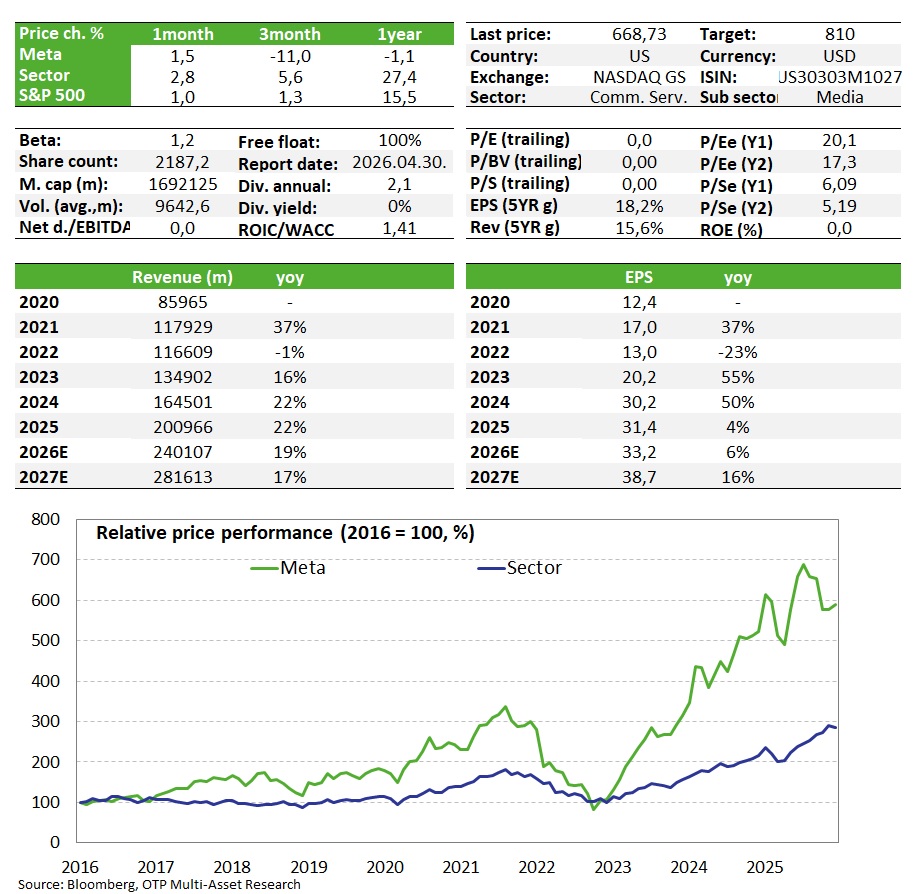

Meta: strong revenue, costs don't matter

Related content

Honeywell's stock price may be on the verge of a breakout

Major indices began to fall at the end of last week, but the movements were news-driven, and there has been significant volatility, which has resulted in a low number of opportunities indicating a quality breakout for the past two weeks. This week, one of the stocks from our Equity Top Pick List, Honeywell, also ranked high on the momentum list. After a minor pullback, the technical picture could indeed be supportive.

Uber Falls on Negative News

Uber shares failed to follow through on their breakout attempt, and on Friday, negative news concerning the company’s robotaxi business pushed the share price down to the stop-loss level specified in our trading idea.

Investors responded very positively to Meta's fourth-quarter report (+8%), as the company has so far been able to offset increased cost pressures with improved revenue dynamics. There have been periods in the past when investors would have fled at the sight of similar cost figures, but for now they believe that the expenses can be monetized (the revenue figures in the advertising market are indeed very impressive), perhaps partly because Meta still appears to be well positioned to benefit from the emergence of AI assistants. As Meta is currently the cheapest of the big tech companies, we continue to see this hidden option as attractive. As a result, we still keep Meta on our Equity Top Pick List.

