Balance of Payments: C/A surplus at 2% of GDP, sustainable debt trajectory

Related content

AI Could Be the New Profit Driver for Digital Platforms

In recent years, artificial intelligence has become one of the most important topics in the technology sector. While much of the attention is focused on model developers and companies providing infrastructure, the long-term winners in this technology may also emerge on the application side. The interactive media segment is particularly interesting from this perspective, as the business models of companies operating in this field rely heavily on monetizing user attention and producing digital content. In the second part of our industry analysis series, we review current trends and potential catalysts affecting search engines and social media platforms.

European Software Companies Are Set to Make a Comeback

European stock markets are currently outperforming their U.S. counterparts, and thanks to the gains of the past few days, our screenings have identified a number of interesting stocks. Among these, we have highlighted stocks that have recently shown signs of a structural turnaround, while strengthening buying pressure is also supporting the positive technical picture. One such company is Germany’s Nemetschek, a leading provider of construction and architectural design software. The other is the Dutch firm Wolters Kluwer, which offers professional information, software, and specialized database solutions. For both stocks, the search for long entry opportunities may have begun.

Hungary’s external position remains the most reassuring aspect of Hungary’s macroeconomic situation. Based on a current account surplus of around 2% of GDP, the gross external debt ratio stagnating or slightly declining between 60–65% of GDP (in line with the regional average), and foreign exchange reserves about EUR 10 billion higher than required by reserve adequacy rules, Hungary’s external balance position is significantly stronger than what would be considered sustainable.

Looking ahead, we keep our forecasts on the current account at 2% of GDP in 2025 and 1.3% in 2026. Consequently, the net financing capacity could remain in positive territory this year and next, despite the expected rise in domestic demand. We expect net FDI inflow to remain slightly positive. Hungary’s external debt indicators could gradually decline further, with gross external debt moderating to around 60% of GDP in 2026.

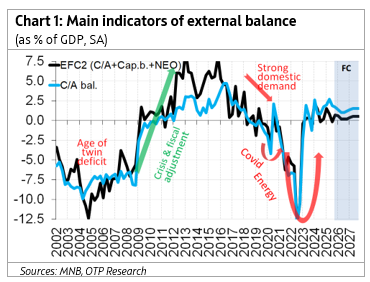

Indicators of external balance: the current account balance remained around 2% of GDP, while the external financing capacity is around zero

· Current account balance remained around 2% of GDP: In Q3 2025, Hungary's current account balance reached a EUR +0.9 billion surplus in NSA terms, in line with the preliminary data. In seasonally adjusted terms, the surplus was EUR 1 bn, or 2% of GDP, roughly the same as in the past four quarters. This means that the fiscal adjustment and the fall in investments could counterbalance the effects of rising consumption and still weak export demand (SA export data kept on declining).

· EFC1: between 2-3% of GDP. Hungary's external financing capacity (the sum of the current account and the capital balance) reached 2.3% of GDP in Q3, below the 3.3% figure in Q2, but in line with the figures between 2% and 3% of GDP in the past few quarters. The surplus of the capital balance reached 0.5% of GDP, in line with the subdued levels seen after the freeze of EU funds, well below the 2% level before.

· EFC2: around zero. (EFC1 plus net errors and omissions), the net financing capacity, which we usually consider the best and most stable indicator of external imbalances, fell to 0 in Q3, and remained moderately positive in the past four quarters (+0.4% of GDP). As usual in the first few publications, the NEO remained highly negative (-2% / -2.5% % of GDP). As we wrote many times before, the negative NEO could be the consequence of hidden imports through online retail trade and/or capital outflows under the radar (most likely the latter in recent years).

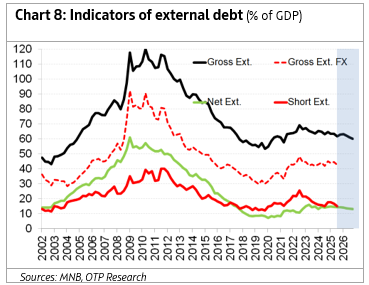

Indebtedness and reserves: Slight decrease in debt ratios, FX reserves above the adequate levels

·First, we emphasise that we use the BoP and external debt figures without SPVs. In our view, the figures that contain special-purpose vehicles are heavily distorted by entities that do not have much to do with the Hungarian economy. Therefore we rely on data cleaned from SPVs, as these data are much more consistent with the Hungarian macro-trajectory, and give us reliable information on indebtedness and vulnerability. We also filter out intercompany loans, which we consider to be more FDI-like than debt.

· The gradual but steady decline in the indicators of external debt between 2010 and 2019 was a key factor in supporting Hungary's credit story, and its rating as well. Having topped out in 2009-2010 at very high levels (gross external debt at 120% of GDP), it fell to levels of around 50-55% of GDP, which could be considered low even in regional comparison. From 2020 the decrease in debt reversed due to the energy crisis (just like in most CEE countries; see Chart 7), and debt ratios followed upward trajectories; levels were still not high in CEE comparison. In 2023, debt ratios started to moderate again, albeit very gradually.

· Indicators of external indebtedness have been stagnating, or very slightly decreasing, for a while. Net external debt stagnates just below 15% of GDP, gross external debt fell to 62%, the lowest level in four years, after topping out near 70% of GDP in 2022. Gross external FX debt has been fluctuating around 45% of GDP and short-term external debt between 15% and 20% for many quarters.

Hungary's FX reserves rose to EUR 48 billion in Q3 (or 22% of GDP) and to EUR 50 bn in November. The surplus of FX reserves above the level suggested by the reserve adequacy rules increased further, to EUR 10-15 bn, providing room for the national bank to be active on the FX market, if needed.

Outlook:

The external trajectory remained solid, which could support the HUF looking ahead. The C/A surplus will reach 2% of GDP in 2025 and 1.3% in 2026, despite the recent appreciation and the ongoing consumption-led recovery. Hungary’s net financing capacity could remain in the slightly positive territory in 2025 and 2026, just like net FDI inflow. All in all, we expect the economy to be a net debt repayer and the gross-external-debt-to-GDP ratio could slightly decline toward 60% by the end of 2026. FX reserves will exceed the adequate level significantly. Risks are balanced, with higher export growth due to stronger external demand on the positive side, while fiscal measures could boost consumption and imports more than we expect.

Get more out of your investments!

Global Markets Services

OTP Global Markets offers a broad range of services in the field of local and international money and capital markets.

Read morePrivate Banking Services

Personal care and expertise with OTP Private Banking, along with the knowledge, security, and innovations of a multinational banking group.

Read more