GDP growth accelerated slightly in Q4, but remains fragile and downside risks strengthened for 2026

Related content

India would take a step forward and become a developed country

The conflict in Iran and the effects of the El Nino weather phenomenon could cast a shadow over the Indian economy this year, but there is reason to be optimistic in the longer term. India remains one of the world’s fastest-growing economies, but it does not intend to stop there; the country has set an ambitious goal to transform itself into a developed nation by 2047, the centennial of its independence. In this part of our analysis on India, we examined what is currently happening in the Indian economy, as well as what the future may hold for India.

Noble: disappointing earnings report, but no tragedy

Noble, the offshore oil drilling company, published a disappointing Q2 earnings report. Although the company exceeded expectations in terms of revenue, its earnings fell significantly short of analysts’ forecasts. This can be mainly attributed to the fact that Petrobras has suspended operations at the company’s two deepwater drilling rigs. Consequently, operating cash flow has declined, and management has also revised its annual financial targets downward. However, this is not yet a tragic situation considering that the company has a high cash balance and strong liquidity, hence dividend payments are not at risk, and the market environment may improve next year. For now, we are keeping Noble’s shares on our Equity Top Pick List, but if market prospects deteriorate significantly in the coming months, we will remove the stock from the list.

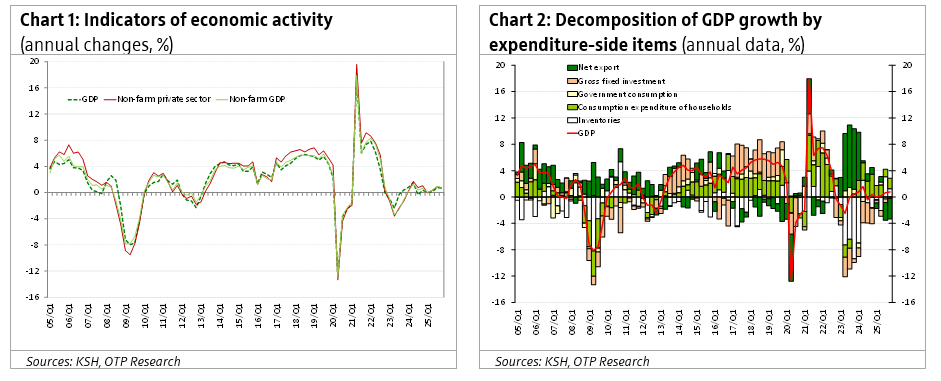

In Q4 2025, Hungary's gross domestic product grew by 0.8% year-on-year (non-adjusted), which is 0.1 ppts higher than the preliminary estimate. On a quarterly basis, in Q4 GDP growth accelerated from 0.0% to 0.4% according to KSH’s data. Our in-house seasonal adjustment shows somewhat lower, 0.3% QoQ growth. Non-farm GDP and non-farm private sector’s GDP expanded by 0.8 and 0.7% year-on-year, respectively, below their pace in Q3 (1% and 0.9%). QoQ growth figures also decelerated, from 0.3% to 0.1% in the case of non-farm GDP, while the growth pace of non-farm private sector GDP moderated from 0.1% to 0%. Underlying GDP indicators highlight that the Hungarian economy is still struggling and the conditions for a sustained recovery are not in place.

· In 2025 as a whole the Hungarian economy grew by 0.4%, 0.2 ppts slower than in 2024. Non-farm GDP growth also decelerated from 0.7% in 2024, to 0.5% in 2025, reflecting that the weak agricultural season is not the main factor behind the weak performance. Household consumption expenditure’s growth slowed from 6% in 2024 to 2.9% due to slowing real wage growth and declining employment, while the contribution of net exports to growth also deteriorated from 2.3 percentage points to -1.5 percentage points. These developments could not be offset by rising government consumption and a moderation in the decline in investment (from -9.9% in 2024, to -2.2%, after 9.9% in 2025).