Quarterly report

The top lines are reassuring, with active users growing to 3.58 billion (December average), representing a 7% increase on an annual basis. Ad impressions grew by 18%, and average ad prices also increased by 6% on average, resulting in total revenues of nearly $60 billion, up 24% from the base period. This is not only a big jump from an already strong base, but also significantly exceeds expectations (58.4 billion).

What's more, management is confident that these favorable trends will continue, with the current quarter also bringing in $53.5-56.5 billion in revenue, which is also a big surprise compared to the expected $51.3 billion. In other words, the company is able to demonstrate that its significant AI expenditures have a monetizable, revenue-boosting effect even in the short term, which is very important in order to maintain investor confidence in its more serious plans for the future.

Costs do not look good, having increased by 40% in the quarter, largely due to the signing of big-name AI experts, which has been widely reported in the news. Operating profit was thus much more modest, showing only 6% growth, with margins falling from 48% to 41%. Due to the increase in personnel expenses and infrastructure costs, a significant cost jump to $162-169 billion is expected by 2026, which is a significant change from last year's level of $117 billion, but also from the expected $151 billion. In other words, although revenue will also increase, this will still "only" be enough to slightly improve operating profit from last year's level. This therefore suggests a fragile balance for this year as well, and it will be necessary for investors to continue to trust that Meta will be among the first to monetize the potential expected from the emergence of AI agents.

Capital expenditures have been increased in a similar vein, even though investors were already keeping a close eye on previous plans. This year, the company plans to spend $115-135 billion, while the market had previously expected around $110 billion. This will reduce the company's free cash flow, and its net cash position will also deteriorate due to significant investment needs, although the balance sheet remains positive for the time being. All this puts pressure on share buybacks, which is a rather unfavorable development in the short term.

Valuation

The risks are somewhat offset by the fact that, thanks to the sideways movement of the share price over the past year, valuation multiples remain at comfortable levels, and in fact, the lowest multiples can be seen compared to the big tech giants (P/E: ~20, EV/EBITDA: ~14), while profit growth expectations do not justify this at all (20% EPS and EBITDA CAGR 2025-27). Based on these indicators, we maintain our previous fair value estimate of USD 810.

Investment story

- Meta's social media platforms are actively used by nearly 3.5 billion people every day. Its activities can be divided into two segments: applications such as Facebook, Instagram, Messenger, and WhatsApp, which account for the majority of its revenue, and products and solutions related to virtual and augmented reality (Reality Labs).

- Among the big tech companies, Meta may be one of the biggest beneficiaries of the continuous development of AI solutions, as it can leverage its existing, sufficiently large customer base: On the one hand, Meta AI is already running as a solution that engages in chat as a conversation partner, identifies and edits images, and can even serve as a live conversation partner on paper, with an active user base of more than 1 billion. There are still some issues with reliability, but these will be overcome as AI develops.

- The company spends most of its advertising revenue on developing AI capabilities, with plans to spend over $100 billion this year, but the associated personnel and other costs are also increasing significantly. Cost pressures hang over the stock like a sword of Damocles, but for now, strong revenue growth means investors are willing to accept that the company will be able to translate these expenses into results over time.

- On the one hand, AI solutions can help a lot in targeting ads more effectively by identifying behavioral habits and patterns, and new products can be developed based on this, while there is still further potential for growth in some of the company's platforms (expansion of Threads, exploitation of WhatsApp's potential). What is still a hidden reserve, and it is not yet clear whether the company will be able to capitalize on it, is the emergence and spread of AI agents and the development of "personal superintelligence," as envisioned by Mark Zuckerberg. Since Meta has a considerable amount of personal data based on our social media consumption and activity, it is well positioned to offer a truly personalized solution, which could even lead to a leading role in the AI assistant market. However, this requires investment, and the return on investment will only be seen later.

- TikTok poses strong competition to the company's platforms, but there is also the risk of competition authority and other legal concerns and penalties due to its large size (discussions with the European Commission may prompt the company to make changes that could have a significant negative impact on European revenues).

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more