No sign of recovery in Q3 2025 means weaker growth outlook also for 2026

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

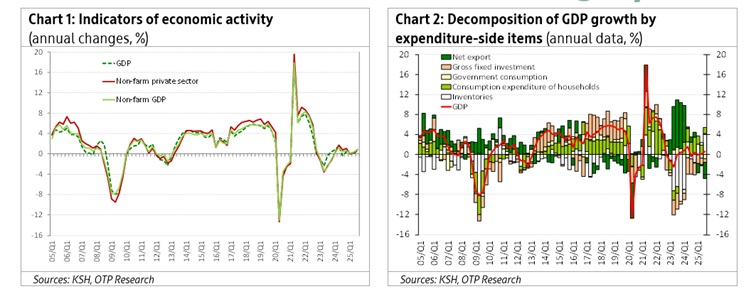

In Q3 2025, Hungary's gross domestic product grew by 0.6% year-on-year (non-adjusted), in line with the preliminary estimate. On a quarterly basis, GDP stagnated according to KSH’s data and our in-house seasonal adjustment. Both non-farm GDP and non-farm private sector’s GDP expanded by 0.9% year-on-year. The former grew by 0.2%, while the latter increased by 0.1% QoQ. These figures barely paint a better picture than the headline GDP.

· The big picture – stagnation for three years, as rising consumption is counterbalanced by falling investment and decreasing exports – roughly remained the same. The Hungarian economy is facing similar challenges to those experienced by other industry-focused economies across Europe. These challenges include a shift in demand toward services, while the automotive sector – the former driver of growth – struggles with high energy prices, technological transitions, and increasing competition from China. In addition to external challenges, several country-specific factors are contributing to Hungary’s weak economic performance. Investment has declined sharply for the third consecutive year, as the previous investment-focused economic strategy led to overcapacities, the key drivers of investment activity have deteriorated significantly, and public investment has also been scaled back due to the freezing of EU funds and the need to rein in the budget deficit. Hungary’s manufacturing sector remains heavily dependent on car and battery production — industries that currently underperform across many economies.

· The Hungarian Central Statistical Office (KSH) has made significant revisions to previous years' figures. In 2024 as a whole, the growth contribution of final consumption expenditure of households (aggregation of households’ consumption expenditure and transfers in kind), fixed capital formation and net exports were revised up (from 2.1 ppts to 2.9 ppts, from -2.8 ppts to -2.5 ppts, and from 0.7 ppts to 2.5 ppts, respectively), while that of inventories was revised down from 1.1 ppts to -1.7 ppts. With the downward revision of inventory change, the inventory-to-GDP ratio continued to converge towards its historical average, following a significant increase in 2022. With the upward revision of household final consumption expenditure (up HUF 1,178 bn at current prices, YoY growth rate: from 3.5% to 4.9%), the downward trend in household financial asset acquisition since the second half of 2024 becomes more understandable (Chart 10). The 2024 data revisions only reinforced the "consumption-heavy" growth structure. Although after the revisions, the growth contribution of net exports almost matches that of final consumption expenditure of households, this has been achieved amid declining export and import figures, which cannot be considered a textbook example of a healthy growth composition.

· On the expenditure side, the KSH significantly revised the data for the first half of 2025. The key driver of economic growth remained households’ consumption (and inventory accumulation), but to much smaller extent than we had previously known. The growth of households’ consumption expenditure in H1 2025 was revised down from 4.5% to 3.3%, and it reached only 2.6% in Q3. This is a significant change even when compared to the previous data release, which showed that households’ consumption expenditure growth slowed from 5.1% in 2024 to 4.5% in 2025H1, while the revised data show that the 6% growth in 2024 slowed to 3.3%. Such a slowdown in household consumption growth is not necessarily surprising, given that real wage growth of around 8.5% in 2024 may slow to around 4.5% this year and has temporarily slowed to below 4% due to a surge in inflation at the beginning of the year. In addition to slowing real wage growth, increasing labour market uncertainty —declining job vacancies, rising layoffs, and slightly declining employment, all of which are phenomena that workers have not faced for a long time— may also curb consumer spending. While the government raised family tax allowances in the first round on 1 July, and there are still a bunch of consumption-targeting measures in the pipeline (like introducing 14th-month pension, a six-month bonus for armed forces, the second round of raising family tax allowance from 1 January, tax exemption for mothers with three children from October, the introduction of tax exemption for mothers under 40 with two children from 1 January, minimum wage hike by more than 10%, while inflation is expected to fall to 3.5% in 2026), but with the significantly revised down data, the 4.7% growth in household consumption expected for this year and the 6% growth expected for 2026 are no longer achievable. Currently we expect that households’ consumption expenditure will increase by 2.9% and 4.5% in 2025 and 2026, respectively.

