Investment Outlook Q3 2026

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

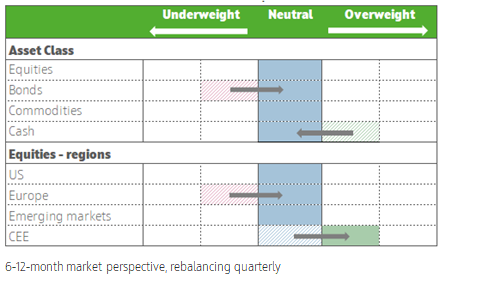

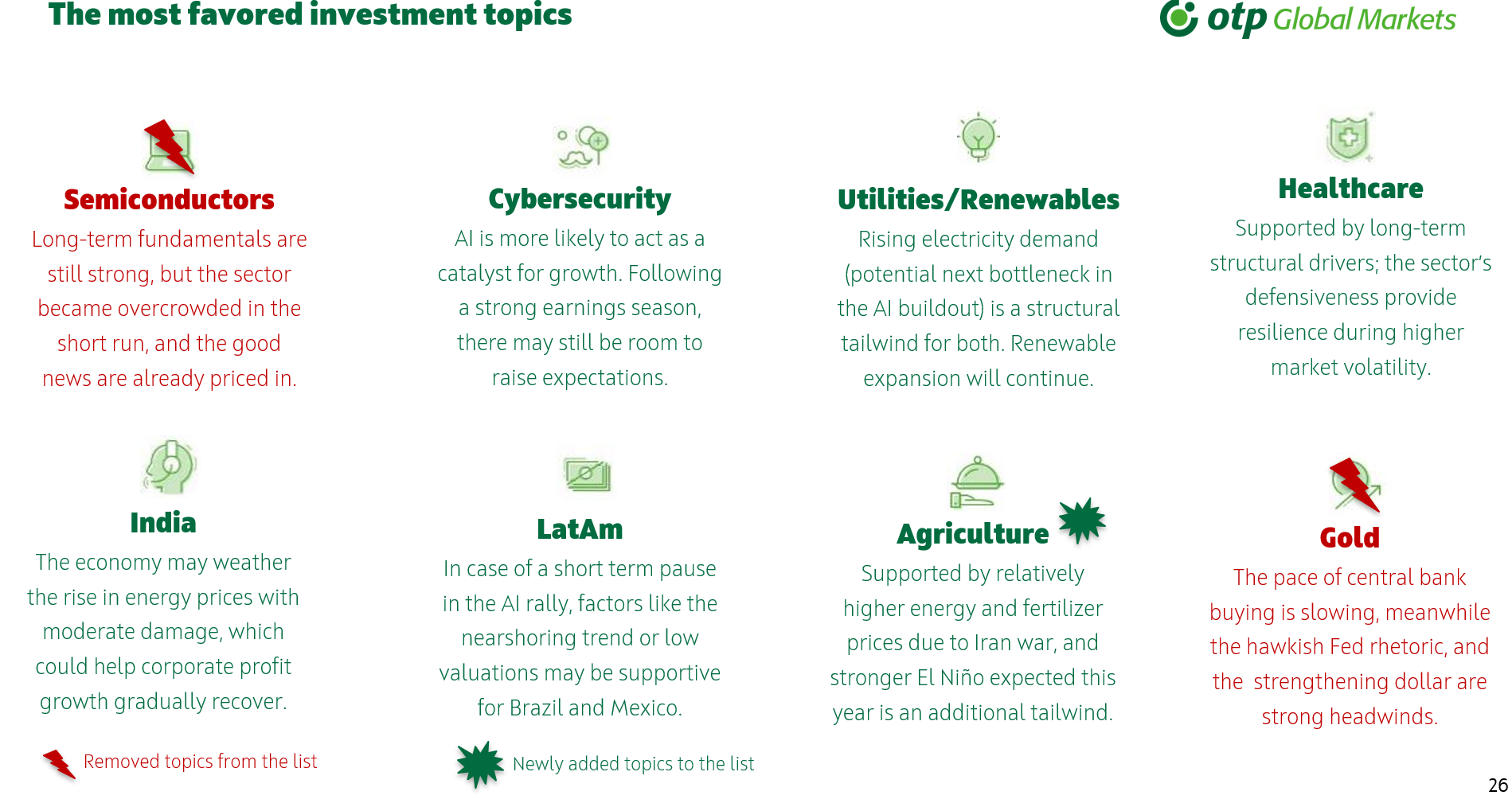

Strong profit growth remains supportive for equities, which could contribute to a broadening of the market rally beyond the technology sector. However, there are several risk factors, like the hawkish Fed, midterm elections, fragile US-Iran deal, large tech IPOs, and AI return fears, that could lead to increased market volatility. Semiconductors’ long-term fundamentals are still strong, but the sector became overcrowded in the short run, and the good news are already priced in, so we removed the sector from our most favored list. We would still keep AI related exposures, like cybersecurity on the software side, but since the next bottleneck could be the power supply to data centers, we remain optimistic about the utilities and renewable energy sectors, as well as healthcare, which stands to benefit from increasingly advanced AI solutions. As we expect a short term pause in the tech rally, even in the face of a significant profit boom, we would maintain neutral exposure regarding the US and EM regions. Given the normalization of energy prices, capital may shift toward relative laggards, like India, LatAm or the CEE region, which have a much more reasonable valuation and growth characteristics.

Macro

With the reopening of the Strait of Hormuz, the worst-case economic scenario may have been averted. Growth forecasts have stabilized in the US around 2% for both 2026 and 2027, and 0.7% and 1% in the eurozone. Inflation has remained persistently high in the US, with the base of acceleration broadening rather than narrowing. In the eurozone, inflation may hover around 3%, but inflationary pressures are not expected to strengthen over the medium term. As a result, the market has already priced in two interest rate hikes by the Fed this year, and even if the central bank ultimately does not go that far, the hawkish tone is likely to persist in the coming months. The ECB has already implemented one rate hike, and may not need to carry the second one out. Hungarian yield curve still prices in four cuts for this year, even as HUF is already testing the 350 level. We believe that at current levels, the risk distribution for the exchange rate is clearly tilted toward depreciation. However, we do not expect any significant HUF weakening.

