Investment Outlook 2026

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

Consumption and AI related investments saved the year in the US with 2% GDP growth, and despite the trade war and shutdown the outlook remained solid. Fiscal and monetary easing continues to provide strong tailwinds, but equities are expensive, meaning there is less and less room for error. We are therefore keep some powder dry, to increase equity exposure in case of drawdowns, and selectively choosing between sectors and regions for excess returns. Within Europe, we see potential in the cheapest small-cap segment, several factors could catalyze its outperformance in addition to the German stimulus.

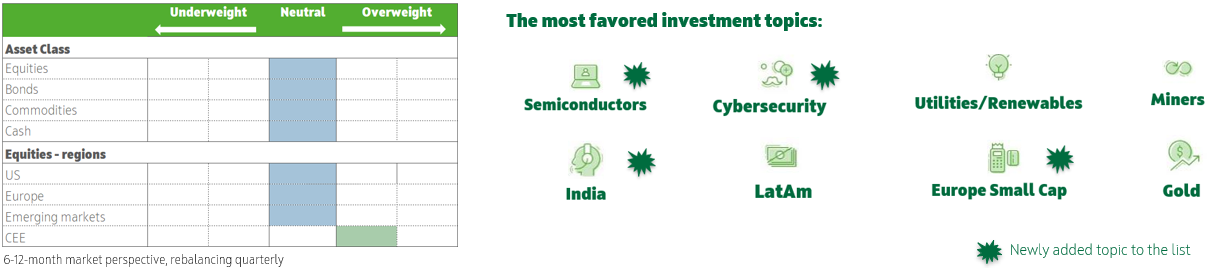

Macro

Consumption and AI related investments saved the year in the US with 2% GDP growth, and despite the trade war and shutdown the outlook remained solid. Recession risk is low, but the weakening labor market, high and fast rising debt, halted disinflation above CB’s target, and political pressure on the Fed remain a cause for concern. Looser fiscal policy in the EU could add to GDP growth in 2026-2027, but debt sustainability issues can not be neglected. Inflation is at target levels, but risks are more tilted to the upside. In the short run we expect the market to price in more cuts as the new FED chair is getting closer, which will moderate long bond yields. In Europe, we still expect term premiums to rise. From the current level, we do not expect further meaningful HUF appreciation, but holding long positions remains to be attractive due to high interest rate differential.

Equities

Fiscal and monetary easing continues to provide strong tailwinds, but equities are expensive, meaning there is less and less room for error. We are therefore keep some powder dry, to increase equity exposure in case of drawdowns, and selectively choosing between sectors and regions for excess returns. In the US, we favor sectors primarily linked to the development of AI infrastructure, like semis on the hardware and cybersecurity on the software, utilities/renewables on the energy supply side. Within Europe, we see potential in the cheapest small-cap segment, several factors could catalyze its outperformance in addition to the German stimulus. The weakening dollar and Fed interest rate cuts are tailwinds for EM, but valuation is already neutral, so we prefer the cheapest Brazil and the nearshoring driven Mexico. After a long consolidation, we would also start building positions in the structural megatrends driven India. We see no change in the factors driving CEE so far, depressed valuations compensate for higher risks.

Bonds

While the weakening labor market and slowing growth are pushing yields lower, continued significant budget deficits and deteriorating debt trajectories pose risks in the opposite direction. For this reason, we continue to favor the short/medium end of the yield curve. Corporate bonds’ historically tight spreads do not cover the increasing risks.

Commodities

We maintain an overall neutral view on commodities, as energy and agricultural products remain weak for now. However, the outlook for industrial and precious metals remains favorable, so selective exposure is recommended. We like copper, uranium, and gold related exposures.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more