Following record revenue, construction recovery would be key for Masterplast

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

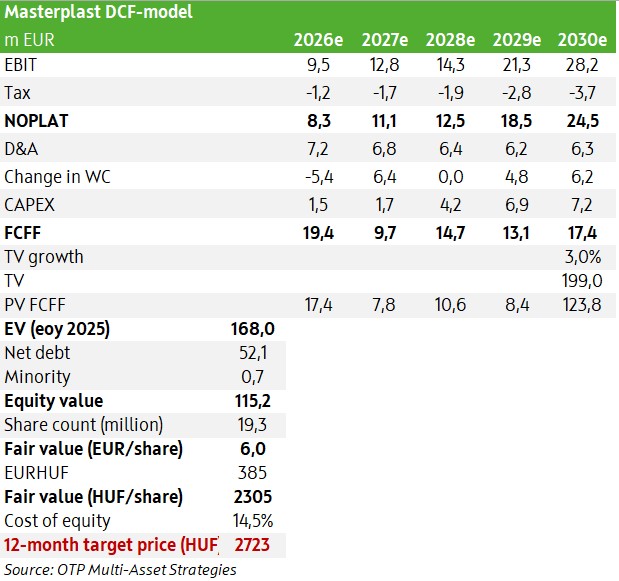

We have revised our DCF model and earnings estimates for Masterplast (a Hungarian player in the insulation business with regional presence). We have raised our 12-month target price to HUF 2723 (from HUF 2552 as of 01.07.2025), while we maintain our HOLD recommendation. The primary reason for raising the target price is that the company may be able to curb its capital expenditures more than previously expected, which supports FCFF estimates in the coming years, while we are calculating with a lower leverage beta due to the improving capital structure, which lowers WACC values.

Masterplast closed out 2025 with a strong quarter, achieving record revenue while also reaching EBITDA levels not seen since 2022; it also returned to profitability on a net income basis in Q4, excluding one-time items. However, the rise was primarily driven by strong demand for Certified Energy Savings (HEM), which may still support growth in early 2026, but we see little chance of repeating the Q4 figures. In segments independent of HEM, demand remains subdued, and the construction industry failed to show any meaningful turnaround in 2025. The number of new housing starts reached a decade-long low, though the pace of decline has slowed compared to 2024, while the number of building permits issued showed a significant increase. The Otthon Start program may also support a revival in new housing construction in the medium term, but its impact is likely to materialize only toward the end of the year at the earliest. In contrast, the Home Renovation and Rural Home Renovation Programs are expected to run out in the first half of the year. Overall, the business outlook remains characterized by significant uncertainty .

The macroeconomic outlook is mixed: revenue-weighted GDP growth forecasts for Masterplast’s markets indicate a 2.2% increase in 2026, following 1.2% in 2025. However, this forecast was 2.5% just eight months ago, and growth expectations for subsequent years are also slightly lower. In addition, the potential prolongation of the war in Iran creates further uncertainty and downside risks.

In our view, Masterplast’s liquidity position has improved since the middle of last year. With significantly higher cash reserves and the operating cash flow expected this year, the company may be able to cover its larger loan and bond repayments in 2026, assuming that short-term working capital loans are successfully extended.

Given the slower-than-expected economic recovery, we have revised our revenue forecasts downward over the longer term, although this may be partially offset by the positive impact of HEM sales in 2026. Overall, we still expect a YoY increase of approximately 6% in 2026 revenue, while the EBITDA margin could rise to 9.2%, although this still falls somewhat short of our previous expectations.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more