Equities

Strong profit growth remains supportive for equities, which could contribute to a broadening of the market rally beyond the technology sector. However, there are several risk factors, like the hawkish Fed, midterm elections, fragile US-Iran deal, large tech IPOs, and AI return fears, that could lead to increased market volatility. Semiconductors’ long-term fundamentals are still strong, but the sector became overcrowded in the short run, and the good news are already priced in, so we removed the sector from our most favored list. We would still keep AI related exposures, like cybersecurity on the software side, but since the next bottleneck could be the power supply to data centers, we remain optimistic about the utilities and renewable energy sectors, as well as healthcare, which stands to benefit from increasingly advanced AI solutions. As we expect a short term pause in the tech rally, even in the face of a significant profit boom, we would maintain neutral exposure regarding the US and EM regions. Given the normalization of energy prices, capital may shift toward relative laggards, like India, LatAm or the CEE region, which have a much more reasonable valuation and growth characteristics.

Bonds

The rapid normalization of energy prices is helping to mitigate inflation risks, which is why it is recommended to maintain a neutral position on long-term bonds rather than underweighting them as before. Long bond yields in both the US and the eurozone are currently within what is considered a fair range in the current macro environment.

Commodities

We maintain our neutral view on commodities, as the conflict in the Middle East is still not resolved. As with energy prices, we expect that even if a peace agreement is reached, fertilizer prices may remain relatively higher, which coupled with a stronger El Nino, provide a tailwind for agricultural commodities. We removed gold from our favored list, as the pace of central bank buying is slowing, meanwhile the hawkish Fed rhetoric, and the strengthening dollar are strong headwinds.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more