· The big picture has not changed: the economy has been stagnating for three years, as rising consumption was counterbalanced by falling investment and decreasing exports. The Hungarian economy is facing similar challenges to those experienced by other industry-focused economies across Europe. These challenges include a shift in demand toward services, while the automotive sector –the former driver of growth– struggles with high energy prices, technological transitions, and increasing competition from China. However, the Hungarian economy underperformed even in regional comparison, as most peers could reach 1-2% growth on average in the 2023-2025 period, which was the consequence of several country-specific factors. Investment has declined sharply for four consecutive years, as the previous investment-focused economic strategy led to overcapacities, the key drivers of investment activity have deteriorated significantly, and public investment has also been scaled back due to the freezing of EU funds and the need to rein in the budget deficit. Hungary’s manufacturing sector remains heavily dependent on car and battery production — industries that currently underperform across many economies.

· However, expenditure-side developments confirm our slightly optimistic expectations for 2026. First, after four years of decline, we expect investments to start growing in 2026. Since fixed capital formation stagnated in Q4 as well as in Q3 on a QoQ basis, it seems very likely that investments could have already hit the bottom (year-on-year decline moderated to only 1% in Q4). In addition to the headline capital formation data, corporate lending, the number of new building permits, and the trend in construction orders also confirm our expectations of a recovery. Among the sectors, we expect rebound in 2026, particularly in households’ housing investment (the number of completed dwellings fell to a 10-year low in 2025, while the subsidized Otthon Start loan program introduced in the autumn of 2025 significantly increased demand for new homes) and, due to the elections, in public investment. This is why we expect that fixed capital formation can grow by around 4% this year.

Household consumption expenditure’s growth accelerated on both a year-on-year and quarter-on-quarter basis. The former accelerated from 2.3% to 2.7%, while the latter rose from 0.6% to 1% (according to our in-house seasonal adjustment, QoQ growth accelerated from 0.5% to 0.8%). Government measures such as the increase in family tax allowances and the extension of tax allowances for mothers with children began to take effect in Q4. The annualized consumption growth of around 4% confirms our consumption growth forecast of 4.5% for 2026, as further significant fiscal measures will come into effect in the first quarter of 2026 (introduction of a 14th month pension, a six-month bonus for the armed forces, an 11% increase in the minimum wage (while inflation fell to 2.1% in January), etc.).

· Although exports grew by 0.5% year-on-year in Q4 following a 0.1% decline in Q3, this remains a very weak performance, especially considering that the EU economy proved to be much more resilient to the trade war in 2025 than previously assumed. In addition, in Q4, the acceleration in imports (from 3.8% to 5.2% year-on-year) exceeded that of exports, so the growth contribution of net exports fell to -3.1 percentage points in Q4 from -2.7 percentage points in Q3. In 2026, exports may pick up compared to the stagnation in 2025 due to the acceleration of the German economy and new export capacities, but the rate of growth is likely to be modest, around 2-4%. It is very difficult to tell to what extent the new Hungarian battery and car manufacturing capacities will cannibalize the old ones, given the significant global overcapacity in battery production and stagnating European car sales. In any case, the beginning of the year is overshadowed by the fact that the Mercedes factory in Kecskemét switched to a single-shift production system in the first months of 2026, officially due to preparations for a model change.

· We still maintain our 2.3% growth forecast for 2026. We believe that the Q4 data confirmed our expectations regarding the main trends, but downside risks related to the “extent” of these trends have increased. The main downside risks are: (1) a protracted war in Iran would certainly increase inflation, decelerate real wage growth, and negatively affect several sectors that use hydrocarbons as raw materials, (2) after elections, the budget may possible to be adjusted to achieve the government's deficit targets (2026: 5%, 2027: 4%), and (3) declining employment and the resulting increase in labour market uncertainty may hold back consumer spending, which is the main driver of growth (especially if this is compounded by the inflationary shock of the war in Iran and/or fiscal adjustment measures).

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more