, if the budget deficit remains elevated for an extended period and the fiscal trajectory is not consistent with meeting the Maastricht criteria, yields could remain persistently more elevated, allowing less rate cuts.

Expectations for the base rate (%)

Sources: Bloomberg, OTP Research, Focus Economics, MNB

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more