· Fixed capital formation data for H1 2025 have also been revised. According to this, instead of the previously known 8.3% YoY fall, the decline was only 7%. Another positive factor is that the QoQ drop in investments essentially stopped in Q3, which indicates that the twelve-quarter-long contraction in investment may reach its bottom, and it can be the first ray of hope that some growth can be expected in this area next year. Thanks to the upward revision of the data, the decline in investment in 2025 may be 4.7% instead of the previously expected 7%. There are numerous signs that the long-awaited turnaround in investment may finally happen in 2026. Public investment may increase next year, and housing investment may also pick up, thanks to the housing capital program (which stimulates the supply side of the housing market) and the Otthon Start subsidized housing loan scheme. The easing of trade war uncertainty, the improvement in demand prospects, and the improvement in corporate borrowing all suggest that corporate investment may also begin to improve. So, we think around 4% growth in fixed capital formation is still achievable in 2026.

· The growth contribution of net exports improved from -1.9 percentage points to -1 percentage point following the 2025H1 data revisions. However, this improvement occurred in the most unfavourable way: H1 YoY export growth fell from -0.6% to -2.2%, while YoY imports fell from 2% to -1%. Weak imports partly reflect weak domestic demand. However, weak imports – viewing imports as production inputs – also suggest that companies are not planning to increase their production. The data revisions only confirm our earlier expectation that exports may decline in 2025 as well as in 2024, but by 1.5% instead of the previously expected 0.3%. Declining exports in two consecutive years highlight again that Hungary’s exports are negatively affected by the sectoral structure of the domestic manufacturing industry (strong dependence on battery and car manufacturing). Hopefully, exports pick up in 2026 due to Germany’s fiscal stimulus and new export capacities coming on stream (BMW, BYD), but its growth can be somewhat lower (2.2% vs 2.5%) than previously thought, because of lower rollover effect.

· For 2025 as a whole, GDP growth of 0.5% appears realistic, rather than the previously expected 0.6% even if we expect some acceleration in the fourth quarter (if only for statistical reasons). In Q4, the weight of agriculture, which is showing a decline, is much smaller in GDP than in Q3. In addition, construction output fell by 22% in August, reducing the Q3 average figure by 7%, and GDP by 0.3%, but after a rebound in September, this effect will likely reverse. Furthermore, the tax relief for mothers with three children will come into effect in Q4 and this might stimulate household consumption.

· We have also lowered our growth forecast for 2026 from 3% to 2.3% due to the following reasons: (1) data revisions reveal a less favourable growth structure than previously thought, (2) weak Q3 growth data, and (3) the deteriorating labour market situation and low savings rate threaten consumption growth, which would be the main driver of GDP growth next year. Among the upside risks, it should be noted that the government has raised its deficit target for 2025 to 5%, which is well above the 3.6% rolling deficit seen in Q3. The increased deficit target thus gives the government considerable leeway to introduce additional measures, the effects of which will only be seen in 2026 growth. However, it is important to highlight two downside risks: (1) households will spend less due to uncertainty about the labour market and possible fiscal adjustments, or (2) fiscal stimulus will significantly worsen the external balance (as we have seen previously in Romania).

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more