Hungary: Another low inflation print ahead of the energy price shock

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

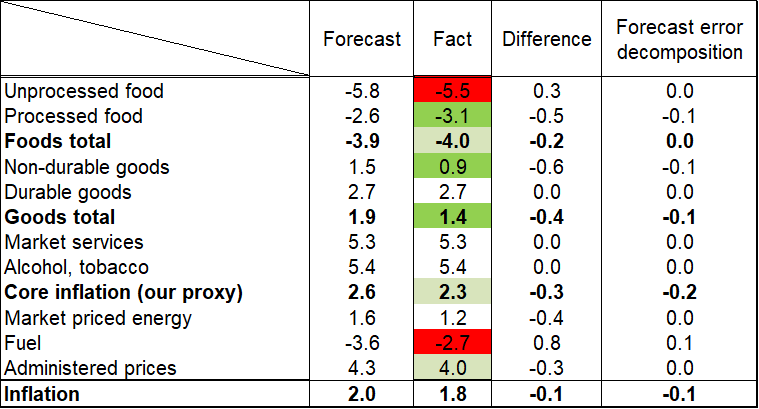

Hungary's headline inflation increased from 1.4% year-on-year in February, to 1.8% in March. The published data came as a surprise as it was lower than both the consensus (2.2%) and our forecast (2%). The downward surprise mostly came from lower-than-expected non-durable goods and processed food inflation, while fuel prices were slightly higher-than-foreseen. Core inflation edged down from 2.1 to 1.9%.· The March data do not yet reflect the impact of the Iran war. Even before the sharp increase in energy prices, we expected inflation to reach its annual low in February, followed by a gradual acceleration. The acceleration in inflation is largely driven by fuels and by the waning disinflationary effect of food prices, although prices in both categories are still declining on a year-on-year basis. By contrast, inflation in goods and services that determine inflation over the longer term eased further. The outlook largely depends on the outcome of the Iran war, in our new baseline we think inflation could be around 3% this year.

In our baseline scenario—where oil remains at USD 90–95 and gas at EUR 50–55 for around two months, followed by a normalization—we expect a relatively moderate additional inflationary impact of higher energy prices in 2026, below 0.5 percentage points. One reason for this is that the “starting” inflation environment prior to the energy price shock was relatively favorable: we observed restrained price setting at the beginning of the year among goods and services that determine inflation over the longer term, reinforced by strong disinflationary effects from food prices, as European meat and dairy markets are currently characterized by substantial oversupply. Another reason is that household products in principle directly affected by rising energy prices, such as fuel and household energy are regulated, which may keep the direct inflationary impact limited. On the other hand, indirect effects—through a weaker exchange rate and pass-through via production chains—appear much more slowly in inflation than direct effects. Furthermore, tight monetary policy and the weak business cycle position of the economy limit the cost pass-through. As a result, even under the assumed rise in energy prices in the baseline scenario, inflation could average around 3% in 2026. In 2027, however, inflation may rise above 3.5%, as we expect the currently favourable food price trends to reverse by then, and pass-through effects via production chains to generate additional inflation in 2027, especially during early-year price resets.

The main risk is a further escalation of the war in Iran, leading to a prolonged closure of the Strait of Hormuz and persistently elevated extreme energy prices. In such a scenario, the effects of the energy price shock could easily become non-linear. If the magnitude and/or duration of the shock were to exceed the level that firms can absorb through lower profits and governments through higher budgetary spending, both the speed and the extent of energy price pass-through would increase significantly. Moreover, the larger the energy price shock, the higher the probability of spillovers to other markets, including agricultural commodities. However, yesterday’s announcement of a temporary ceasefire and the continuation of negotiations reduce the likelihood of this adverse risk scenario.

We will publish the usual detailed assessment of the data tomorrow.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more